Vision classes

Vision classes

1. Meaning & characteristics of NPO

NON-PROFIT ORGANISATION

MEANING & CHARACTERISTICS

Organizations are of two types: - profit-making & non-profit making. Profit-making organizations operate with the main objective of earning profit. But there are organizations whose objective is not to earn profit but to render services. These organizations are called non-profit making organizations. The services are rendered to its own members or to the society at large. The main objective of such organizations may be social, educational, religious, or charitable. The surplus arising from rendering services is not distributed among its members by way of dividends or share of profit but utilized for the furtherance of the objective of the organization—examples of non-profit making organizations are clubs, societies, schools, colleges, hospitals, charitable trusts etc.

Features of non-profit making ORGANISATIONS:

The features of non-profit making organizations are as follows:

1. Service motive – Unlike profit-making organizations, the non-profit making organization operates with the motive to serve the people of the society.

2. Separate identity – The non-profit making organizations have separate legal entities.

3. Form of organization – Such organizations function in the form of schools, colleges, hospitals, clubs, societies, charitable trusts etc.

4. Utilisation of surplus – The excess revenue earned over the cost incurred in the process of rendering services is not distributed among its members. Rather it is utilized for achieving the objective of serving society.

5. Financing – Non-profit making organizations cannot financially operate only by receiving revenue from rendering services. Therefore, it receives donations either from members or outsiders to finance the cost of rendering services.

6. Budget – Each non-profit organization prepares an annual budget. The budget gives information about the anticipated receipt and expenditure for the ensuing year.

7. Management – Such organizations are managed by elected representatives of the members.

8. Accounting – Non-profit making organizations are required to prepare their annual accounts and these accounts are submitted to the members of the government departments. The accounts are prepared on an accrual basis.

1. Nature of partnership, Partnership Deed, Maintenance of Partnership accounts,

Meaning

Partnership business is an association between two or more persons who agree to do business & share profits & losses. The partners act as both agents & principals of the firm.

“Partnership is the relation between persons who have agreed to share the profits of a business carried on by all or any of them acting for all.” Section 4 of Indian Partnership Act, 1932.

Nature & Essential features of Partnership

Partnership is a separate business entity from the accounting viewpoint. However, from the legal viewpoint, a partnership firm is not separate from its partners. In case the business assets are not enough to meet the liabilities, the partner’s personal assets would also be liable to meet the debts.

Features

- Two or more persons – In a partnership business, the minimum number of partners is two & the maximum number of partners allowed is 50.

- Agreement – The relationship between partners is based on an agreement & that agreement is known as Partnership Deed.

- Profit-sharing – A partnership business is formed to do lawful business.

- Business of partnership can be carried on by all or any of them acting for all.

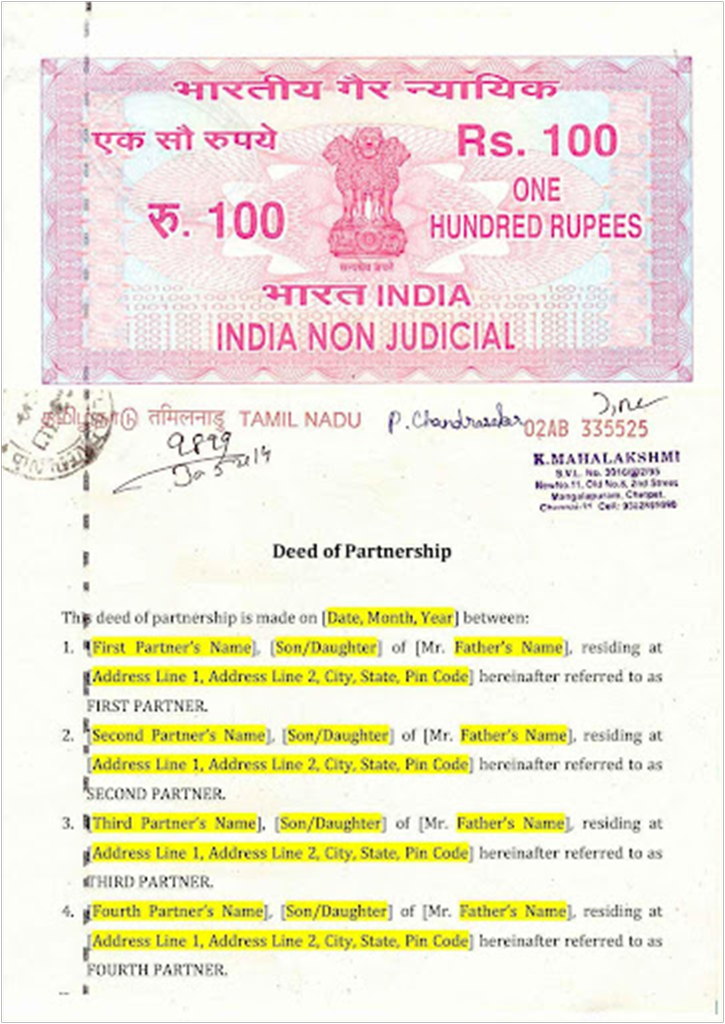

Partnership Deed

Partnership comes into existence by an oral or written agreement between the partners which contains all the terms & conditions of partnership. This agreement defines the relationship between partners. It is a legal document which is signed by all the partners. This document helps in avoiding any kind of dispute in future among the partners. This document is known as Partnership Deed.

A partnership deed, we can say, is the most important document in partnership business & it consists of the following clauses;

- Description of partners – Name, description & address of partners.

- Description of the firm – Name & address of the firm.

- Principal place of business – Address of the principal place of business

- Nature of business – What type of business is it - Trading or manufacturing? The nature of business is mentioned here.

- Commencement of Business – Date of commencement of partnership is mentioned here.

- Capital Contribution – The amount of capital to be contributed by each partner & whether the capital accounts are fixed or fluctuating.

- Interest on Capital – Rate of interest, if allowed, on capital

- Interest on Drawings – Rate of interest, if to be charged, on drawings

- Profit-Sharing Ratio – Ratio in which profits & losses are to be shared by partners.

- Interest on Loan – Rate of interest on loan given by a partner to a firm.

- Salary – Amount of salary, and commission to be paid to the partners

- Settlement of accounts – The manner in which the accounts of the partners are to be settled in case of his retirement, death or dissolution of partnership.

- Accounting period – The date on which accounts shall be closed every year.

- Rights & duties of partners – The rights & duties of partners are defined here.

- Duration of partnership – The period of partnership for which it has been started.

- Bank account operation – How shall the bank accounts be operated? Whether it shall be operated by any partner or jointly.

- Valuation of Assets – The manner in which the assets & liabilities of the firm are to be valued.

- Death of a partner – Whether the firm will continue or dissolve after the death of a partner.

- Settlement of Disputes – If there is any dispute among the partners then how it’ll be settled.

SPECIAL ASPECTS OF A PARTNERSHIP ACCOUNT

When the partnership deed is silent or does not have any clause in respect of the following matters or no partnership deed has been prepared by the partners, the following provisions of the Indian Partnership Act, 1932, shall apply:-

- Sharing of profit & losses – Profit & losses to be shared equally by all the partners.

- Interest on Capital – Interest on capital is not paid to any partner.

- Interest on Drawings – Interest on drawings is not charged to any partner.

- Interest on loan or advance/ loans by partners – Interest on loans is paid @ 6% pa. Interest is payable even if there is a loss.

- Remuneration to partners – Remuneration (salary, commission etc.) is not paid or allowed to any partner.

Some other important points:-

- A minor may be admitted for the benefit of partnership.

- A partner may retire from partnership with the consent of other partners or as per the agreement.

- Registration of firm is optional & not compulsory.

- Unless otherwise agreed by the partners, a firm is dissolved on the death of a partner.

Note – These provisions are applicable even if the partnership deed does not have a clause to this effect.

Maintenance of Partnership Accounts

This is how partnership accounts are maintained

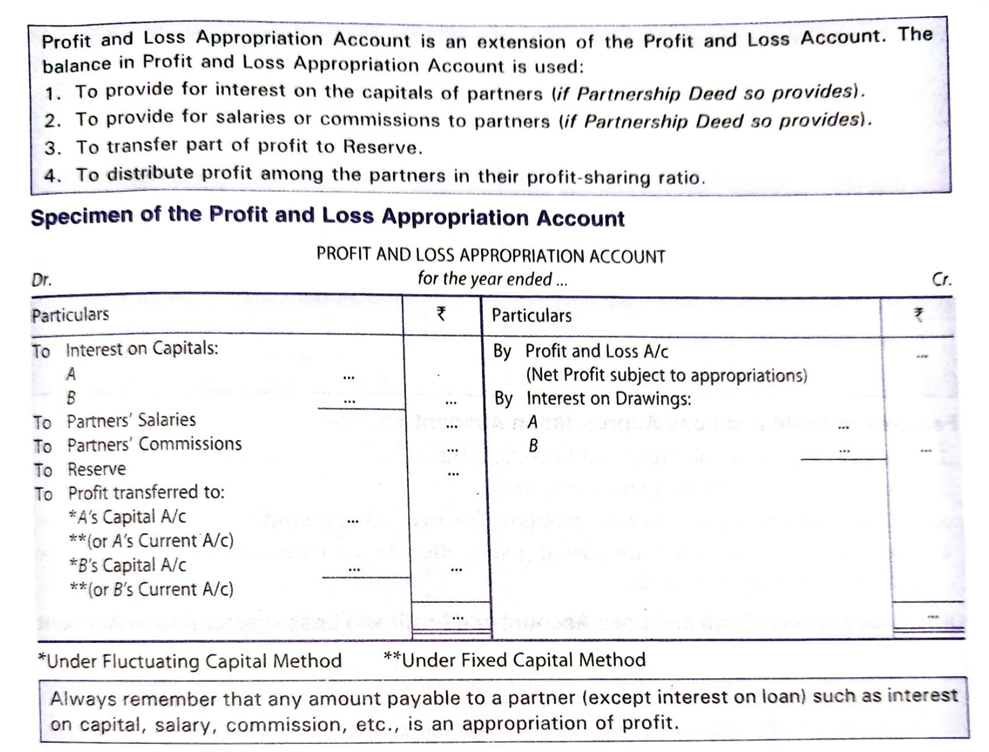

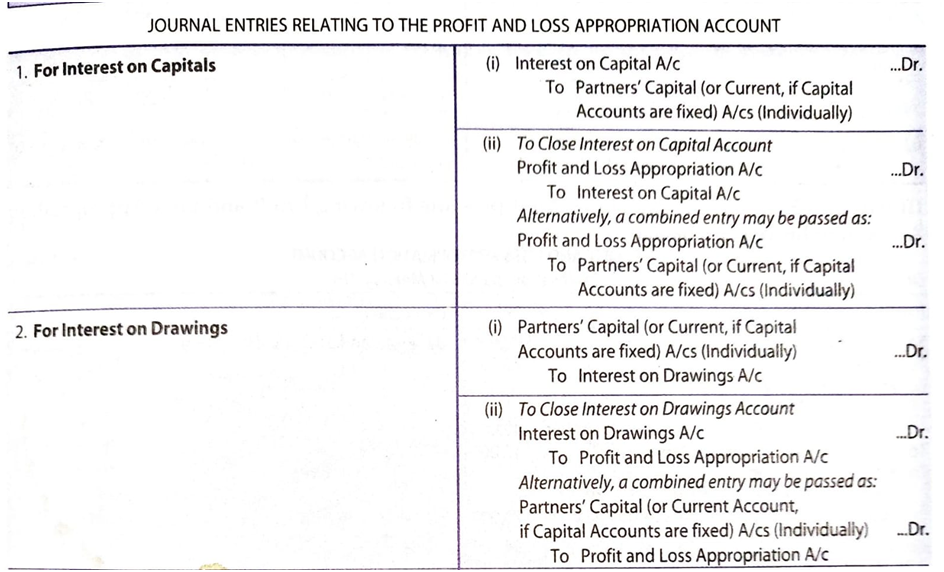

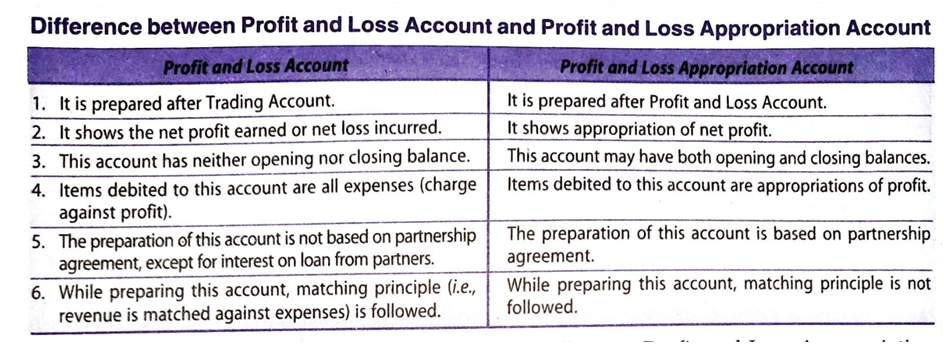

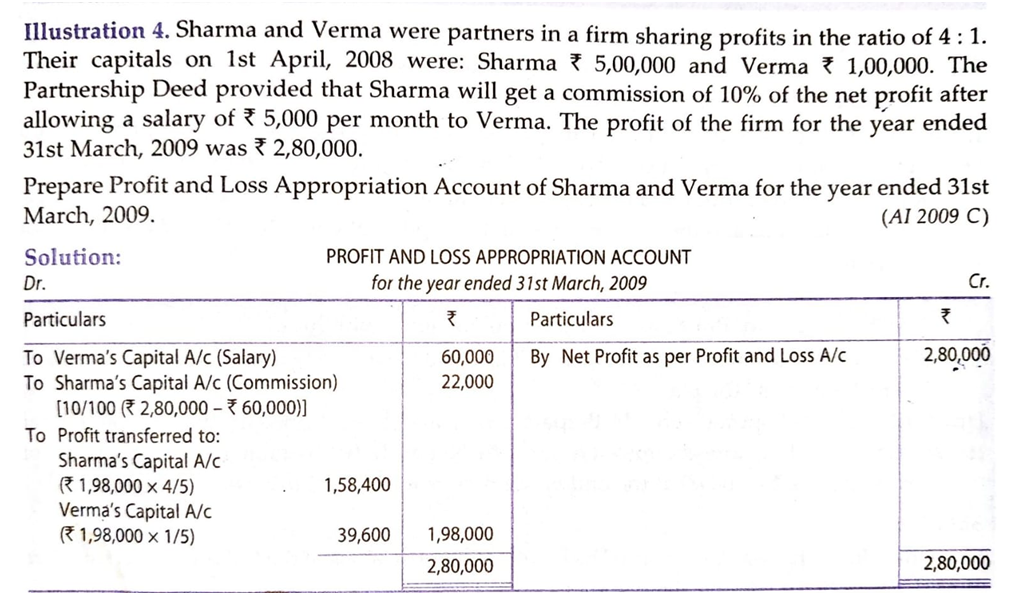

After the determination of net profit by preparing Profit & Loss A/c, we have to prepare Profit & Loss Appropriation A/c. Profit & Loss Appropriation A/c is an extension of Profit & Loss A/c. It is credited with the Net Profit taken from the Profit & Loss A/c & interest on drawings & debited with interest on capital, partner’s salaries & commissions. If the partners decide to transfer a certain part of the profit to Reserves, then it is also shown in the Dr side& the balance profit is distributed among the partners in their profit sharing ratio.

