PathSet Publications

PathSet Publications

GOVERNMENT BUDGET

Government Budget

Definition: A government budget is an annual financial statement showing item wise estimates of expected revenue and anticipated expenditure during a fiscal year.

- Budget prepared by central government, is known as ‘Union Budget’.

- Budget is required to be approved by the parliament, before it can be implemented.

Objectives of Government Budget

- Reallocation of resources:

- Private enterprises always desire to allocate resources to those areas of production where profits are high.

- However, it is possible that such areas of production (like production of alcohol) may not promote social welfare.

- Through its budgetary policy, the government of a country directs the allocation of resources in a manner such that there is a balance between the goals of profit maximisation and social welfare.

- Production of goods which are injurious to health (like cigarettes) are discouraged through heavy taxation.

- On the other hand, production of “socially useful goods” (like khaadi) is encouraged through subsidies.

- Therefore, the government has to reallocate resources in accordance to social and economic considerations in case the free market fails to do or does so inefficiently.

2. Redistributive activities:

- Budget of a government shows its comprehensive exercise on the taxation and subsidies.

- A government uses fiscal instruments of taxation and subsidies with a view of improving the distribution of income and wealth in the economy.

- A government reduces the inequality in the distribution of income and wealth by imposing taxes on the rich and giving subsidies to the poor, or spending more on welfare of the poor.

- It reduces income of the rich and raises the living standard of the poor, thus, leads to equitable distribution of income.

- Expenditure on special anti-poverty and employment schemes will be increased to bring more people above poverty line.

- Public distribution system should be inferred so that the poor could get foodgrains and other essential items at subsidised prices.

- Therefore, equitable distribution of income and wealth is a sign of social justice, which is the principal objective of any welfare state in India.

3. Stabilising activities:

- Free play of market forces (or the forces of supply and demand) are bound to generate trade cycles, also called business cycles.

- These refer to the phases of recession, depression, recovery and boom in the economy. The government of a country is always committed to save the economy from business cycles. Budget is used as an important policy instrument to combat the situations of deflation and inflation.

- By doing it the government tries to achieve the state of economic stability.

- Economic stability leads to more investment and increases the rate of growth and development.

4. Management of Public Enterprises:

- A government undertakes commercial activities that are of natural monopolies; and which are established and managed for social welfare of the public.

- A natural monopoly is a situation where there are economies of scale over a large range of output.

- Industries, which are potentially natural monopolies, are railways etc.

5. Economic Growth

- The growth rate of a country depends on rate of saving and investment.

- For this purpose, budgetary policy aims to mobilise sufficient resources for investment in the public sector.

- Therefore, the government makes various provisions in the budget to raise overall rate of savings and investments in the economy.

6. Reducing Regional Disparities

- The government budget aims to reduce regional disparities through its taxation and expenditure policy for encouraging setting up of production units in economically backward regions.

Importance of a budget:

- Today every country aims at Economic Growth to improve the living standard of its people. There are many issues such as poverty, unemployment, inequalities in incomes, wealth etc. Government strives hard to solve these problems through budgetary measures.

- The budget shows the fiscal policy, item wise estimates of expenditure discloses how much and on what items the government is going to spend. Similarly, item wise details of government receipts indicate the sources from where the government intends to get money to finance the expenditure.

- In this way, budget is the most important instrument in hands of government. To achieve their objectives is the most important goal of the government budget.

- Note: Fiscal year is the year in which country’s budget is prepared. Its duration is from 1 April to 31 March.

Types of Budget:

- Balanced Budget

- Unbalanced Budget

Balanced Budget: If in a fiscal year, the government revenue is equal to the government expenditure, it is known as balanced budget.

Balanced Budget = Estimated Govt. Receipts = Estimated Govt. Expenditure

Unbalanced Budget: If in a fiscal year, the government expenditure is either more or less than the government receipts, the budget is known as Unbalanced budget.

