Vision classes

Vision classes

1. Meaning & characteristics of NPO

NON-PROFIT ORGANISATION

MEANING & CHARACTERISTICS

Organizations are of two types: - profit-making & non-profit making. Profit-making organizations operate with the main objective of earning profit. But there are organizations whose objective is not to earn profit but to render services. These organizations are called non-profit making organizations. The services are rendered to its own members or to the society at large. The main objective of such organizations may be social, educational, religious, or charitable. The surplus arising from rendering services is not distributed among its members by way of dividends or share of profit but utilized for the furtherance of the objective of the organization—examples of non-profit making organizations are clubs, societies, schools, colleges, hospitals, charitable trusts etc.

Features of non-profit making ORGANISATIONS:

The features of non-profit making organizations are as follows:

1. Service motive – Unlike profit-making organizations, the non-profit making organization operates with the motive to serve the people of the society.

2. Separate identity – The non-profit making organizations have separate legal entities.

3. Form of organization – Such organizations function in the form of schools, colleges, hospitals, clubs, societies, charitable trusts etc.

4. Utilisation of surplus – The excess revenue earned over the cost incurred in the process of rendering services is not distributed among its members. Rather it is utilized for achieving the objective of serving society.

5. Financing – Non-profit making organizations cannot financially operate only by receiving revenue from rendering services. Therefore, it receives donations either from members or outsiders to finance the cost of rendering services.

6. Budget – Each non-profit organization prepares an annual budget. The budget gives information about the anticipated receipt and expenditure for the ensuing year.

7. Management – Such organizations are managed by elected representatives of the members.

8. Accounting – Non-profit making organizations are required to prepare their annual accounts and these accounts are submitted to the members of the government departments. The accounts are prepared on an accrual basis.

2. Accounting records

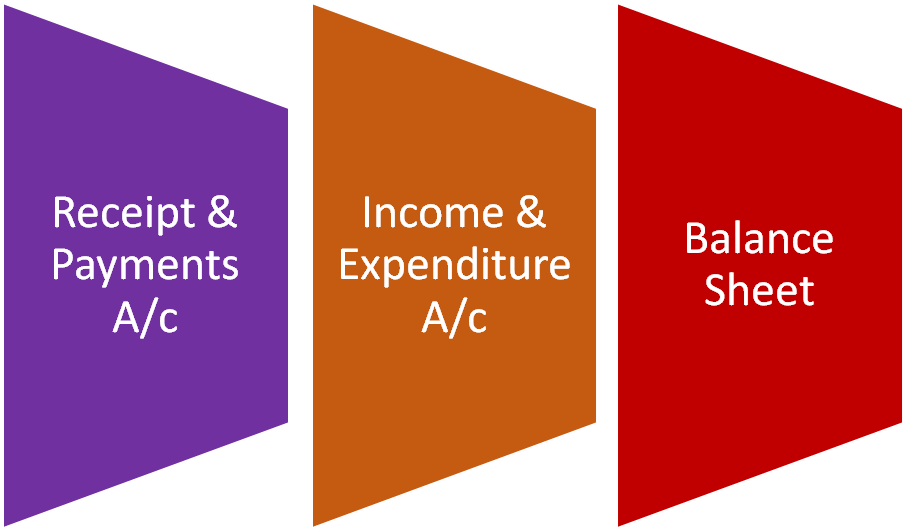

financial statements of non-profit making organizations

Like trading organizations, non-profit making organizations also prepare their financial statements at the end of each accounting period. Their financial statements comprise the following:

1. Receipts and Payments Account (Cash Book)

2. Income and Expenditure Account (Profit & Loss A/c)

3. Balance Sheet.

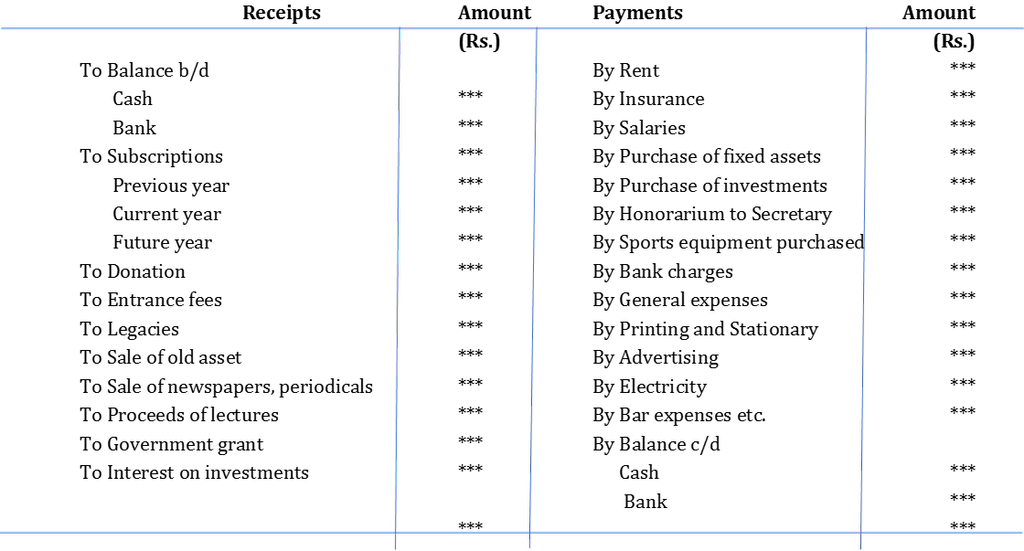

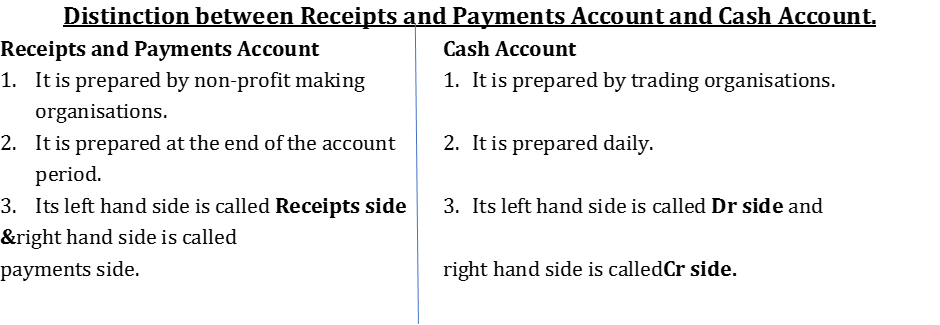

1. Receipts and Payments ACCOUNT:

The following points are noteworthy relating to Receipts and Payments A/C:

a. Receipts and Payments Account is a summary of cash transactions.

b. It shows the opening and closing balance of cash and bank, receipts and payments (both cash and cheque) and the closing cash and bank balance at the end of the accounting period.

c. The left-hand side records all receipts and the right-hand side all payments (whether revenue or capital or relating to current years past or future accounting years).

d. It shows a classified summary of cash transactions during a given period.

For example, fees may be received from the members of a club on different dates and appear on different pages of the Cash Book as it is a chronological record. But the total fees received during the accounting period is shown in the Receipts and Payments Account.

Keypoints OF RECEIPTS and Payments Account

1. It is similar to a Cash Book of a trading concern.

2. It is a real account. Receipts are recorded on the receipt side and payments are recorded on the payment side.

3. It starts with the opening cash and bank balance and closes with the closing cash and bank balance.

4. Both cash and bank transactions are merged in the same column.

5. All types of receipts are recorded on its receipts side irrespective of the nature of receipts (i.e. both capital and revenue receipts and receipts relating to past, present and future years).

6. All types of payments are recorded on the credit side irrespective of the nature of payments (i.e. both capital and revenue payments and payments relating to past, present and future years).

Format of Receipts and Payments Account:

Name of the Non-Profit Making Organisation:-

Receipts and Payments Account for the year ended **********

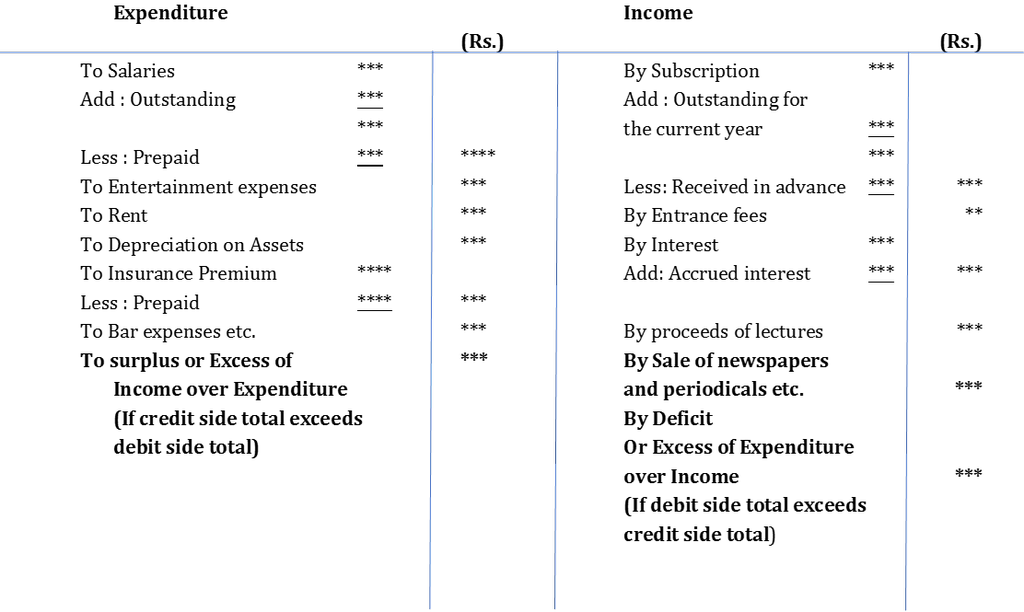

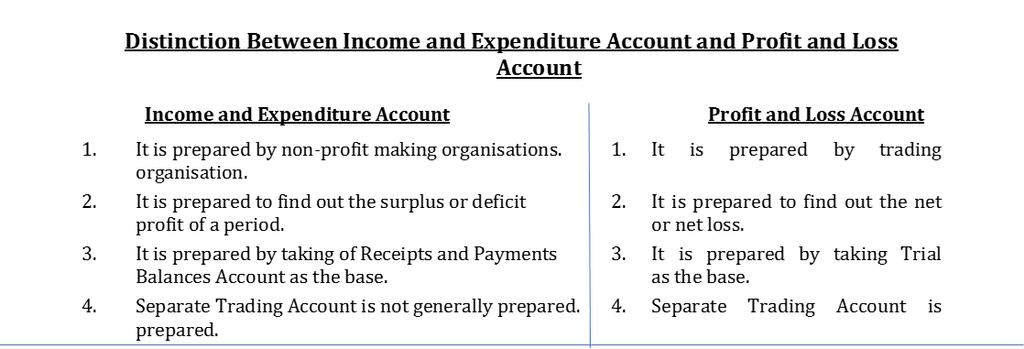

Income and Expenditure Account

Important Facts about Income & Expenditure A/C:

- Income and Expenditure Account is similar to Profit and Loss Account of a trading concern

- Since non-profit making organizations do not operate on profit objectives, income and Expenditure Account is prepared instead of preparing Profit and Loss Account.

- On the debit side, it shows all revenue expenses relating to the current year whether paid or not.

- On the credit side, it shows all revenue incomes and gains relating to the current year whether received or not.

- It is a nominal account and its preparation procedure is the same as that of a Profit and Loss Account of a trading concern.

- The balancing figure of this account is called surplus/excess of income over expenditure or deficit/excess of expenditure over income.

Key points of Income and Expenditure Account

1. It is similar to the Profit and Loss Account of a trading concern.

2. It is a nominal account. Expenses and losses are recorded on the debit side and incomes and gains are recorded on the credit side. The expenses are matched with revenues of the concerned period.

3. All revenue incomes relating to the current year whether received or due are recorded on the credit side.

4. All revenue expenses relating to the current year whether paid or outstanding are recorded on the debit side.

5. Capital expenditures and capital receipts are not recorded in this account.

6. It records both cash and non-cash items such as depreciation.

Format of Income and Expenditure Account

(Name of the Non-Profit Making Organisation)

Income and Expenditure Account

For the year ended on *********

3. Balance Sheet

The balance sheet of a non-profit making organization is prepared on the same line as that of a trading concern. Assets including accrued income and prepaid expenses are shown on the assets side and the liabilities side shows all liabilities including outstanding expenses. Capital Fund (same as Capital Account in case of trading concerns) appears on the liabilities side. The surplus during the period is added to the Capital Fund and the deficit is subtracted.