2. Accounting records

financial statements of non-profit making organizations

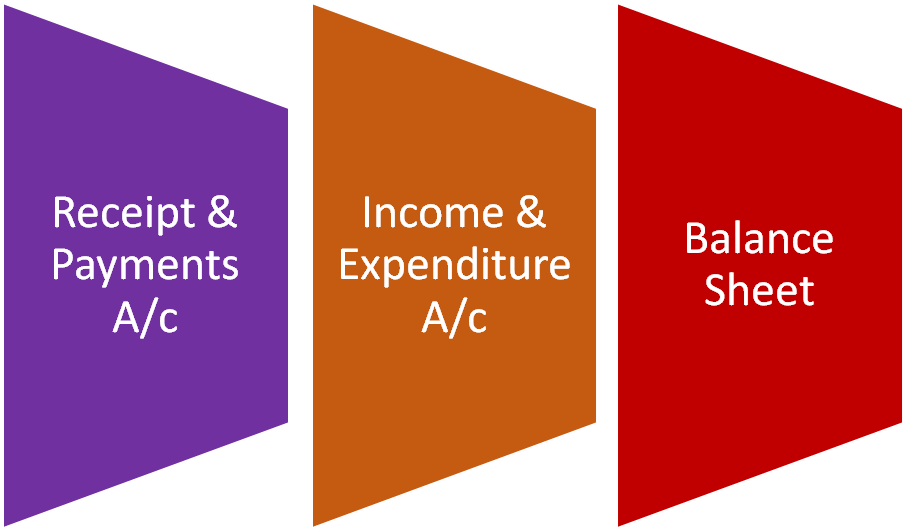

Like trading organizations, non-profit making organizations also prepare their financial statements at the end of each accounting period. Their financial statements comprise the following:

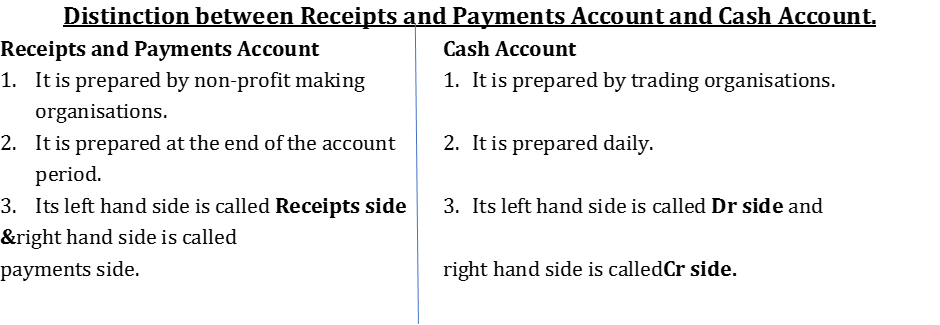

1. Receipts and Payments Account (Cash Book)

2. Income and Expenditure Account (Profit & Loss A/c)

3. Balance Sheet.

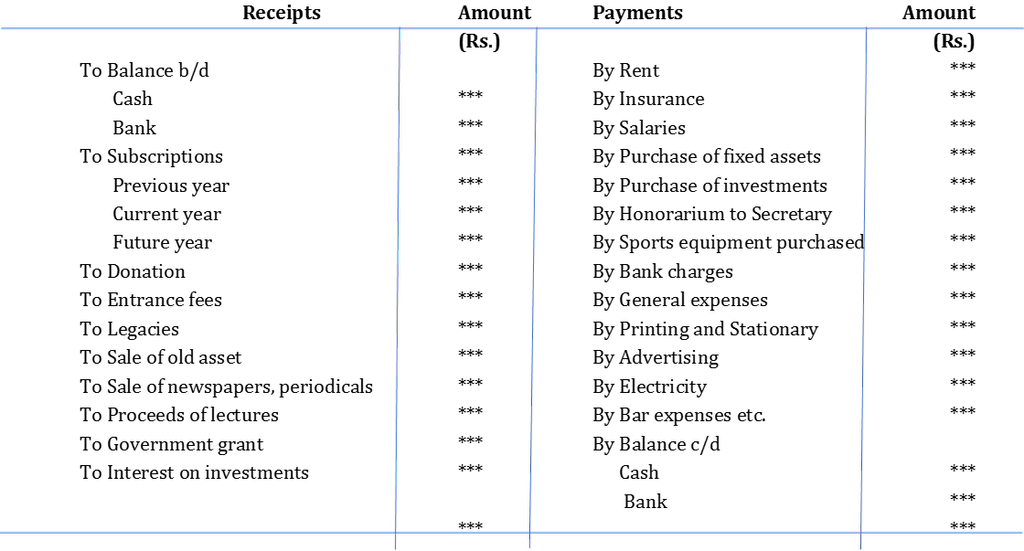

1. Receipts and Payments ACCOUNT:

The following points are noteworthy relating to Receipts and Payments A/C:

a. Receipts and Payments Account is a summary of cash transactions.

b. It shows the opening and closing balance of cash and bank, receipts and payments (both cash and cheque) and the closing cash and bank balance at the end of the accounting period.

c. The left-hand side records all receipts and the right-hand side all payments (whether revenue or capital or relating to current years past or future accounting years).

d. It shows a classified summary of cash transactions during a given period.

For example, fees may be received from the members of a club on different dates and appear on different pages of the Cash Book as it is a chronological record. But the total fees received during the accounting period is shown in the Receipts and Payments Account.

Keypoints OF RECEIPTS and Payments Account

1. It is similar to a Cash Book of a trading concern.

2. It is a real account. Receipts are recorded on the receipt side and payments are recorded on the payment side.

3. It starts with the opening cash and bank balance and closes with the closing cash and bank balance.

4. Both cash and bank transactions are merged in the same column.

5. All types of receipts are recorded on its receipts side irrespective of the nature of receipts (i.e. both capital and revenue receipts and receipts relating to past, present and future years).

6. All types of payments are recorded on the credit side irrespective of the nature of payments (i.e. both capital and revenue payments and payments relating to past, present and future years).

Format of Receipts and Payments Account:

Name of the Non-Profit Making Organisation:-

Receipts and Payments Account for the year ended **********

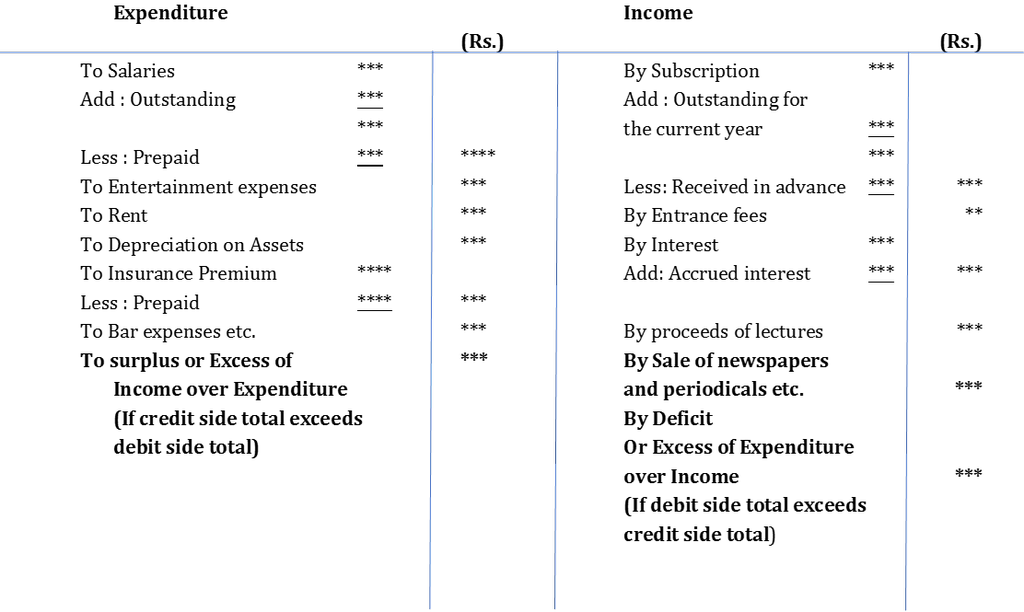

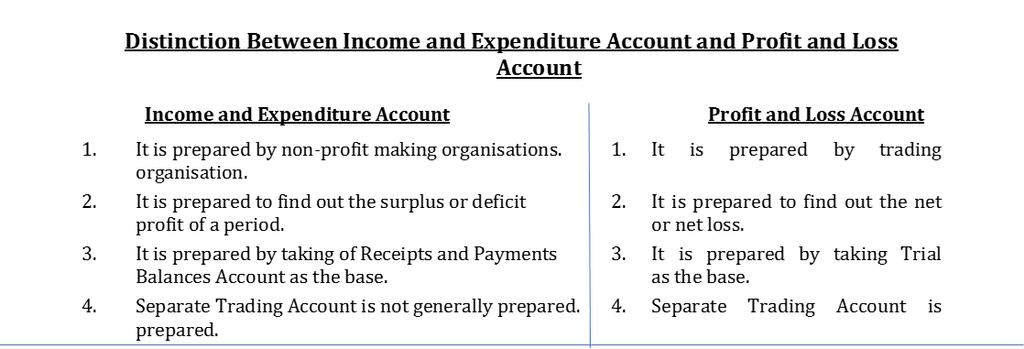

Income and Expenditure Account

Important Facts about Income & Expenditure A/C:

- Income and Expenditure Account is similar to Profit and Loss Account of a trading concern

- Since non-profit making organizations do not operate on profit objectives, income and Expenditure Account is prepared instead of preparing Profit and Loss Account.

- On the debit side, it shows all revenue expenses relating to the current year whether paid or not.

- On the credit side, it shows all revenue incomes and gains relating to the current year whether received or not.

- It is a nominal account and its preparation procedure is the same as that of a Profit and Loss Account of a trading concern.

- The balancing figure of this account is called surplus/excess of income over expenditure or deficit/excess of expenditure over income.

Key points of Income and Expenditure Account

1. It is similar to the Profit and Loss Account of a trading concern.

2. It is a nominal account. Expenses and losses are recorded on the debit side and incomes and gains are recorded on the credit side. The expenses are matched with revenues of the concerned period.

3. All revenue incomes relating to the current year whether received or due are recorded on the credit side.

4. All revenue expenses relating to the current year whether paid or outstanding are recorded on the debit side.

5. Capital expenditures and capital receipts are not recorded in this account.

6. It records both cash and non-cash items such as depreciation.

Format of Income and Expenditure Account

(Name of the Non-Profit Making Organisation)

Income and Expenditure Account

For the year ended on *********

3. Balance Sheet

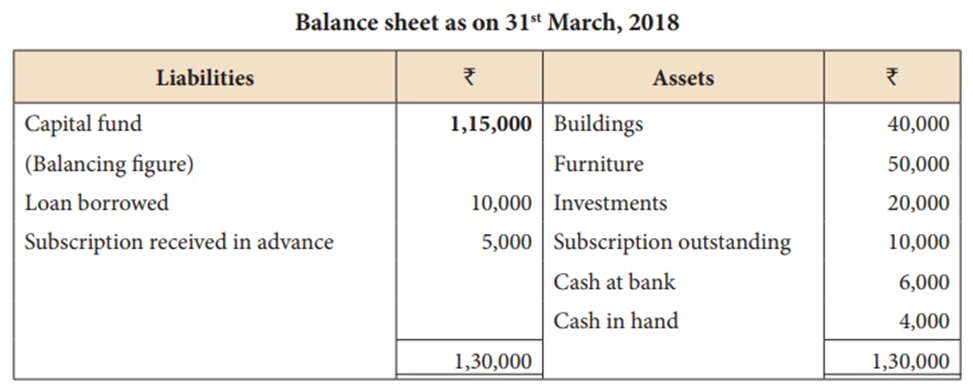

The balance sheet of a non-profit making organization is prepared on the same line as that of a trading concern. Assets including accrued income and prepaid expenses are shown on the assets side and the liabilities side shows all liabilities including outstanding expenses. Capital Fund (same as Capital Account in case of trading concerns) appears on the liabilities side. The surplus during the period is added to the Capital Fund and the deficit is subtracted.

Note: When no information regarding Capital Fund is available, it can be ascertained by preparing the Balance Sheet at the beginning of the year i.e. Opening Balance Sheet.

3. Preparation of opening & closing Balance Sheet, Some peculiar items, Incidental Trading Activity

How to Prepare Opening & Closing Balance Sheet?

Step 1 – Take into account the closing balances of assets & liabilities of the previous year & the opening balances of the Receipts & Payments A/c will be the cash in hand & cash at the bank as of that date. The Balancing Figure will be Capital Fund

Step 2 – After the preparation of the opening Balance Sheet, we shall proceed towards the preparation of the Closing Balance Sheet& for this purpose, the assets will be then adjusted for any sale or purchase during the year. Any gain or loss on the sale of assets will be taken to Income & Expenditure A/c. Any depreciation will also be taken to Income & Expenditure A/c. Only the net assets will appear on the Balance Sheet& the payments made for the purchase of new assets in the Receipts & Payments A/c shall appear as the new asset or added to the old assets.

Step 3 – From the Receipts side, any capital receipts like contributions to Building Fund & specific funds like specific donations will be recorded on the liabilities side.

Step 4 – Adjustments for prepaid & outstanding expenses will be made to the relevant expenses. Outstanding expenses & advance subscriptions will appear on the liabilities side whereas prepaid expenses & outstanding subscriptions will appear on the asset side.

Step 5 – The liabilities appearing in the previous year’s Balance Sheet should be checked with the payments made during the year. If some liabilities have been paid, then these liabilities will not appear in the new Balance Sheet to the extent they are paid. Only the net unpaid amount if any will appear on the Balance Sheet.

Step 6 – Finally, the Capital Fund balance from Opening Balance Sheet shall be adjusted with surplus or deficit from the Income & Expenditure A/c & also any specific fund which is not required anymore will be added to the Capital fund.