It may be of two types:

- Surplus budget

- Deficit budget

Surplus Budget: If the revenue received by the general government is more in comparison to expenditure, it is known as surplus budget.

In other words, surplus budget implies a situation where government income is in excess of government expenditure.

Deficit Budget: If the expenditure made by the general government is more than the revenue received, then it is known as deficit budget.

In other words, in deficit budget, government expenditure is in excess of government income.

Components of Budget

Revenue Budget: It deals with the revenue aspect of the government budget. It explains how revenue is generated, collected ad allocated among various expenditure heads. It consists of Revenue receipts and Revenue expenditure.

Capital Budget: It deals with the capital aspect of the government budget. It consists of Capital receipts and Capital expenditure.

BUDGET RECEIPTS

BUDGET RECEIPTS

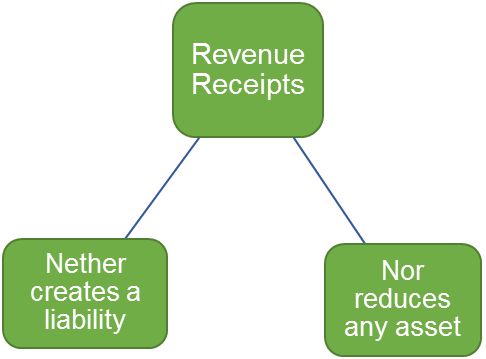

Revenue receipts

- Neither create any liabilities for the government; nor cause any reduction in assets of the government

- Revenue receipts include items, which are repetitive and regular in nature.

Revenue receipts are further classified into:

Tax Revenue:

- Tax revenue refers to receipts from all kinds of taxes such as income tax, corporate tax, excise duty etc.

- A tax is a compulsory legal payment imposed by the government on income and profit of persons and companies without reference to any benefit.

- Taxes are of two types: Direct taxes and Indirect taxes.

Direct Taxes:

- Liability to pay a tax (Impact of Tax), and (b) the burden of that tax (Incidence of tax), falls on the same person, it is termed as direct tax.

- A direct tax is paid directly by the same person on whom it has been levied. In other words, burden of a direct tax is borne by the person on whom it is imposed, which means the burden cannot be shifted to others.

- Alternatively, the person from whom the tax is collected is also the person who bears the ultimate burden of the tax. Income tax and corporate (profit) tax are most appropriate examples of direct tax.

Indirect Tax:

- Liability to pay a tax (Impact of tax) is on one person; and (b) the burden of that tax (Incidence of tax), falls on the other person, it is termed as indirect tax.

- In other words, indirect taxes are the taxes of whose burden can be shifted to others. In case of an indirect tax, person first pays the tax but he is able to transfer the burden of the tax to others.

- For instance, sales tax is an indirect tax. Government collects indirect tax from the seller of the commodity, who in turn realizes the tax amount from the buyer by including it in the price of the commodity. Other examples of indirect taxes are excise duty, custom duty, entertainment tax, service tax etc.

Non-Tax Revenue:

- Non-tax revenue refers to government revenue from all sources other than taxes.

- These are incomes, which the government gets by way of sale of goods and services rendered by different government departments.

Components of Non-Tax Revenue:

- Commercial Revenue (Profit and interest):

- It is the revenue received by the government by selling the goods and services produced by the government agencies.

- For example, profit of public sector undertakings like Railways, BHEL, and LIC etc.

- Government gives loan to State Government, union territories, private enterprises, public and earns interest receipts from these loans.

- It also includes interest and dividends on investments made by the government.

- Administrative Revenue: The revenue that arises on account of the administrative function of the government. This includes:

- Fee: Fee refers to a payment made to the government for the services that it renders to the citizens. Such services are generally in public interest and those, who receive such services, pay fees. For example, passport fees, court fees, school fees in government schools.

- License Fee: License fee is a payment to grant a permission by a government authority. For example, registration fee for an automobile.

- Fines and penalties for infringement of the law, i.e., they are imposed on lawbreakers.