Note: When no information regarding Capital Fund is available, it can be ascertained by preparing the Balance Sheet at the beginning of the year i.e. Opening Balance Sheet.

3. Preparation of opening & closing Balance Sheet, Some peculiar items, Incidental Trading Activity

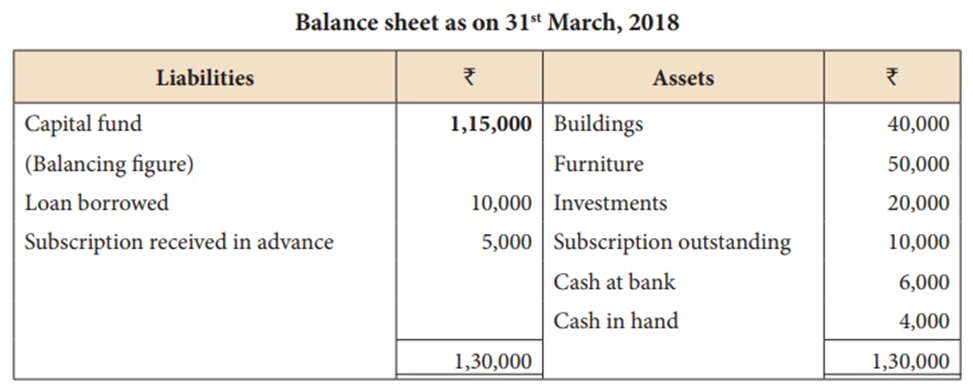

How to Prepare Opening & Closing Balance Sheet?

Step 1 – Take into account the closing balances of assets & liabilities of the previous year & the opening balances of the Receipts & Payments A/c will be the cash in hand & cash at the bank as of that date. The Balancing Figure will be Capital Fund

Step 2 – After the preparation of the opening Balance Sheet, we shall proceed towards the preparation of the Closing Balance Sheet& for this purpose, the assets will be then adjusted for any sale or purchase during the year. Any gain or loss on the sale of assets will be taken to Income & Expenditure A/c. Any depreciation will also be taken to Income & Expenditure A/c. Only the net assets will appear on the Balance Sheet& the payments made for the purchase of new assets in the Receipts & Payments A/c shall appear as the new asset or added to the old assets.

Step 3 – From the Receipts side, any capital receipts like contributions to Building Fund & specific funds like specific donations will be recorded on the liabilities side.

Step 4 – Adjustments for prepaid & outstanding expenses will be made to the relevant expenses. Outstanding expenses & advance subscriptions will appear on the liabilities side whereas prepaid expenses & outstanding subscriptions will appear on the asset side.

Step 5 – The liabilities appearing in the previous year’s Balance Sheet should be checked with the payments made during the year. If some liabilities have been paid, then these liabilities will not appear in the new Balance Sheet to the extent they are paid. Only the net unpaid amount if any will appear on the Balance Sheet.

Step 6 – Finally, the Capital Fund balance from Opening Balance Sheet shall be adjusted with surplus or deficit from the Income & Expenditure A/c & also any specific fund which is not required anymore will be added to the Capital fund.

AN EXAMPLE OF CLOSING A BALANCE SHEET

Meaning and Treatment of Special Items

The meaning and treatment of the special items in the financial statements of non-profit making organizations are as follows:

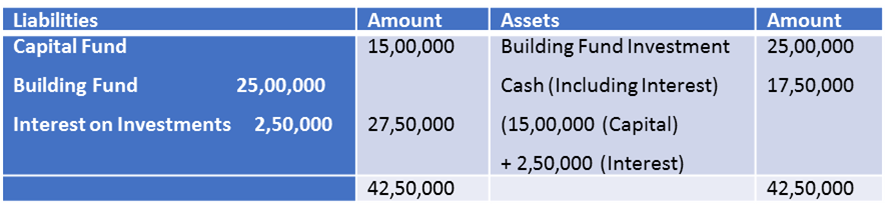

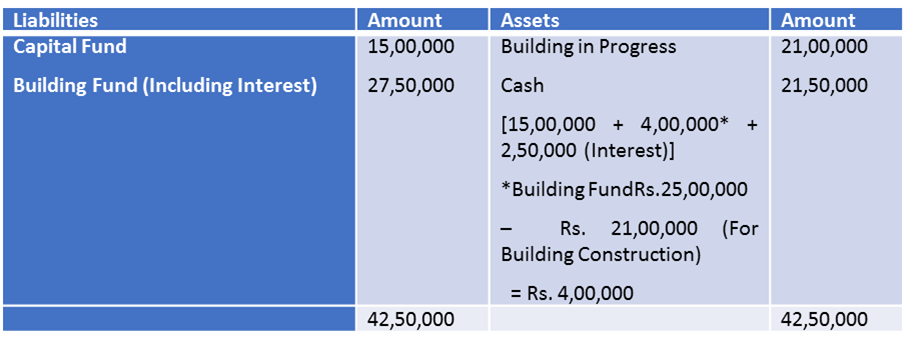

1. Capital Fund

Non-profit organizations follow FUND BASED ACCOUNTING method. In this method, the fund is of two types i.e. General Fund or Capital Fund & Specific Fund. The capital introduced is known as the General Fund or Capital Fund. It is an unrestricted fund that can be used to achieve the objectives of society. All the recurring expenses like salary and rent are charged to General Fund through Income & Expenditure A/c similarly all the revenues are added to the General Fund through Income & Expenditure A/c. If the fund money is invested somewhere then the interest earned will be directly added to the General Fund/Capital Fund.

On the other hand, Specific Fund is a restricted fund set up for a specific purpose. The money can be used only for the achievement & realization of that particular purpose. The restriction on the use of this fund is either put by the donor or by the management. If the fund money is invested somewhere then the interest earned will be directly added to the specific Fund. It is again classified into two types;

- Specific Asset Building – Funds used for building some fixed assets like Building or Pavilion.

![]()

![]()

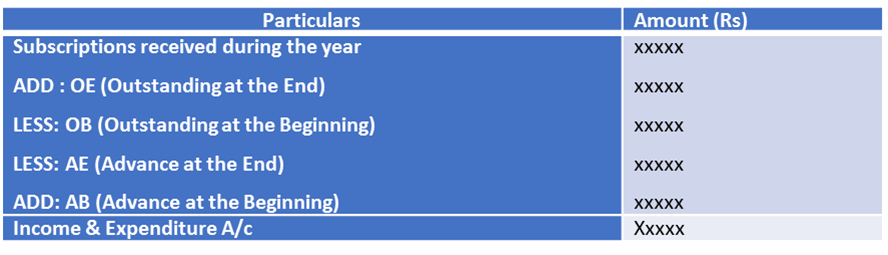

2. Subscriptions

Subscriptions are collected by non-profit making organizations from their members regularly. It is revenue in nature. It is the main source of income for any non-profit making organization. Subscriptions related to the current year shall be recorded in Income & Expenditure A/c whether received or not. Subscriptions due for the current year shall also be shown in the asset side of the Balance Sheet. Subscriptions received in advance for next year shall not appear in the Income & Expenditure A/c as it is not a current year item but the amount received in advance shall be recorded as a liability in the Balance sheet as it is a prepaid income.

Explanation:-

Income& Expenditure A/c is nothing but P/L A/c with a different name. Since the purpose of preparing P/L A/c is to find out the current year's profit or loss, therefore, only current items of revenue nature is recorded in P/L A/c. In the same way, Income & Expenditure A/c also records only the current year items & items of the previous year & next year are excluded.

- Outstanding at the end shall be added as it is a current year item.

- Outstanding at the beginning shall be deducted as it is a previous year's item (last year’s closing outstanding is this year’s opening outstanding)

- Advance at the End is not a current year item. It is the membership fees received for next year in advance so it’ll be deducted from the total subscriptions received.

- Advance at the beginning is this year’s income because it represents last year’s closing advance i.e. membership fees for the current year received in advance during the previous year.

3. Donations

A non-profit making organization may receive donations from time to time. Donations received for a particular purpose like the development of a pavilion, construction of a building, awarding prizes etc. are called specific donations. A donation received not for a specific purpose is called a general donation.

Accounting Treatment: All specific donations are to be capitalized i.e. put in the liabilities side of the Balance Sheet.

If the general donation is a big amount it is to be capitalized i.e. added to the Capital Fund in the liabilities side of the Balance sheet.