AN EXAMPLE OF CLOSING A BALANCE SHEET

Meaning and Treatment of Special Items

The meaning and treatment of the special items in the financial statements of non-profit making organizations are as follows:

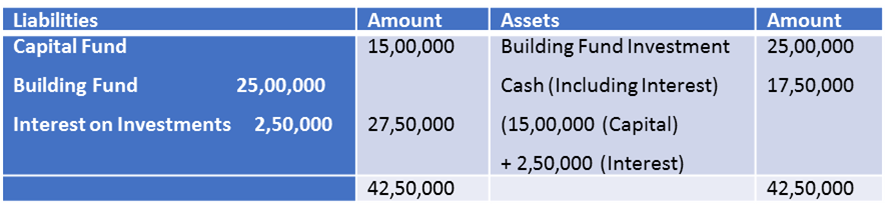

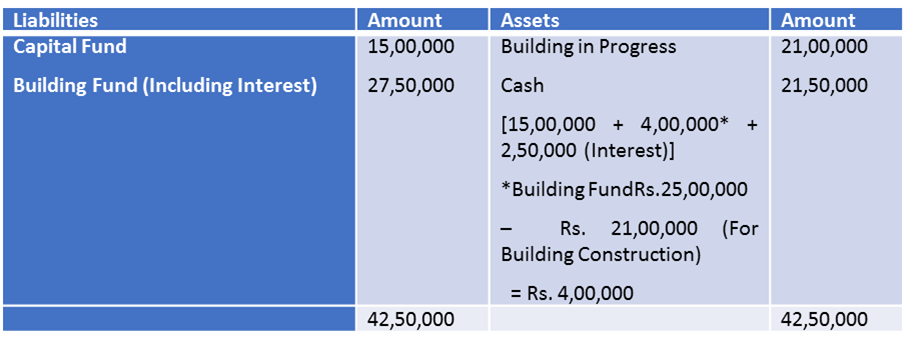

1. Capital Fund

Non-profit organizations follow FUND BASED ACCOUNTING method. In this method, the fund is of two types i.e. General Fund or Capital Fund & Specific Fund. The capital introduced is known as the General Fund or Capital Fund. It is an unrestricted fund that can be used to achieve the objectives of society. All the recurring expenses like salary and rent are charged to General Fund through Income & Expenditure A/c similarly all the revenues are added to the General Fund through Income & Expenditure A/c. If the fund money is invested somewhere then the interest earned will be directly added to the General Fund/Capital Fund.

On the other hand, Specific Fund is a restricted fund set up for a specific purpose. The money can be used only for the achievement & realization of that particular purpose. The restriction on the use of this fund is either put by the donor or by the management. If the fund money is invested somewhere then the interest earned will be directly added to the specific Fund. It is again classified into two types;

- Specific Asset Building – Funds used for building some fixed assets like Building or Pavilion.

![]()

![]()

2. Subscriptions

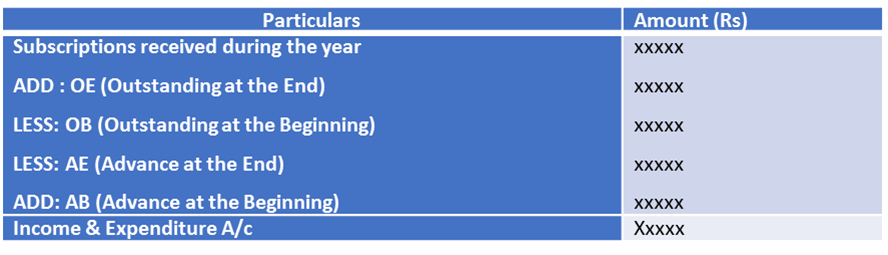

Subscriptions are collected by non-profit making organizations from their members regularly. It is revenue in nature. It is the main source of income for any non-profit making organization. Subscriptions related to the current year shall be recorded in Income & Expenditure A/c whether received or not. Subscriptions due for the current year shall also be shown in the asset side of the Balance Sheet. Subscriptions received in advance for next year shall not appear in the Income & Expenditure A/c as it is not a current year item but the amount received in advance shall be recorded as a liability in the Balance sheet as it is a prepaid income.

Explanation:-

Income& Expenditure A/c is nothing but P/L A/c with a different name. Since the purpose of preparing P/L A/c is to find out the current year's profit or loss, therefore, only current items of revenue nature is recorded in P/L A/c. In the same way, Income & Expenditure A/c also records only the current year items & items of the previous year & next year are excluded.

- Outstanding at the end shall be added as it is a current year item.

- Outstanding at the beginning shall be deducted as it is a previous year's item (last year’s closing outstanding is this year’s opening outstanding)

- Advance at the End is not a current year item. It is the membership fees received for next year in advance so it’ll be deducted from the total subscriptions received.

- Advance at the beginning is this year’s income because it represents last year’s closing advance i.e. membership fees for the current year received in advance during the previous year.

3. Donations

A non-profit making organization may receive donations from time to time. Donations received for a particular purpose like the development of a pavilion, construction of a building, awarding prizes etc. are called specific donations. A donation received not for a specific purpose is called a general donation.

Accounting Treatment: All specific donations are to be capitalized i.e. put in the liabilities side of the Balance Sheet.

If the general donation is a big amount it is to be capitalized i.e. added to the Capital Fund in the liabilities side of the Balance sheet.

In case the general donation is a small amount it is treated as income and put in the credit side of the Income and Expenditure Account.

Note: Whether the amount of general donation is big or small, it is judged by considering the nature of the activities of the non-profit making organizations.

4. Entrance Fees

This is the fee collected from the new entrants on admission to the clubs or societies etc. It is also known as admission fees.

Accounting Treatment: The entrance fees may be treated as revenue or capital depending upon the rule and by-laws of the organizations.

5. Legacies

It is a kind of gift received by a non-profit making organisation as per the will of a deceased person.

Accounting Treatment: If legacy is a small amount, it is treated as an income and is to be taken in the credit side of Income and Expenditure Account.

In case of a big amount, it should be capitalised i.e. added to Capital Fund in the liabilities side of Balance Sheet.

Note:Whether the amount of legacy is big or small, it is judged by considering the nature of activities of non-profit making organisation.

6. Life Membership Fees

Membership fees for the whole life collected from members is known as life membership fees. In this case the member is to pay a lump-sum amount instead of periodic payments and enjoys the benefits of the organisation till the end of his life.

Accounting Treatment: Life membership fees is treated as capital item and hence added to the Capital fund.

Note: However, there is another way of treatment.

It is credited to a separate fund (Life Membership Fees Account) and an amount equal to the annual membership fee (subscription) is transferred to the Income and Expenditure Account. The balance in the separate fund is shown in the liabilities side of the Balance Sheet. If a life member dies, then the balance lying in the special fund is transferred to the Capital Fund of the organization.

7. Special Fund

Sometimes a non-profit making organisation may create funds for some special purposes. For example, a sports club may create Tournament Fund for meeting tournaments expenses or a building fund for the construction of building etc.

Accounting Treatment: The fund may be invested in banks or in Govt. securities.

- Any income relating to such special fund is added to this fund.

- Any expenditure on account of this fund is subtracted from such fund.

- Such special fund appears in the liabilities side of Balance Sheet.

- If there is deficit (the expenditure on account of fund is more than the amount of fund) it is recorded in the expenditure side of Income and Expenditure Account.

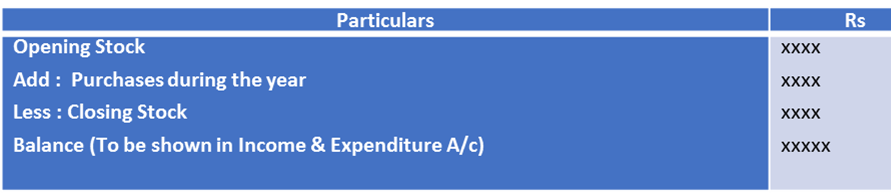

8. Calculation of Cost of Consumable Goods – Consumable goods are the items that are used or consumed during the year such as sports material, stationery, books, medicines, and food items. In the Income & Expenditure A/c, only the amount of such items consumed will during the year be shown. Therefore, it is necessary to find out the cost of consumption of such goods.

STEPS TO PREPARE INCOME & EXPENDITURE A/C FROM RECEIPTS & PAYMENTS A/C

- Prepare the Opening Balance Sheet to find out the opening balance of Capital Fund (if it is not given).

- Identify the revenue receipts from the receipts side of Receipts & Payment A/c & show them in the Income side of the Income & Expenditure A/c. Capital receipts will be shown in the Balance sheet.

- Identify the Capital expenditure from the payment side of Receipts & Payment A/c & show it in the Balance sheet. Capital items won’t appear in Income & Expenditure A/c.

- Certain items do not appear in Receipts & Payment A/c but shall be recorded in Income & Expenditure A/c such as depreciation of fixed assets, loss on sale of fixed assets, and profit on the sale of fixed assets. Depreciation & loss shall be shown in the Expenditure side whereas profit on the sale of fixed assets shall be shown in the Income side.

- Finally, find out the surplus or deficit i.e. if the income side is higher it is surplus & if the expenditure side is higher then it is a deficit.

- Prepare Closing Balance Sheet by taking into consideration the opening balance of assets & liabilities, surplus/deficit, purchase & sale of assets during the year & depreciation on fixed assets. The surplus shall be added to the Capital whereas the Deficit shall be deducted from the Capital.

INCIDENTAL TRADING ACTIVITY

This Incidental Trading activity is also known as incidentals, these are the gratuities and the fees or costs which are incurred in addition to the main item, service or event paid for during the trading pursuits.

Trading pursuits like a hospital or a chemist shop or even a beauty parlor or canteen, all these places can also in use to furnish certain provisions to the members or public. In this scenario, the trading A/c has to be drawn to determine the outcome of this incidental pursuit. The profit from these trading pursuits is solicited to accomplish the primary objectives which satisfy the cause for which the establishment was set up, then it is transferred to the Income and Expenditure A/c.

In Relation to the Above, the following are the Details:

- The trading A/c has to be outlined to ascertain either profit or loss due to incidental commercial pursuit. All these costs and revenues in a straight way and principally are associated with such pursuits, are documented in the trading A/c. After this, the Balance of the trading A/c is being transferred to the Income and Expenditure A/c

- Income and Expenditure A/c documents, also the trading profit (or loss), and all other incomes and expenses are not documented in the Trading A/c. Surfeit or deficit is disclosed by the Income and Expenditure A/c as is being transferred to the capital or general fund.

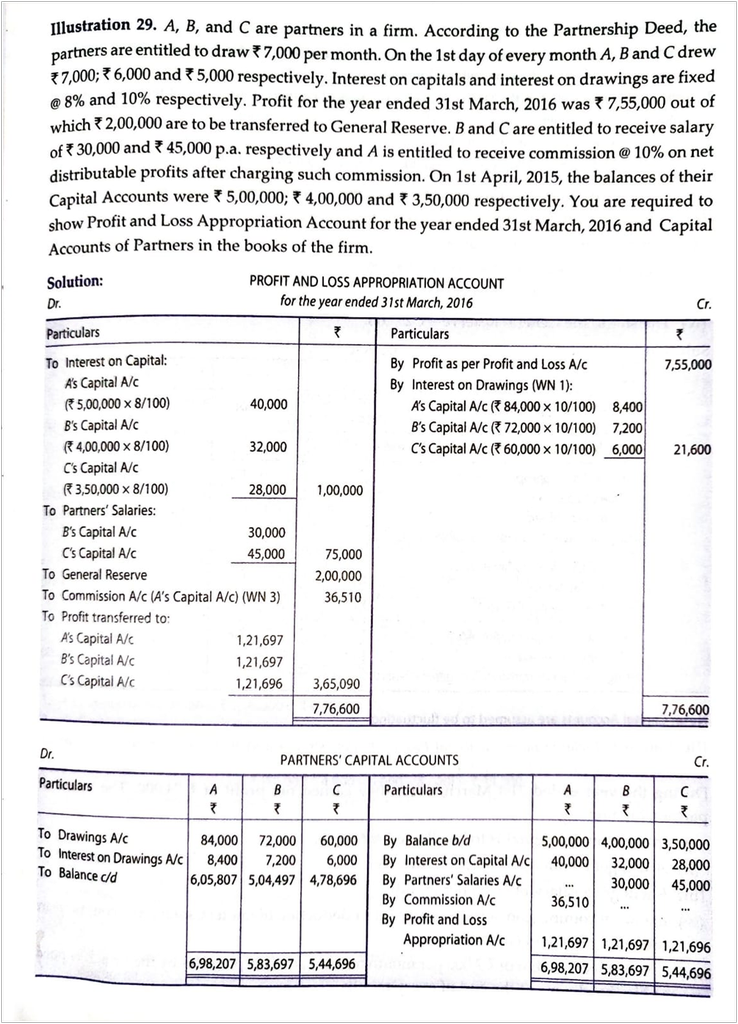

2. Maintenance of capital accounts, Distribution of profit among the partners

MAINTENANCE OF CAPITAL ACCOUNTS& DISTRIBUTION OF PROFITS AMONG THE PARTNERS

To record the changes in Capital A/c of each partner, we prepare individual capital accounts for each partner. The capital accounts of partners can be maintained in two methods :

Fixed Capital Method

Fluctuating Capital Method

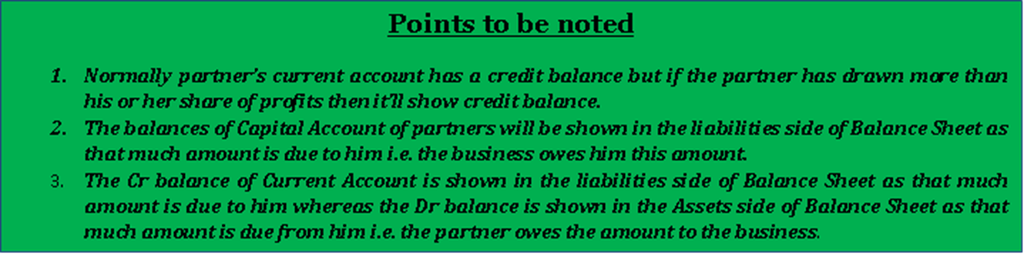

- Fixed Capital Method – In this method, the capital A/c of partners remains unaltered or fixed. When this method is followed, two accounts i.e. Capital A/c & Current A/c for each partner are maintained.

- Capital A/c – The capital account remains unaltered i.e. fixed unless additional capital is introduced or withdrawal is made from the existing capital. If there is no fresh capital introduced or any withdrawals, the capital account of the partner show the same balance year after year.

- Current A/c – It is prepared to record transactions other than introduction & withdrawal of capital such as interest on capital, interest on drawings, salary or commission to a partner, and share of profits/losses. The balance of current account always keeps fluctuating because of these adjustments.

Current A/c is debited with;

- Drawings made by partner

- Interest on drawings

- Share of loss

- Transfer of amount to any capital account permanently

Current A/c is credited with;

- Interest on capital

- Salary or commission

- Share of profits

- Transfer of any amount from capital account permanently

- Fluctuating Capital A/c – Under Fluctuating Capital method, only one account namely Capital A/c is maintained for each partner. All the transactions of a partner like salary, commissions, interest on capital are recorded in this account. As a result of this, the capital a/c fluctuates with every transaction. The debit balance of capital account is shown in the liabilities side & the credit balance is shown in the asset side.