- Special Assessment:

- Sometimes government undertakes developmental activities by which value of nearby property appreciates, which leads to increase in wealth. Special Assessment includes the payment made by owners of those properties whose value has appreciated. For example, if value of a property near a metro station has increased, then a part of developmental expenditure made by government is recovered from owners of such property. This is the value of special assessment.

- Forfeitures are in the form of penalties imposed by courts that a person needs to pay in the court of law for failing to comply with court orders.

- Escheat refers to the claim of the government on the property of a person who dies without having any legal heir or without leaving a will.

- External grants: Government receives financial help in the form of grants, gifts from foreign governments and international organisations (IMF, World Bank). Such grants and gifts are received during national crisis such as earthquakes, flood, war etc.

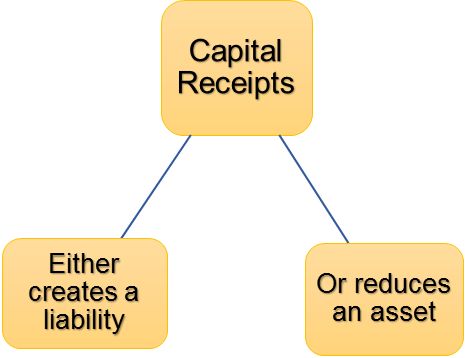

Capital Receipts:

- Government receipts that either creates liabilities (of payment of loan) or reduce assets (on disinvestment) are called capital receipts.

- Capital receipts include items, which are non-repetitive and non-routine in nature.

Components:

- Borrowing (Domestic and external): Borrowings are made to meet the financial requirement of the country. A government may borrow money:

- Domestically: General Public (By issuing government bonds in the open market).

- Externally: Rest of the world (foreign government and international institutions)

- Recovery of Loans and Advances:

- Loans offered to others are assets of the government. It includes recovery of loans granted by the central government to state and union territory governments.

- It is a capital receipt because it reduces financial assets of the government.

- For example, the government of India may give Rs.1000 crore as a loan to the state government of Delhi. Here the value of asset is Rs.1000 crore. When Delhi state government repays Rs.100 crore, the value of the assets of Government of India will reduce to Rs.900 crore. Since, recovery of loan reduces the value of assets, it is termed as a capital receipts.

- Disinvestment:

- A government raises funds from disinvestment also. Disinvestment means selling whole or a part of the shares (i.e., equity) of selected public sector enterprises held by government. As a result, government assets are reduced.