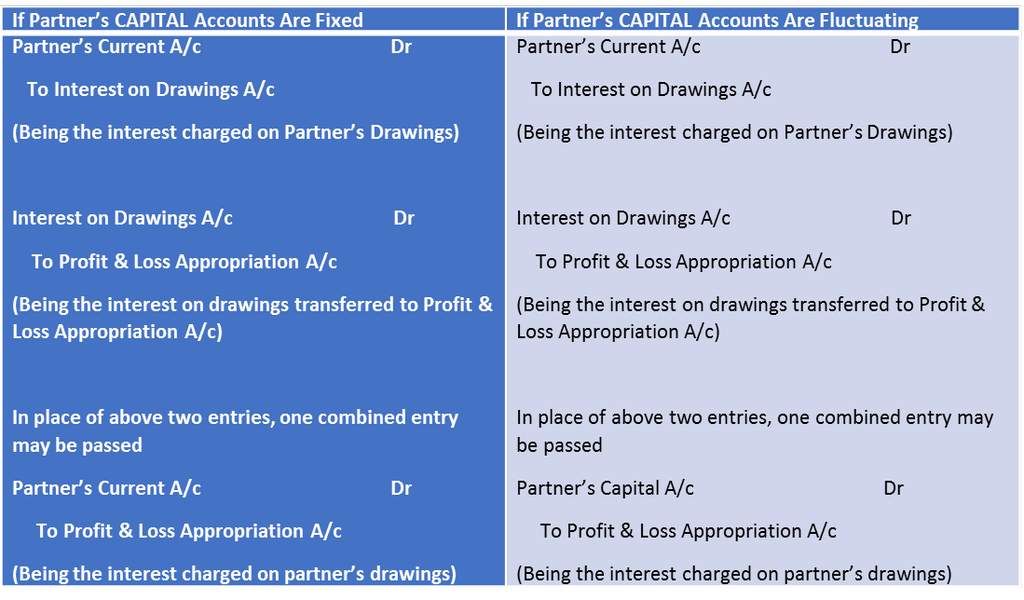

INTEREST ON DRAWNGS

- Drawings refers to the amount withdrawn by the owner in cash or in kind.

- Interest on drawings is charged only when it is mentioned in the partnership deed.

- When it is charged, it is debited to Profit & Loss Appropriation A/c.

- It is either debited to Partner’s Capital A/c or Current A/c depending on whether Fixed Capital or Fluctuating Capital method is being followed

INTEREST ON DRAWINGS : - HOW IT IS CALCULATED?

- The computation of Interest on Drawings depends upon various factors like when the amount is withdrawn & the time period for which it remains withdrawn etc.

- So, the situations can be as follows;

- Fixed amount is withdrawn at the BEGINNING of every Month

If a partner withdraws fixed amount in the beginning of every month, interest is charged on the whole amount for 6 ½ months

Interest on Drawings = Total Drawings X Rate of Interest X 6 ½ 100 12

6 ½ months = Average Period

Average Period Formula = Time left after first drawings + Time left after last drawings 2

- Average period should be used only when the amount of Drawings is uniform & the time interval between the two consecutive drawings is also uniform.

- Fixed amount is withdrawn at the END of every Month.

If a partner withdraws a fixed amount at the end of every month, interest is charged for 5 ½ months.

Interest on Drawings = Total Drawings X Rate of Interest X 5 ½ 100 12

- Fixed amount is withdrawn in the MIDDLE of every Month

Interest on Drawings = Total Drawings X Rate of Interest X 6 100 12

- Fixed amount is withdrawn at the BEGINNING of every QUARTER

Interest on Drawings = Total Drawings X Rate of Interest X 7 ½ 100 12

- Fixed amount is withdrawn in the MIDDLE of every QUARTER

Interest on Drawings = Total Drawings X Rate of Interest X 6 100 12

- Fixed amount is withdrawn at the END of every QUARTER

Interest on Drawings = Total Drawings X Rate of Interest X 4 ½ 100 12

- Fixed amount is withdrawn during 6 MONTHS

- At the BEGINNING OF EACH MONTH

Interest on Drawings = Total Drawings X Rate X 3 ½

100 12

- In the MIDDLE OF EACH MONTH

Interest on Drawings = Total Drawings X Rate X 3

100 12

- At the END OF EACH MONTH

Interest on Drawings = Total Drawings X Rate X 3 ½

100 12

- If Unequal amount is withdrawn at DIFFERENT DATES, interest on drawings is calculated on the basis of the Simple Method or Product Method

Interest on Drawings = Total of Product X Rate of Interest x 1 or 1 100 12 365

- When the date of withdrawal IS NOT GIVEN, the interest on drawings is calculated for six months on an average basis.

- When Rate of Interest is given without the word PER ANNUM, interest is charged without considering the time factor

Journal Entries to Record Interest on Drawings

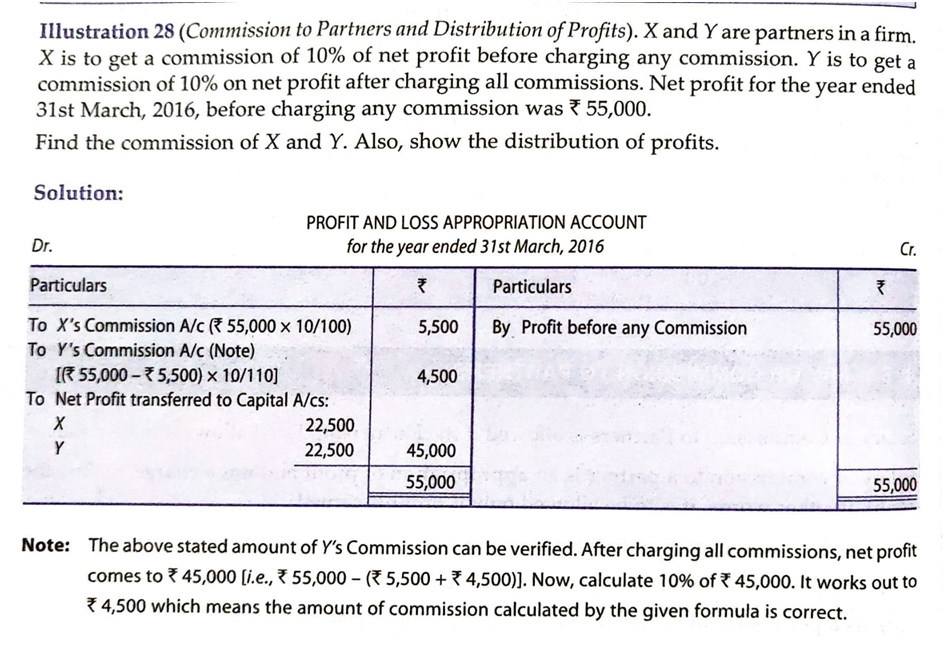

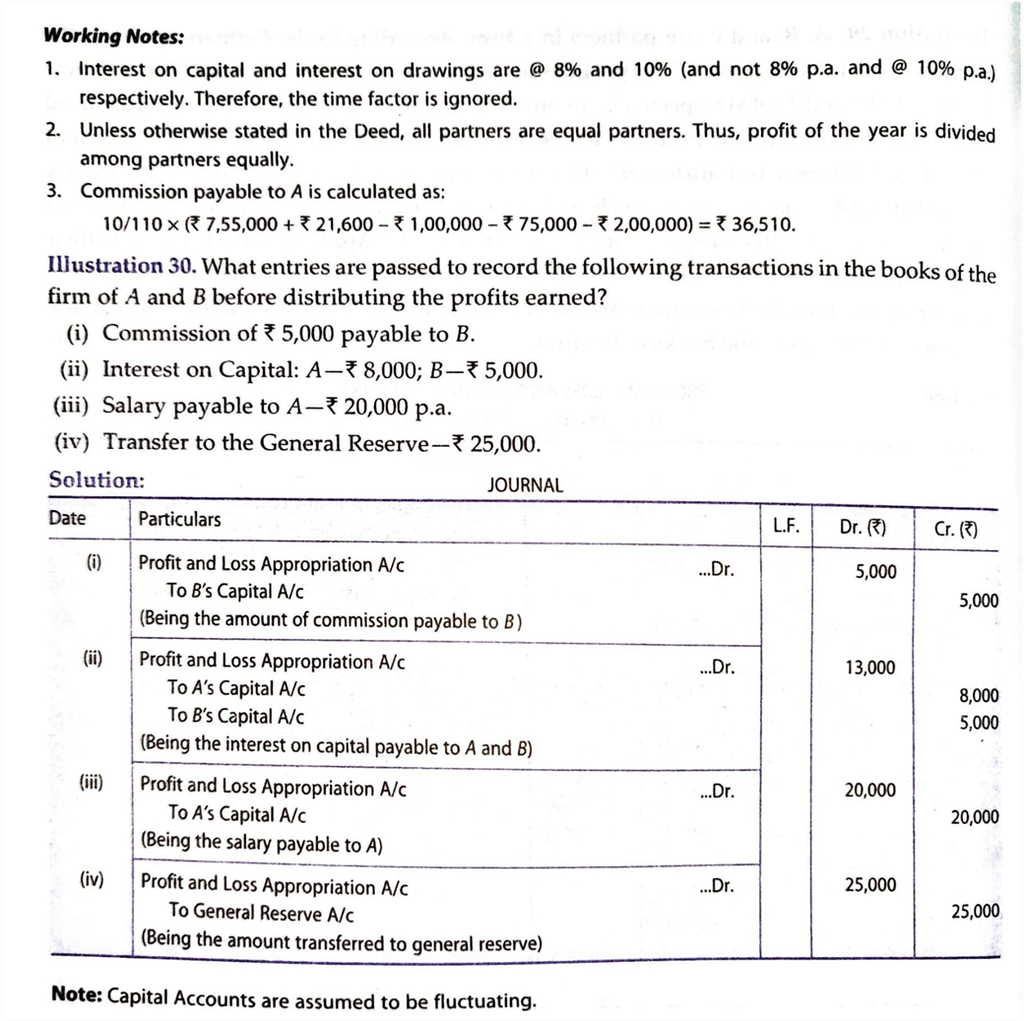

Salary or Commission to Partners

- Salary or commission to partners is paid only when it is allowed in Partnership Deed

- It is an appropriation of profit & not charge against the profit so it should be allowed only when profit is earned

- Commission may be allowed to the partners either

- As a percentage of profit before charging such commission

Net Profit (before Commission) x Rate of commission

100

or

- As a percentage of profit after charging such commission

Net profit (before commission) x Rate of Commission

100+Rate of Commission

Accounting Treatment:-

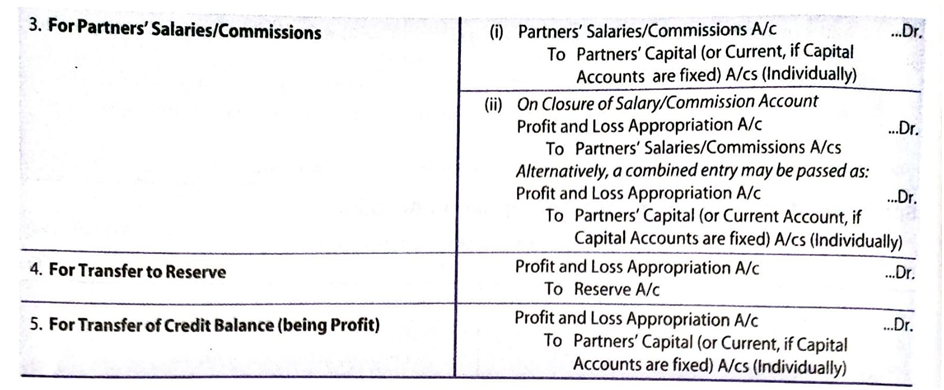

Partner’s Salaries/ Commission A/c Dr

To Partner’s Current A/c (When capitals are fixed)

To Partner’s Capital A/c (When capitals are fluctuating)

Profit & Loss Appropriation A/c Dr

To Partner’s salaries/commission A/c

Interest on Partner’s Loan to the Firm

- If a partner apart from investing share capital, advances any loan to the firm then he is entitled to receive interest even in the absence of an agreement/deed.

- In the absence of an agreement/deed, the minimum rate of interest on loan to be paid to the partner is 6% p.a.

- Interest on loan is a charge against profit & it is transferred to the debit of Profit/Loss A/c & not to the debit of Profit/Loss Appropriation A/c

- Journal Entries

- Interest on partner’s loan A/c Dr

To Partner’s Loan A/c

- Profit & Loss A/c Dr

To Interest on partner’s loan A/c

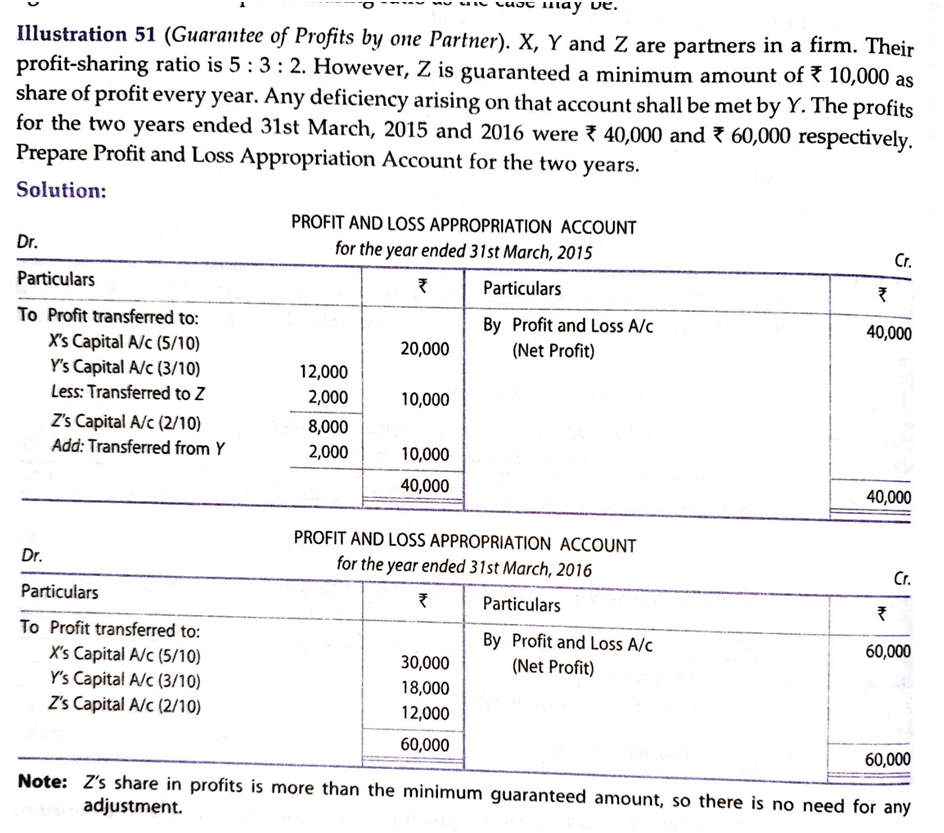

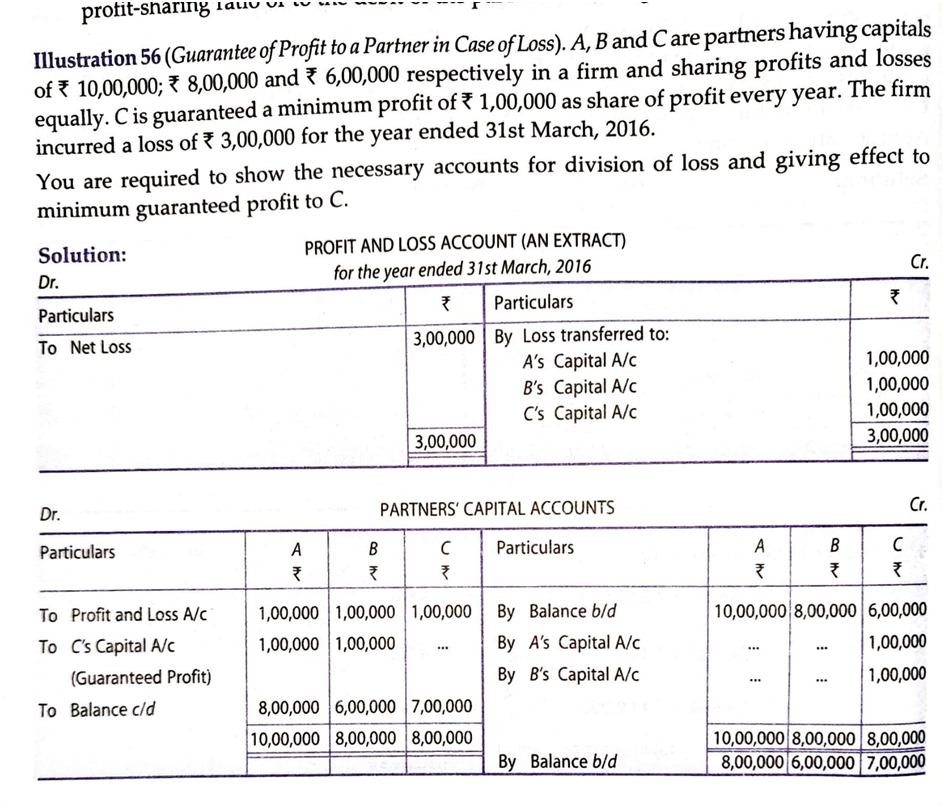

3. Guarantee of profit to a partner, Past adjustments, Final accounts

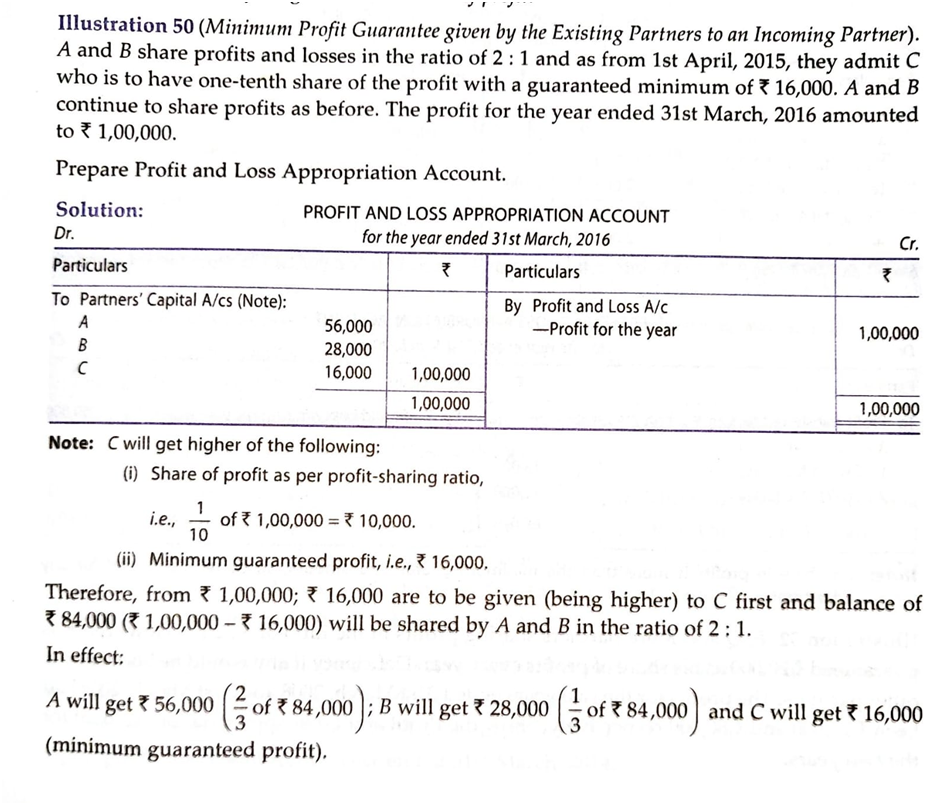

Guarantee of Profit

- In some cases, a partner may be admitted in the firm on a guarantee in respect of his minimum profit from the business.

- Such a guarantee may be given to an existing partner as well.

- Such a guarantee to the incoming partner is given ;

- All the old partners in agreed ratio

- Some of the old partners

When all the partners guarantee that one of the partners shall be given a minimum amount of profit, the following amounts have to be calculated separately

- Share of profit as per profit sharing ratio

- Minimum Guaranteed Profit

- The minimum of the above two is given to that partner & the balance of profit (i.e. total profit – profit given to the guaranteed partner) is shared by the remaining partners in the profit-sharing ratio.

- If the partner’s actual share of profit turns out to be more than the guaranteed profit then in that case the partner will be given the actual amount instead of the guaranteed amount.

- When one or more than one partner guarantees a minimum profit, the adjustment is made through the partner’s capital accounts. The following steps are followed;

- Distribute the profit among the partners in their profit sharing ratio

- If the share of the guaranteed profit of the partner falls short of the minimum amount then the difference is deducted from the original share of profit of the partners who guarantee & it is added with the original share of profit of the guaranteed partner.

- When two or more partners give guarantee, the shortfall is shared by them in the agreed ratio or in their profit-sharing ration as the case may be.

- Accounting Treatment of Guarantee of Profit in case of Loss

- Sometimes it is possible that the firm has incurred losses but the guaranteed profit is to be paid to the partner who has been guaranteed minimum profit. In such a case, the adjustment has to be made through partner’s capital A/c in the following manner;

- Distribute the loss among the partners in their profit sharing ratio

- Capital A/c of the guaranteed partner is credited with guaranteed minimum profit plus the amount of loss. This amount is debited to remaining partners in their profit sharing ratio or to the debit of the partner who has guaranteed minimum profit.

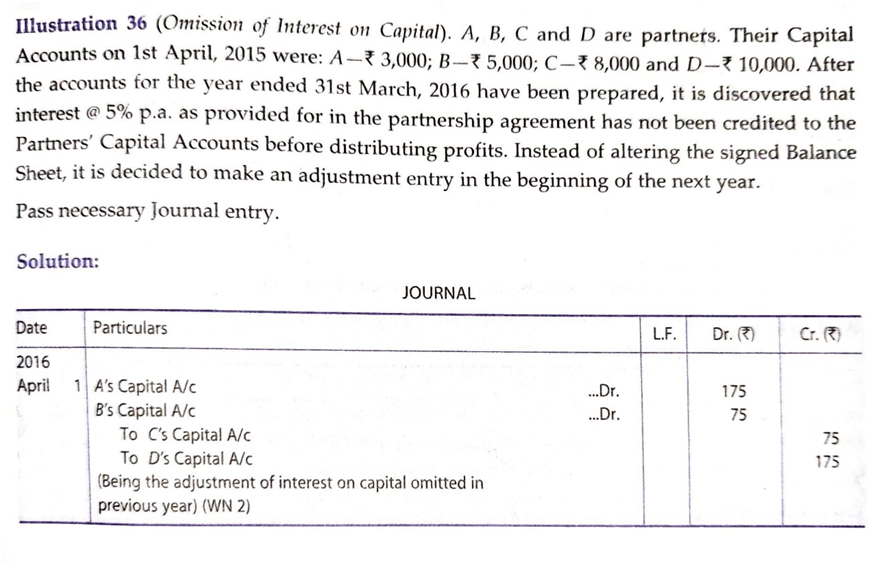

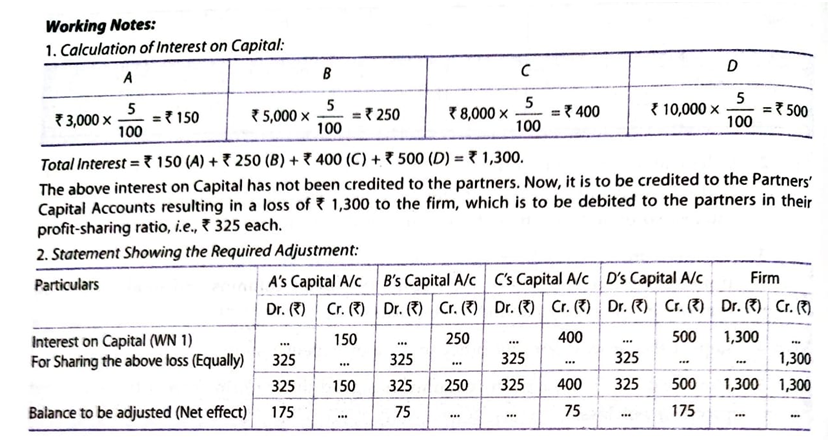

Past Adjustments

Sometimes, after the final accounts of a firm have been closed, it is found that certain matters have been left out by mistake. In such cases, instead of altering the final accounts which have already been closed, the firm rectifies the error or omission by passing an adjustment entry in the beginning of the financial year. Such adjustments are called past adjustments as they relate to the past.

Steps to pass adjusting journal entry:

Step 1 Calculate the amount already recorded.

Step 2 Calculate the amount which should have been recorded.

Step 3 Calculate the difference between Step 1 and Step 2.

Step 4 Find out the partner who received excess and the partner who received short.

Step 5 Pass the adjusting journal entry by debiting the partner who received excess and by crediting the partner who received short.

PREPARATION OF FINAL ACCOUNTS OF PARTNERSHIP FIRM

Final accounts of a partnership firm are prepared in the usual way in which they are prepared for a sole proprietorship concern except that the profits in the partnership have to be distributed among the various partners according to the terms of the partnership contract and the amount of profit may be arrived at after making adjustments for interest on capital, interest on drawings, salaries to partners, etc. for this another account “Profit & Loss Appropriation Account” is prepared after preparing Profit & Loss Account.

The final accounts prepared by partnership firms are:

a) Manufacturing account – if manufacturing activity is carried on

b) Trading and profit and loss account – to ascertain profitability

c) Profit and loss appropriation account – to show the disposal of profits and surplus

d) Balance sheet – to ascertain the financial status.

1. Modes of reconstitution of a partnership firm, Admission of a new partner

(MODES OF RECONSTITUTION)

A partnership firm may go for reconstitution for various reasons such as;

- Change in the profit-sharing ratio among the Existing Partners.

- Admission of a Partner.

- The Retirement of an Existing Partner.

- Death or Insolvency of a Partner.

ADMISSION OF A PARTNER

- Admission of a partner is one of the modes of reconstitution of partnership firm because when a new partner is admitted, the existing agreement among the partners comes to an end & a new agreement comes into existence which results in change in profit sharing ratio, goodwill valuation & reassessment of assets & liabilities.

- The capital contribution of the new partner, his liabilities, and share of profits is decided upon.

- As per Section 31 of the Indian Partnership Act, the new partner shall not be admitted to the firm without the consent of all existing partners.

- After admission, the new partner gets the following two rights :

- Right to share future profits of the firm

- Right to share in the assets of the firm

- He/she also becomes liable for any liability of the business incurred after admission & any loss incurred by the firm

- The new/incoming partner receives share in future profits that is equal to the sacrifice of profit by an existing partner/partners of the firm & the same new partner has to compensate the partner/partners who are sacrificing their share in profits in his/her favor.

- Such amount paid by the incoming partner is known as Goodwill or Premium for Goodwill.

- Besides Goodwill/Premium for Goodwill, the new partner also contributes in Capital to get the rights in the assets of the firm.

Effects of Admission of Partner

- Old partnership agreement comes to an end & a new agreement is formed.

- New or incoming partner becomes entitled to the future share of profits & losses of the firm.

- New or incoming partner contributes an agreed amount of capital in the firm.

- New or incoming partner gets a right to the assets of the firm.

- Adjustments are made regarding the accumulated profits & losses

- Assets are revalued & liabilities are reassessed & the net change is adjusted in existing or old partner’s capital accounts in their old profit sharing ratio.

- Goodwill of the firm is valued in order to pay the sacrificing partner for their sacrificed share by the gaining partners through their capital accounts.

What are the adjustments required on the admission of a partner?

- Determining new profit sharing ratio

- Valuation of adjustment of goodwill

- Adjustment of profit/loss arising from revaluation of assets & reassessment of liabilities.

- Adjustments of accumulated profits, reserves & losses.

- Adjustment of capital (if agreed)

1. Dissolution of partnership, Dissolution of firm

Dissolution of Partnership & Dissolution of Firm are not the same thing. Whenever there is a change in constitution of the firm, the business of the firm continues. There is a change in constitution in case of admission, retirement & death of a partner. This change leads to dissolution of partnership & not dissolution firm. The relationship between the partners changes but the overall business of the firm continues as usual. However, in the case of dissolution of partnership firm, both the partnership & the business comes to an end. Dissolution of the firm is the end of partnership business. Dissolution of partnership occurs due to the following reasons;

- Due to the admission of a new partner

- Due to the retirement of a new partner

- When a partner is declared insolvent

- When the profit-sharing ratio is changed

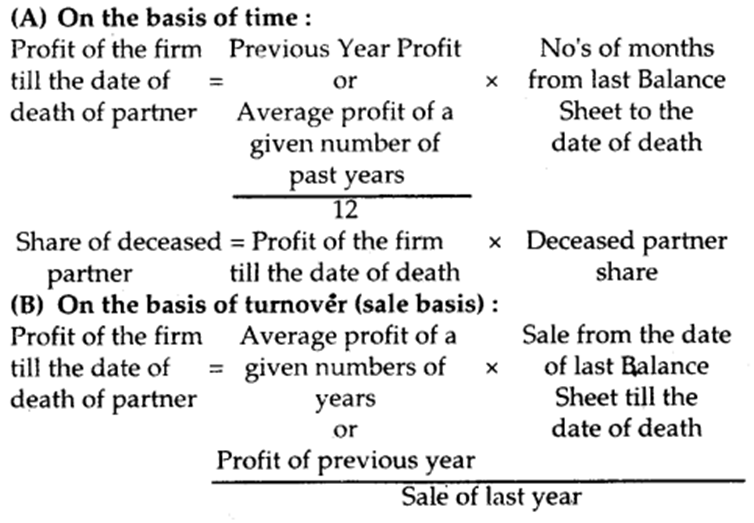

1. Ascertaining the amount due to the retiring or deceased partner, New profit sharing ratio, Gaining ratio,

Reconstitution of the partnership firm can also take place on the retirement of the partner or death of the partner. Here, the existing partnership deed comes to an end a new partnership deed comes into existence where the remaining partners continue to do the business but on different terms and conditions. In both cases, i.e. on retirement or death of a partner, it is required to determine the sum due to the retiring partner or to the legal representatives of the deceased partner.