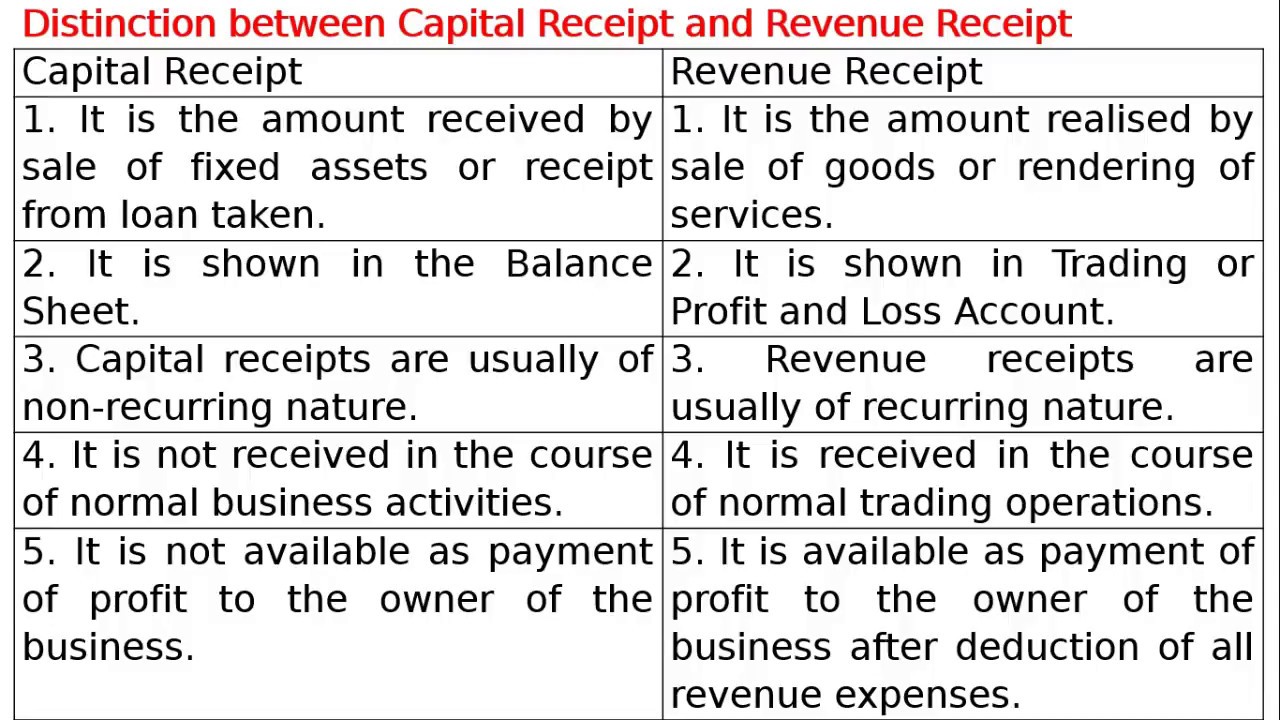

Difference between capital receipts and revenue receipts.

BUDGET EXPENDITURE

BUDGET EXPENDITURE

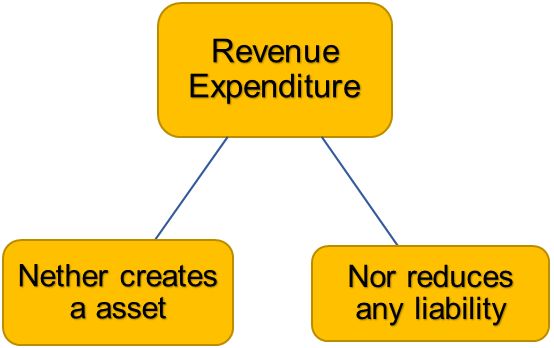

Revenue Expenditure:

- An expenditure that (a) Neither creates any assets (b) nor causes any reduction of liability.

- Examples of revenue expenditure are salaries of government employees, interest, payment on loans taken by the government, pensions etc.

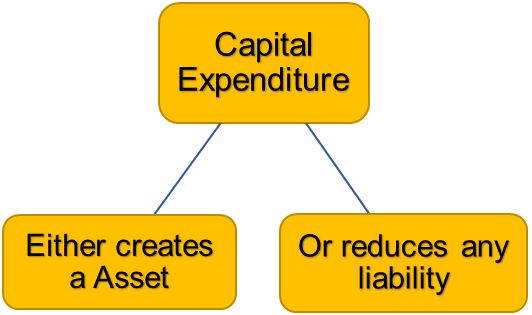

Capital Expenditure:

- An expenditure that either create assets for the government [equity or shares) of the domestic, or cause reduction in liabilities of the government.

- Examples include Loan to state and union territories, expenditure on building flyovers, road etc.

Difference between capital expenditure and revenue expenditure.

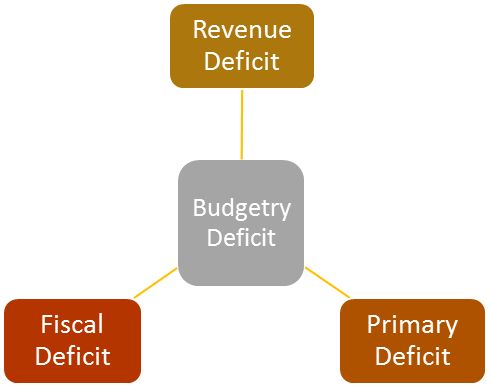

MEASUREMENT OF GOVERNMENT DEFICIT

Measures of Government Deficit.