Retirement of a Partner:

A partner may retire from the partnership firm:

- with the consent of all other partners;

or - in case of retirement at will i.e. (partnership at will);

or - by giving notice in writing to all other partners by the retiring partner.

On retirement, the old partnership comes to an end arid a new one between the remaining partner1 comes into existence. However the partnership firm as such continues.

Ascertaining the Amount due to Retiring Partner

In order to ascertain the amount due to the retiring partner, we have to calculate the following things

- Credit Balance of his Capital Account;

- Credit Balance of his Current Account (if any);

- His share of goodwill, accumulated profits, reserves etc.;

- His share in the profit on revaluation of assets and liabilities;

- His share of profit, interest on capital up to the date of retirement;

- Any salary/commission due to him.

The following deductions (if any) is made from his share:

- Debit balance of the his-current account (if any);

- His share of Goodwill to be written off, accumulated losses;

- His share of loss on revaluation of assets and liabilities;

- His share of loss, drawing and interest on drawings up to the date of retirement.

The various accounting aspects involved in retirement or death are as follows:

- New profit sharing ratio

- Gaining ratio

- Goodwill Treatment

- Accumulated profit and losses -Distribution

- Profit and Loss till the date of retirement or death

- Adjustment of Capital

- Settlement of the amount due to retired /deceased partner.

New Profit Sharing Ratio:

The new profit sharing ratio is the ratio in which the remaining partners will share future profits after the retirement or death of any partners. In other words, the new profit sharing ratio of each remaining partner will be the sum total of his old share of profits in the firm and the portion of the retiring partner’s share of the profit acquired.

New Share of Partner = Old share + Acquired share from retiring/deceased partner.

(a) Nothing is mentioned about the new profit sharing ratio at the time of retirement:

If nothing is stated about the future ratio of the remaining partner, then their old ratio is considered as their new ratio. In other words, in the absence of any information regarding the profit-sharing ratio in which the remaining partner acquires the share of the retiring/deceased partner, then it is assumed that they will acquire it in the old profit-sharing ratio and so the share the future profits in their old ratio.

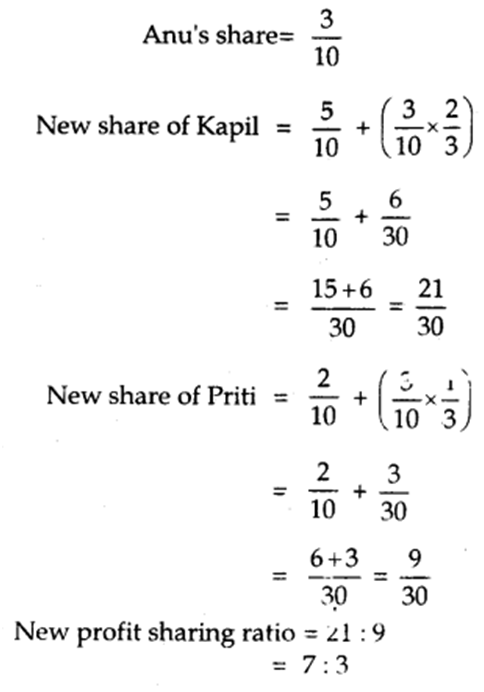

For example, Kapil, Anu and Priti are partners in a firm sharing profits and losses in the ratio of 5: 3: 2. If Anu retires, then the new profit sharing ratio of Kapil and Priti will be 5: 2.

(b) Remaining partners acquire the share of retiring/deceased partner in the specified ratio:

If the remaining partners acquire the share of the retiring/deceased partner in a specified ratio, other than their old ratio, then there is a need to compute a new profit sharing ratio among them. The new profit sharing ratio is equal to the sum total of their old ratio and the share acquired from the retiring/deceased partner.

For example, Kapil, Anu and Priti are partners in a firm sharing profits and losses in the ratio of 5: 3: 2. If Anu retires from the firm and her share was acquired by Kapil and Priti in the ratio of 2: 1. In that case, the new share of profit will be calculated as follows: New share of remaining partner = Old share + Acquired share from the outgoing partner.

(c) Remaining partners may agree on a particular new profit sharing ratio:

If the remaining partners decide on a particular profit sharing ratio to share the future profits of the firm, in such a case the ratio so specified will be the new profit sharing ratio.

Gaining Ratio:

The ratio in which the continuing partners acquire the share of the retiring /deceased partner is called the gaining ratio.

(a) If nothing is mentioned in the agreement: If nothing is mentioned in the agreement about the gaining ratio, then it is assumed that the remaining partners acquire the share of the retiring/deceased partner in their old profit sharing ratio. In that case, the gaining ratio of the remaining partners will be the same as their old profit sharing ratio and there is no need to compute the gaining ratio.

(b) If a new profit sharing ratio is given: If the new profit sharing ratio is given of the remaining partners then we have to compute the gaining ratio. In this case, the gaining ratio is calculated by deducting the old ratio from the new ratio.

Gaining ratio = New ratio – Old ratio

For example X, Y and Z are partners in a firm, sharing profits and losses in ratio of 5:3:2. Y retires from the firm and X and Z decide to share future profits and losses in the ratio of 7: 5

The gaining ratio will be calculated as follows:

2. New profit sharing ratio, Sacrificing Ratio

Determination of New Profit Sharing Ratio

The new or incoming partner is entitled to the share of future profits & losses of the firm. Therefore, there will be a change in the existing profit sharing ratio of the old partners since the new partner will acquire his/her share from the existing share of old partners. The new or incoming partners may acquire the share from the old partner in the following ways;

- In their old profit-sharing ratio

- In a particular ratio or surrendered ratio

- In a particular fraction from some of the partners

Let us discuss in detail;

- When a new partner acquires his share from old or existing partners in their old profit sharing ratio;

In this situation, the share of the new partner is given & it is assumed that the new partner has acquired his share from old partners in their old profit sharing ratio. Old partners continue to share the balance profits & losses in their old profit-sharing ratio. Unless otherwise agreed, the profit-sharing ratio of the existing partners remains unchanged & the new profit sharing ratio is determined by deducting new or incoming partner’s share from 1 & then dividing the balance in old profit sharing ratio of the old partners.

- When share of the New partner is given & new ratio of Old Partners is also given;

In this case, the new partner’s share is deducted from 1 & the balance is divided among old partners in their new ratio. Hence, there is a new profit-sharing ratio for all the partners.

- When New or Incoming Partner acquires his share from old or existing partners in a particular ratio;

In such a case, the new or incoming partner acquires a part of share of profits from one partner & a part of share of profits from another partner. The existing partner’s share will change to the extent of share sacrificed on admission of new partner.

- When new or incoming partner acquires his shares by surrender of particular fraction of their shares by the old or existing partners;

In such a case, the shares surrendered by the old partners in favor of the new partners are added & it becomes the share of the new partner. The shares surrendered by the old partners is deducted from their respective share to determine old partner’s share in the reconstituted firm.

The Concept of Sacrificing Ratio

Sacrificing ratio can be explained as the ratio in which existing or old partners sacrifice their share of profits in favor of the new or incoming partner. It can also be defined as the ratio in which the new partner is given a share by the existing partners. This share can be given by all the partners equally or by some of the partners in agreed share. Sacrificing ratio determines the compensation that new partner should pay to the old partners for the share of profits sacrificed by them. The following can be the situations under which sacrificing ratio is determined;

- When the share of new or incoming partner is given without giving the details of the sacrifice made by the old or existing partners

In this situation, there is no change in the profit sharing ratio of old partners because it is assumed that the partners make sacrifices in their old profit sharing ratio & for that reason sacrificing ratio is always in the old profit sharing ratio.

- When the old ratio of old or existing partners & new ratio of all the partners are given

In this case, the sacrificing ratio is the difference between the old ratio & the new ratio.

- When new or incoming partner acquires the share by surrendering a particular fraction of shares by old partners

In such a case, the shares surrendered by the old partner in favor of the new partner are added & it becomes the share of the incoming or new partner. The shares so surrendered by the old partner is deducted from his old share to find out his share in the reconstituted firm.

3. Goodwill - Meaning, Nature & Valuation

Goodwill:

Goodwill is the value of the reputation of a firm. In other words, a well-established business develops the advantage of a good name, reputation and wide business connections. This helps the business to earn more profits as compared to newly set-up businesses. This advantage in monetary terms is called ‘Goodwill’ & it arises only if a firm is able to earn higher profits than normal.

“Goodwill may be said to be that element arising from the reputation, connections or other advantages possessed by a business which enable it to earn greater profits than the return normally to be expected on the capital represented by the net tangible assets employed in the business.” – Spicer and Pegler

Characteristics of Goodwill:

- Goodwill is an intangible asset

- It is a valuable asset. It helps in earning higher profits than normal.

- It is very difficult to place an exact value on goodwill. It is fluctuating from time to time due to changing circumstances of the business.

- Goodwill is an attractive force that brings in customers.

- Goodwill comes into existence due to various factors.

Factors Affecting the Value of Goodwill

1. Nature of business: Company produces high value-added products or has stable demand in the market. Such a company will have more goodwill and is able to earn more profits.

2. Location: If a business is located in a favorable place, it will attract more customers and therefore will have more goodwill.

3. Efficient Management: Efficient Management brings high productivity and costs efficiency to the business which enables it to earn higher profits and thus more goodwill.

4. Market Situation: A firm under monopoly or limited competition enjoys high profits which leads to a higher value of goodwill.

5. Special Advantages: A firm enjoys a higher value of goodwill if it has special advantages like import licenses, low rate and assured supply of power, long-term contracts for sale and for purchase, patents, trademarks etc.

6. Quality of Products: If the quality of products of the firm is good and regular, then it has more goodwill.

Valuation of Goodwill: Why is it needed?

- At the time of sale of a business;

- Change in the profit-sharing ratio amongst the existing partners;

- Admission of a new partner.

- Retirement of a partner;

- Death of a partner;

- Dissolution of a firm;

- The amalgamation of the partnership firm

Methods of Valuation of Goodwill: There are various methods for the valuation of goodwill in the partnership business. The value of goodwill may differ in different methods. Goodwill is an intangible asset, so it is very difficult to calculate its exact value. As per the money measurement concept of Accounting, anything that cannot be measured in terms of money should not be recorded in books of accounts. Therefore, it is important to convert Goodwill into monetary terms to record it in the books of accounts. The methods followed for valuing goodwill are:

- Average Profit Method

- Super Profit Method

- Capitalisation Method.

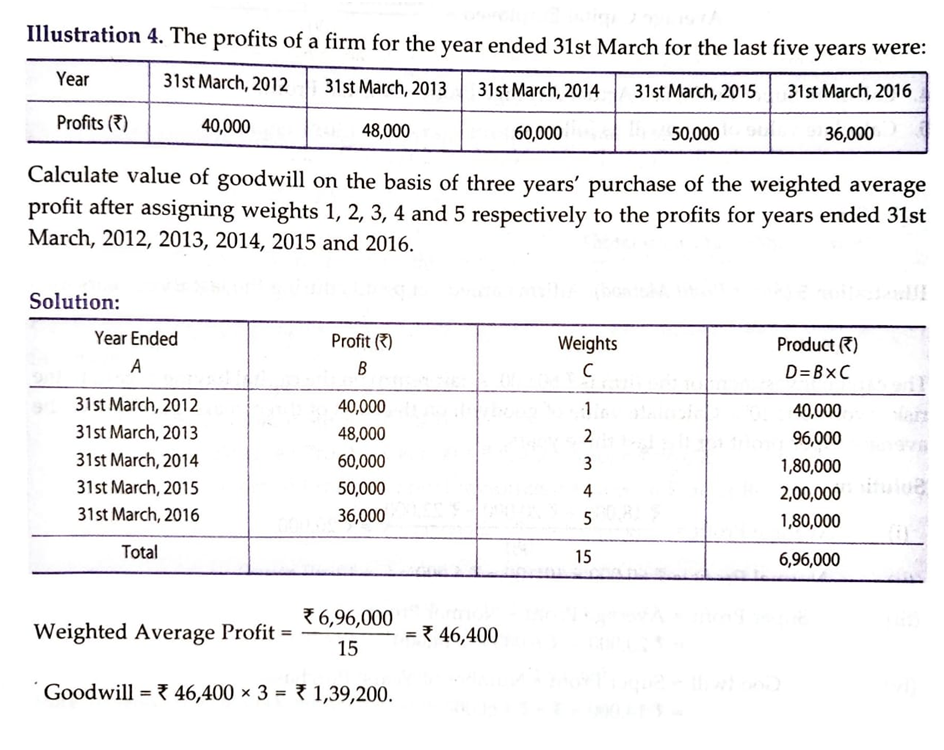

1. Average Profit Method: In this method, Goodwill is calculated on the basis of the number of past years profits. In this method, the goodwill is valued at an agreed number of years purchase of the average profits of the past few years. A number of years purchase means the period for which the business would be able to earn profit only on the basis of the Goodwill of the business.

There are two different methods of calculating average profit which are:

1. Simple average

2. Weighted average

Simple Average: In the simple average method, the goodwill is calculated by multiplying the average profit with the agreed number of years of purchase.

Step 1 – Find out normal profit by deducting abnormal gains & non-business incomes & adding abnormal losses & non-business expenses.

Step 2 – Average Profit = Total Profits/Number of years of profit & loss given

Step 3 - Goodwill = Average Profit x No. of years of purchase

Example of Simple Average Profit Method

The following illustration will help in understanding the concept of Average Profit method more clearly.

ABC & Co. has these profits in the following years

2010 – ₹5000

2011- ₹4000

2012- ₹5000

2013- ₹3000

2014- ₹5000

Calculate the goodwill at 4 years of purchase.

Solution

Average Profit = Total Profit / No.of years

= 5000+4000+5000+3000+5000

= 22000/5

= 4400

Goodwill = Average Profit x No. of years of purchase

= 4400 x 4

= 19600

Weighted Average: In the weighted average method, weights are assigned to the profits of each year with more weightage for the recent years. The goodwill is calculated by multiplying the weighted average profit with the number of years of purchase.

Weighted Average Profit = Sum of Weighted profits / Sum of weights

Goodwill = Weighted Average Profit x No. of years of purchase

If the profits remain constant over a period of a few years then there should be equal weightage given for all the years which is the simple average method.

If the profit is fluctuating every year then the preference shifts to the weighted average method with necessary weightage given to profits obtained from recent years.

Super Profit Method: In this method, goodwill is valued on the basis of excess profits earned by a firm in comparison to average profits earned by other firms. When a similar type of business earns a return as a certain percentage of the capital employed, it is called ‘normal return’. The excess of actual profit over the normal profit is called ‘Super Profits’.

For Ex – The other firms are earning profits within @ 15% return whereas a particular firm is earning profits @ 20%. This 5% of extra return is known as Super Profit.

Steps:

- Calculate Actual Average Profit i.e. [ Total Profit No. of Years ]

- Calculate Normal Profit i.e.

= Capital Employed × Normal Rate of Return 100

[Capital Employed = Total Assets – Outside Liabilities] - Find Out Super Profits

Super Profits = Actual Average Profit – Normal Profit

4. Calculate the Value of Goodwill

= Super profit × No. of years purchased

3. Capitalisation Methods: There are two ways of finding out the value of Goodwill through this method;

(a) By capitalizing the average profits

(b) By capitalizing the super-profits.

(a) Capitalisation of Actual Average Profit Method:

- Calculate actual average profit: [ Total Profit No. of Years ]

- Capitalize the average profit on the basis of the normal rate of return:

The capitalized value of the actual average profit

= Actual Average Profit × 100 Normal Rate of Return - Find out the actual capital employed:

Actual Capital Employed = Total Assets at their current value other than [Goodwill, Fictitious assets and non-trade investments] – Outside Liabilities. - Compute the value of Goodwill:

Goodwill = Capitalised value of actual average profit – Actual Capital Employed.

(b) Capitalisation of Super Profit Method:

1. Calculate Actual Capital Employed [same as above].

2. Calculate Super Profit [same as under Super Profit Method].

3. Multiply the Super Profit by the required rate of return multiplier:

Goodwill = Super Profit × 100 Normal Rate of Return

Treatment of Goodwill:

To compensate old partners for the loss (sacrifice) of their share in profits, the incoming partner, who acquires his share of profit from the old partners brings in some additional amount termed as a share of goodwill.

Goodwill, at the time of admission, can be treated in two ways:

- Premium Method

- Revaluation Method.

1. Premium Method:

The premium method is followed when the incoming partner pays his share of goodwill in cash. From the accounting point of view, the following are the different situations related to the treatment of goodwill:

(a) Goodwill (Premium) paid privately (directly to old partners)

[No entry is required]

(b) Goodwill (Premium) brought in cash through the firm

1. Cash A/c or Bank A/c Dr.

To Goodwill A/c

(For the amount of Goodwill brought by new partner)

2. Goodwill A/c Dr.

To Old Partner’s Capital A/c

(For the amount of Goodwill distributed among the old partners in their sacrificing ratio)

Alternatively:

1. Cash A/c or Bank A/c Dr.

To New Partner’s Capital A/c (For the amount of Goodwill brought b> a new partner)

2. New Partner’s Capital A/c Dr.

To Old Partner’s Capital A/c’s (For the amount of Goodwill distributed among the old partners in their sacrificing ratio)

3. If old partners withdrew goodwill (in full or in part) (if any)

Old Partner’s Capital A/c’s Dr.

To Cash A/c or Bank A/c

(For the amount of goodwill withdrawn by the old partners)

When goodwill already exists in books:

If the goodwill already exists in the books of firms and the incoming partner brings his share of goodwill in cash, then the goodwill appearing in the books will have to be written off.

Old Partner’s Capital A/c’s Dr.

To Goodwill A/c

(For Goodwill written-off in old ratio)

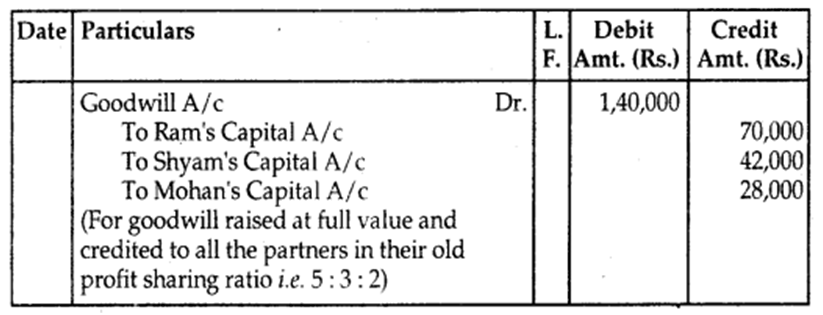

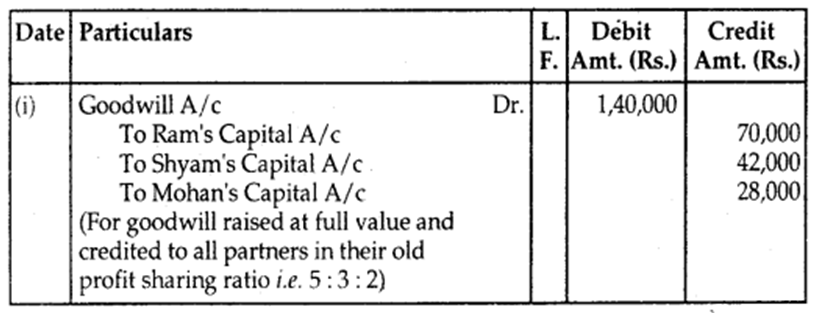

After the admission of the partner, all partners may decide to maintain the Goodwill Account in the books of accounts.

Goodwill A/c Dr.

To All Partner’s Capital A/c’s (For Goodwill raised in the new firm after admission of a new partner in new profit sharing ratio)

2. Revaluation Method:

If the incoming partner does not bring in his share of goodwill in cash, then this method is followed. In this case, the goodwill account is raised in the books of accounts. When goodwill account is to be raised in the books there are two possibilities:

(a) No goodwill appears in books at the time of admission.

(b) Goodwill already exists in books at the time of admission,

(a) No goodwill appears in the books:

Goodwill A/c Dr.

To Old Partner’s Capital A/c’s (For Goodwill raised at full value in the old ratio)

If the incoming partner brings in a part of his share of goodwill. In that case, after distributing the amount brought in for goodwill among the old partners in their sacrificing ratio, the goodwill account is raised in the books of accounts based on the portion of premium not brought by the incoming partner.

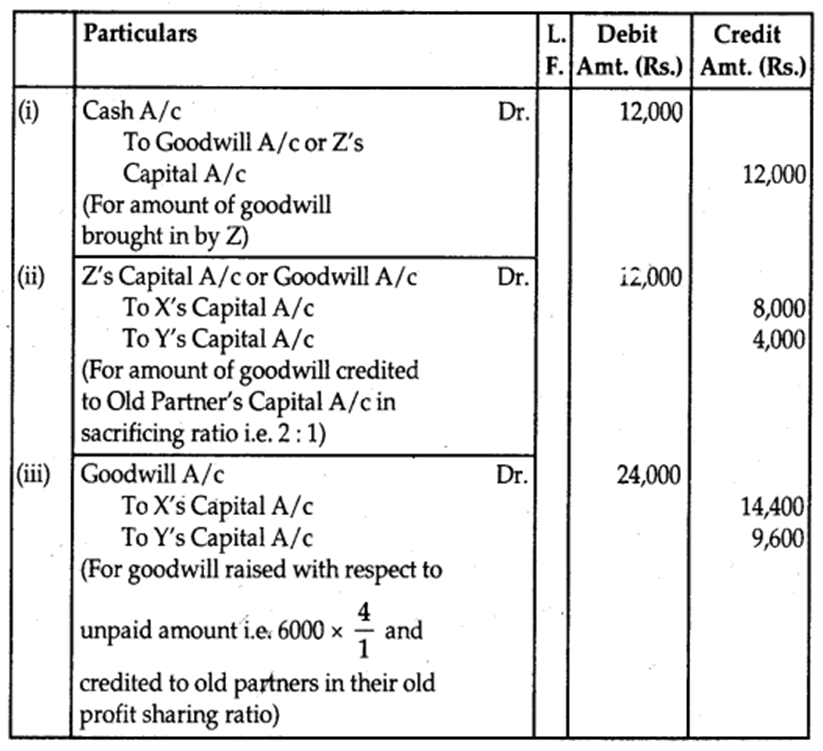

Example: X and Y are partners sharing profits in the ratio of 3: 2. They admit Z as a new partner. 14th share. The sacrificing ratio of X and Y is 2: 1. Z brings Rs. 12,000 as goodwill out of his share of Rs. 18,000. No goodwill account appears in the books of the firm.

Answer:

(b) When Goodwill already exists in the books

1. When the value of goodwill appearing in books is equal to the agreed value:

[No Entry is Required]

2. If the value of goodwill appearing in the books is less than the agreed value:

Goodwill A/c Dr.

To Old Partner’s Capital A/c’s (For Goodwill is raised to its agreed value)

3. If the value of goodwill appearing in the books is more than the agreed value:

Old Partner’s Capital A/c’s Dr.

To Goodwill A/c

(For Goodwill brought down to its agreed value)

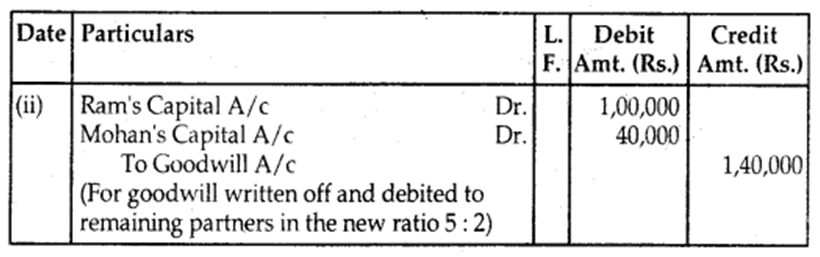

If partners, after raising Goodwill in the books and making necessary adjustments decide that the goodwill should not appear in the firm’s balance sheet, then it has to be written off.

All Partners’ Capital A/c’s Dr.

To Goodwill A/c (For Goodwill written off)

Sometimes, the partners may decide not to show goodwill accounts anywhere in books.

New Partner’s Capital A/c Dr.

To Old Partner’s Capital A/c (For adjustment for New Partner’s Share of Goodwill)

Hidden or Inferred Goodwill:

1. To find out the total capital of the firm by new partner’s capital and his share of profit.

Example: New partner’s capital for the 14th share is Rs. 80,000, the entire capital of the new firm will be

80,000 × 41 = Rs. 3,20,000

2. To ascertain the existing total capital of the firm: We will have to ascertain the existing total capital of the new firm by adding the capital (of all partners, including new partner’s capital after adjustments, if any excluding goodwill)

If assets and liabilities are given:

Capital = Assets (at revalued figures) – Liabilities (at revalued figures)

3. Goodwill= Capital from (1) – Capital from (2)

Generally, this method is used, when the incoming partner does not bring his share of goodwill in cash. Here, we find out the total goodwill of the firm. After that, we can find out the new partner’s share of goodwill and treat accordingly.

4. Adjustments of accumulated profits & losses,

Adjustment for Accumulated (Undistributed) Profits and Losses:

1. For Undistributed Profits, Reserves etc.

(For distribution of accumulated profits and reserves to old partners in old profit sharing ratio)

General Reserves A/c Dr.

Reserve fund A/c Dr.

Profit and Loss A/c Dr.

Workmen’s Compensation Fund A/c Dr.

To Old Partner’s Capital A/c’s

(For distribution of accumulated profits and reserves to old partners in old profit sharing ratio)

2. For Undistributed Losses:

Old Partner’s Capital A/c’s Dr.

To Profit and Loss A/c

(For distribution of accumulated losses to old partners in old profit sharing ratio)

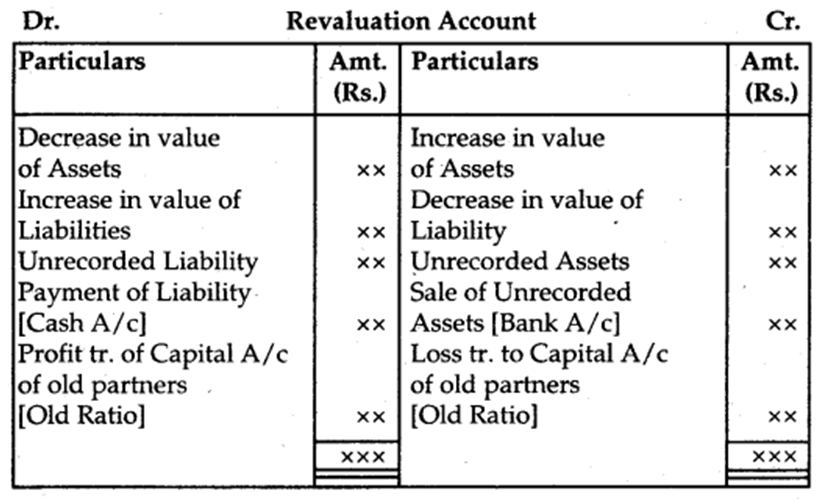

Revaluation of Assets and Reassessment of Liabilities: Revaluation of Assets and Reassessment of Liabilities is done with the help of ‘Revaluation Account’ or ‘Profit and Loss Adjustment Account’.

The journal entries recorded for revaluation of assets and reassessment of liabilities are the following:

1. For increase in the value of an Assets

Assets A/c Dr.

To Revaluation A/c (Gain)

2. For decrease in the value of an Assets

Revaluation A/c Dr.

To Assets A/c (Loss)

3. For appreciation in the amount of Liability

Revaluation A/c Dr.

To Liability A/c (Loss)

4. For reduction in the amount of a Liability

Liability A/c Dr.

To Revaluation A/c (Gain)

5. For recording an unrecorded Assets

Unrecorded Assets A/c Dr.

To Revaluation A/c (Gain)

6. For recording an unrecorded Liability

Revaluation A/c Dr.

To Unrecorded Liability A/c (Loss)

7. For the sale of unrecorded Assets

Cash A/c or Bank A/c Dr.

To Revaluation A/c (Gain)

8. For payment of unrecorded Liability

Revaluation A/c Dr.

To Cash A/c or Bank A/c (Loss)

9. For transfer of gain on Revaluation if the credit balance

Revaluation A/c Dr.

To Old Partner’s Capital A/c’s (Old Ratio)

10. For transfer of loss on Revaluation if debit balance

Old Partner’s Capital A/c’s Dr.

To Revaluation A/c (Old Ratio)

Adjustment of Capitals:

1. When the new partner brings in proportionate capital OR On the basis of the old partner’s capital.

(a) Calculate the adjusted capital of old partners (after all adjustments)

(b) Total capital of the firm

= Combined Adjusted Capital × Reciprocal proportion of the share of old partners

(c) New Partner’s Capital

= Total Capital × Proportion of share of a new partner.