Definition: Budgetary Deficit is defined as the excess of total estimated expenditure.

Budget deficit:

- Budgetary deficit refers to the excess of total budgetary expenditure (both revenue expenditure and capital expenditure) over total budgetary receipts (both revenue receipt and capital receipt).

- In other words, when sum of revenue receipts and capital receipts fall short of the sum of revenue expenditure and capital expenditure, budgetary deficit is said to occur.

Symbolically, Budgetary Deficit = Total Expenditure – Total Receipts

Types:

- (i) Revenue deficit

- (ii) Fiscal deficit

- (iii) Primary deficit

1. Revenue deficit:

Meaning: Revenue deficit refers to the excess of revenue expenditure of the government over its revenue receipts.

Symbolically, Revenue Deficit = Total Revenue Expenditure – Total Revenue Receipts.

Implications of revenue deficit:

- Revenue deficit indicates dis-savings on government account because the government has to make up uncovered gap.

- Revenue deficit implies that the government has to cover this uncovered gap by drawing upon capital receipts either through borrowing or through sale of its assets.

- Since government is using capital receipts to generally meet consumption expenditure of the government, it leads to an inflationary situation in the economy.

Measures to reduce revenue deficit are:

- Government should reduce its unproductive or unnecessary expenditure.

- Government should increase its receipts from various sources of tax and non-tax revenue.

2. Fiscal deficit:

Meaning: Fiscal deficit is defined as excess of total expenditure over total receipts (revenue and capital receipts) excluding borrowing.

In the form of an equation,

Fiscal Deficit = Total Expenditure – Totoal receipts excluding borrowings

- Fiscal deficit is a measure of total borrowings required by the government.

- Fiscal deficit indicates capacity of a country to borrow in relation to what it produces. In other words, it shows the extent of government dependence on borrowing to meet its budget expenditure.

- Another point to be noted here is that as the government borrowing increases, its liability in future to repay loan with interest also increases leading to a higher revenue deficit. Therefore, fiscal deficit should be as low as possible.

Implications of fiscal deficit:

- Causes Inflation: An important component of government borrowing includes borrowing from the Reserve Bank of India. This invariably implies deficit financing or meeting deficit requirements of the government by way of printing more currency. This is a dangerous practice, though very convenient for the government. It increases circulation of money and causes inflation.

- Increase in Foreign Dependence: Government also borrows from rest of the world. It increases our dependence on other countries. Foreign borrowing is often associated with economic and political interference by the lender countries. It increases our economic slavery.

- Financial Burden for Future Generation: Borrowing implies accumulation of financial burdens for the future generations. It is for future generations to repay loans as well as the mounting interest thereon.

- Deficits Multiply Borrowings: Payment of interest increases revenue expenditure of the government, causing an increase in its revenue deficit. Thus, a vicious circle is set wherein the government takes more loans to repay earlier loans, which is called Debt Trap.

Sources of Financing Fiscal Deficit

- Borrowings: From internal sources(public, commercial banks) and external sources(foreign governments, international organisations)

- Deficit Financing: Government may borrow from RBI against its securities to meet the fiscal deficit. RBI issues new currency for this purpose, this is known as deficit financing.

Comparison between Fiscal Deficit and Revenue Deficit.

3. Primary deficit:

Meaning: Primary deficit is defined as fiscal deficit minus interest payments.

Primary Deficit = Fiscal Deficit – Interest Payments

Implications of primary deficit:

- While fiscal deficit shows borrowing requirement of the government for financing the expenditure inclusive of interest payments, primary deficit reflects the borrowing requirements of the government for meeting expenditures other than interest payments on earlier loans.

Comparison between Primary Deficit and Fiscal Deficit.