2. On the basis of the new partner’s capital:

(a) Total Capital of the firm = New Partner’s Capital × Reciprocal proportion of his share.

(b) Distribute Total Capital in New Profit Sharing Ratio.

(c) Calculate adjusted capital of old partners.

(d) Calculate the difference between New Capital and Adjusted Capital.

- If the debit side of the Capital Account is bigger then it means he has excess capital

Partner’s ( capital Accounts Dr.

To Cash A /c or Bank A/c or Current A/c - If the credit side is bigger then it means that he has short capital

Cash A/c or Bank A/c or Current A/c Dr.

To Partner’s Capital A/c’s

Change in Profit Sharing Ratio among the Existing Partners:

Sometimes the existing partners of the firm may decide to change their profit-sharing ratio. In such a case, some partners will gain in future profits and some will lose. Here the gaining partners should compensate the losing partners unless otherwise agreed upon. In such a situation, first of all, the loss and gain in the value of goodwill (if any) will have to adjust.

1. Goodwill A/c Dr.

To Partner’s Capital A/c’s (For raising the amount of Goodwill in old ratio)

2. Partner’s Capital A/c’s Dr.

To Goodwill A/c

(For writing off the amount of Goodwill in New Profit sharing ratio)

Alternatively:

Gaining Partner’s Capital A/c’s Dr.

To Losing Partner’s Capital A/c’s (For adjustment due to change in profit sharing ratio)

Accounting Treatment of Goodwill

In case of change in profit sharing ratio, the gaining partner must components the sacrificing partner by paying the proportionate amount of goodwill.

Note :(i) Increase in the value of an Asset and decrease in the value of a liability result in profit.

Assets A/cDr.

To Revaluation

(ii) Decrease in the value of any asset and increase in the value of liability gives loss.

Revaluation A/cDr.

To Assets A/c

(iii) For an increase in the value of liabilities.

Revaluation A/cDr.

To Liabilities A/c

(Increase in value of Liability)

(iv) For a decrease in the value of Liabilities

Liabilities A/cDr.

To Revaluation A/c

(Decrease in the value of Liabilities)

(v) When the Revaluation account shows profit

Revaluation A/cDr.

To Partner’s Capital A/c

(Profit credited to Partner’s Capital A/c in old ratio)

(vi) In case of Revaluation Loss

Partner’s Capital A/c’sDr.

To Revaluation A/c

(Loss debited to Partner’s Capital A/cs in old ratio)

2. Dissolution of firm

DISSOLUTION OF FIRM

Dissolution of partnership firm occurs due to the following reasons;

- Compulsory dissolution

- When all the partners or all partners except one become insolvent

- When the business becomes illegal

- When all the partners except one decide to retire

- When all the partners except one die

- When the partnership agreement comes to an end as per the provisions mentioned in the agreement.

- Dissolution by Notice – In case of partnership at will, if any partner serves notice to other partners regarding his intention to dissolve the firm then it’ll amount to dissolution of partnership firm.

- Dissolution by Agreement – When all the partners mutually agree to dissolve the firm, it is considered to be dissolution of firm.

- Dissolution of the firm by Court – Under Section 44 of the Partnership Act, 1932, the court may order dissolution of the firm under following circumstances;

- A partner becomes insane

- Sheer impossibility of the business being carried on except at a loss

- Any other ground on which the court is satisfied that the business cannot be carried & it would be just & equitable that the business is wound up.

Section 39 of the Indian Partnership Act 1932 states that the dissolution of partnership firm among all the partners of the partnership firm is the Dissolution of the Partnership Firm. The dissolution of partnership firm ceases the existence of the organization.After this, the partnership firm cannot enter into any transaction with anybody. It can only sell the assets to realize the amount, pay the liabilities of the firm and discharge the claims of the partners.

However, the dissolution of a firm may be without or with the intervention of the court. It is noteworthy here that the dissolution of partnership may not necessarily result in the dissolution of the firm.But, dissolution of partnership firm always results in the dissolution of the partnership.

3. Settlement of Accounts

Settlement of Accounts

In a case where the partners do not have an agreement regarding the dissolution of the firm, the following provisions of the Indian Partnership Act 1932 will apply:

- The firm will pay the losses including the deficiency of capital firstly out of the profits, secondly out of the partner’s capital and lastly by the partners individually in their profit sharing ratio.

- The firm shall apply its assets including any contribution to make up the deficiency firstly, for paying the third party debts, secondly for paying any loan or advance by any partner and lastly for paying back their capitals. Any surplus left after all the above payments is shared by partners in profit sharing ratio.

4. Accounting Treatment

ACCOUNTING TREATMENT - JOURNAL ENTRIES

1. For transferring the assets

Transfer to the debit of realization account at their gross book values of all accounts of assets excluding cash, bank and fictitious assets.

Realization a/c Dr.

To Assets a/c(individually)

It is to be noted that debit balances such as accumulated losses and deferred expenses are not transferred to the realization account. These are transferred to the partners’ capital account in their profit sharing ratio by recording the following entry :

Partners’ capital a/c Dr.

To Fictitious assets a/c

2. For transferring the liabilities

All external liability accounts including provisions, if any, in respect of assets which have been transferred to the realization account are closed by transferring them to the credit of realization account at their book values.

External liabilities a/c(Individually) Dr.

To Realization a/c

Partners’ capital account and loan account of the partner are prepared separately and are not transferred to realization account.

3. For the sale of assets

Bank a/c(realized price) Dr.

To Realization a/c

4. For an asset taken over by a partner

Partner’s capital a/c Dr.

To Realization a/c(Agreed price)

5. For payment to creditors

Any amount paid in cash to creditors, realization account is debited and cash/bank account is credited.

Realization a/c Dr.

To Bank a/c

6. Settlement with the creditors through the transfer of asset

When a creditor accepts an asset in part payment no entry is recorded. It is because the liability due to the creditors has already been transferred to the credit of realization account and the asset is taken over by the creditor is appearing on the debit side of the realization account. Thus, the debit of the asset cancels the credit of the corresponding liability in the realization account. Sometimes, a creditor may accept part of his payment in cash and part of his payment by taking over an asset. In this case, the entry will be recorded for cash payment only.

For example, a creditor to whom Rs. 10,000 was due to accepted office equipment worth Rs. 8,000. He will be paid Rs. 2,000 in cash by recording the following entry :

Realization a/c Dr.Rs. 2,000

To Bank a/c Rs. 2,000

Whenever a creditor takes over an asset, there may be two situations :

(a) When a creditor accepts an asset whose value is more than the amount due to him, he will pay cash. It is recorded as :

Bank a/c Dr.

To Realization a/c

(b) When a creditor accepts an asset as a full and final settlement, no journal entry is recorded.

7. Expenses of realization

(a) When realization expenses are paid by the firm

Realization a/c Dr.

To Bank a/c

(b) When firm has agreed to pay partner a fixed amount towards realization expenses irrespective of the actual realization expenses

Realization a/c Dr.

To Partners’ capital a/c

(c) When the actual expenses are paid by the firm on behalf of a partner, the following entry will be recorded :

Partners’ capital a/c Dr.

To Bank a/c

(d) However, if a partner himself pays and agreed not to get them reimbursed, no journal entry is recorded.

(e) When the partner agrees to pay the expenses on behalf of the firm, the entry to be recorded :

Realization a/c Dr.

To Partners’ capital a/c

8. When liabilities are paid off

Realization a/c Dr.

To Bank a/c

9. When partner discharges a liability

The liability account is transferred from realization account to partner’s capital account by recording the following entry :

Realization a/c Dr.

Partners’ capital a/c

10. For realization of any unrecorded assets

Bank a/c Dr.

To Realization a/c

11. Unrecorded asset is taken over by a partner

Partners’ capital a/c Dr.

To Realization a/c

12. For settlement of any unrecorded liability

Realization a/c Dr.

To Bank a/c

13. Unrecorded liability is taken over by a partner

Realization a/c Dr.

To Partners’ Capital a/c

14. When the profit (loss) on realization is transferred to partners’ capital account in their respective profit sharing ratio :

(a) In case of profit on realization

Realization a/c Dr.

To Partners’ Capitals a/c(individually)

(b) In case of loss on realization

Partners’ Capitals a/c (individually) Dr.

To Realization a/c

15. For transferring accumulated profits and reserve

All accumulated profits and reserves are transferred to the partners’ capital account in their respective profit-sharing ratios:

Accumulated profit/reserves Dr.

To Partners’ capitals a/c (Individually)

16. Transfer of fictitious assets

All accumulated losses and fictitious assets are debited to the partners’ capital accounts in their profit sharing ratio :

Partners’ capitals a/c (Individually) Dr.

To Accumulated losses/Fictitious Assets a/c

17. Payment of loans

Any loans due to partners are paid off :

Partner’s loan a/c Dr.

To Bank a/c

18. Settlement of capital accounts

(a) If the partner’s capital account shows a debit balance, he is to bring in the necessary cash :

Bank a/c Dr.

To Partners’ capital a/c

(b) In the case of partners whose accounts show credit balance, the same is paid off :

Partners’ capitals a/c Dr.

To Bank a/c

It may be noted that the aggregate amount finally payable to the partners must equal to the amount available in the bank and cash accounts. Thus, all accounts of a firm are closed in case of dissolution. At times, the Balance Sheet of the firm may not be available on dissolution of partnership firm. In such a situation, first of all, all the relevant ledger balances are worked out and then the Balance Sheet of the firm on the date of its dissolution is prepared. Thereafter, the process of dissolution is undertaken in the same manner as discussed above.

What happens to goodwill on the dissolution of partnership?

We all know goodwill is an Intangible Asset. When the firm is shut down, It is common practice to sell all the assets. Thus goodwill that appeared in the Balance Sheet is transferred to the Debit side of the Realisation Account to be sold.

Journal Entry of Goodwill in Dissolution of the partnership Firm

Following are the accounting treatment with journal entries of goodwill at the time of dissolution of the partnership firm

When goodwill is transferred to Realisation Account.

Realization A/c Dr.

To Goodwill A/c

(Being goodwill transferred to realization a/c)

When goodwill is sold in cash

Bank (Cash) A/c Dr.

To Realisation A/c

(Being goodwill is sold)

When goodwill is taken over by Partner

Partner’s Capital A/c Dr

To Realisation A/c

(Being goodwill is taken over by partner)

Note:- If Nothing is mentioned about the realization amount of goodwill. It is assumed the market value of goodwill is nil and nothing is realized

(i) For Unrecorded Assets

An unrecorded asset is such an asset whose value is written off from books of accounts, but it is in usable form. It is shown as:

1. If sold in cash

Cash A/c Dr.

To Realisation A/c

(Unrecorded asset sold off for cash)

2. If taken over by any partner

Partner’s Capital A/c Dr.

To Realisation A/c

(Partner takes over unrecorded asset)

ii) For unrecorded liabilities

Liabilities that are not recorded in the books of a firm are called unrecorded liabilities. It can be shown in records as

1. When unrecorded liability is paid off

Realization A/c Dr.

To Cash A/c

(Paid in cash the price of unrecorded liability)

2. When undertaken by a partner

Realization A/c Dr.

To Partner’s Capital A/c

(Liability that is unrecorded is taken over by partner)

Difference Between Realisation and Revaluation Account

2. Treatment of Goodwill

Treatment of Goodwill:

The outgoing partner is entitled to his share of goodwill at the time of retirement/death because the goodwill has been earned by the firm with the efforts of all the existing partners. Therefore, goodwill is valued as per the agreement, at the time of retirement/death.

Due to the retirement/death of any partner, the continuing partners make again because the future profit will be shared only between the continuing partners. Therefore, the continuing partners should compensate the retiring/deceased partner for his share of goodwill in the gaining ratio.

The accounting treatment for goodwill depends upon whether the goodwill already appears in the books of the firm or not.

When Goodwill does not Appear in the Books: When Goodwill does not appear in the books of the firm, there are four following ways to compensate the retiring partner:

(a) Goodwill is raised at its full value and retained in the books:

Goodwill A/cDr.

To All Partner’s Capital A/c’s

(including retiring/deceased partner)

(For the goodwill raised at its full value and credited to capital A/c’s of a ’1 partners in their old profit sharing ratio)

The full value of goodwill will appear in the new balance sheet.

(b) Goodwill is raised at its full value and written off immediately:

If it is decided that the goodwill will not appear in the balance sheet of the reconstituted firm, then the following journal entries are required:

1. Goodwill A/c Dr.

To All Partner’s Capital A/c’s (For raising of Goodwill and credited to all partners capital A/c’s in their old profit sharing ratio)

2. Continuing Partner’s Capital A/c’s Dr.

To Goodwill A/c

(For written-off goodwill between continuing partners in their new profit sharing ratio)

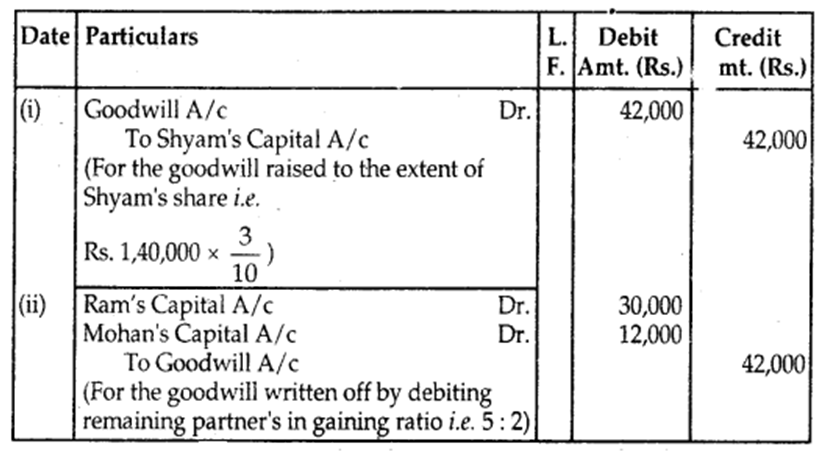

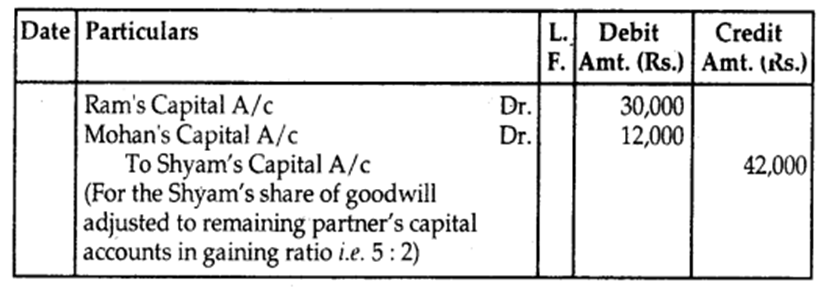

(c) Goodwill is raised to the extent of retired/deceased partner’s share and written off immediately:

1. Goodwill A/c Dr.