In case the general donation is a small amount it is treated as income and put in the credit side of the Income and Expenditure Account.

Note: Whether the amount of general donation is big or small, it is judged by considering the nature of the activities of the non-profit making organizations.

4. Entrance Fees

This is the fee collected from the new entrants on admission to the clubs or societies etc. It is also known as admission fees.

Accounting Treatment: The entrance fees may be treated as revenue or capital depending upon the rule and by-laws of the organizations.

5. Legacies

It is a kind of gift received by a non-profit making organisation as per the will of a deceased person.

Accounting Treatment: If legacy is a small amount, it is treated as an income and is to be taken in the credit side of Income and Expenditure Account.

In case of a big amount, it should be capitalised i.e. added to Capital Fund in the liabilities side of Balance Sheet.

Note:Whether the amount of legacy is big or small, it is judged by considering the nature of activities of non-profit making organisation.

6. Life Membership Fees

Membership fees for the whole life collected from members is known as life membership fees. In this case the member is to pay a lump-sum amount instead of periodic payments and enjoys the benefits of the organisation till the end of his life.

Accounting Treatment: Life membership fees is treated as capital item and hence added to the Capital fund.

Note: However, there is another way of treatment.

It is credited to a separate fund (Life Membership Fees Account) and an amount equal to the annual membership fee (subscription) is transferred to the Income and Expenditure Account. The balance in the separate fund is shown in the liabilities side of the Balance Sheet. If a life member dies, then the balance lying in the special fund is transferred to the Capital Fund of the organization.

7. Special Fund

Sometimes a non-profit making organisation may create funds for some special purposes. For example, a sports club may create Tournament Fund for meeting tournaments expenses or a building fund for the construction of building etc.

Accounting Treatment: The fund may be invested in banks or in Govt. securities.

- Any income relating to such special fund is added to this fund.

- Any expenditure on account of this fund is subtracted from such fund.

- Such special fund appears in the liabilities side of Balance Sheet.

- If there is deficit (the expenditure on account of fund is more than the amount of fund) it is recorded in the expenditure side of Income and Expenditure Account.

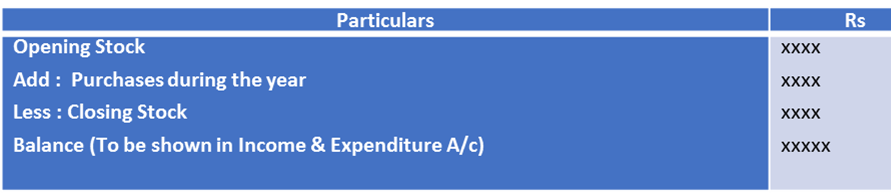

8. Calculation of Cost of Consumable Goods – Consumable goods are the items that are used or consumed during the year such as sports material, stationery, books, medicines, and food items. In the Income & Expenditure A/c, only the amount of such items consumed will during the year be shown. Therefore, it is necessary to find out the cost of consumption of such goods.

STEPS TO PREPARE INCOME & EXPENDITURE A/C FROM RECEIPTS & PAYMENTS A/C

- Prepare the Opening Balance Sheet to find out the opening balance of Capital Fund (if it is not given).

- Identify the revenue receipts from the receipts side of Receipts & Payment A/c & show them in the Income side of the Income & Expenditure A/c. Capital receipts will be shown in the Balance sheet.

- Identify the Capital expenditure from the payment side of Receipts & Payment A/c & show it in the Balance sheet. Capital items won’t appear in Income & Expenditure A/c.

- Certain items do not appear in Receipts & Payment A/c but shall be recorded in Income & Expenditure A/c such as depreciation of fixed assets, loss on sale of fixed assets, and profit on the sale of fixed assets. Depreciation & loss shall be shown in the Expenditure side whereas profit on the sale of fixed assets shall be shown in the Income side.

- Finally, find out the surplus or deficit i.e. if the income side is higher it is surplus & if the expenditure side is higher then it is a deficit.

- Prepare Closing Balance Sheet by taking into consideration the opening balance of assets & liabilities, surplus/deficit, purchase & sale of assets during the year & depreciation on fixed assets. The surplus shall be added to the Capital whereas the Deficit shall be deducted from the Capital.

INCIDENTAL TRADING ACTIVITY

This Incidental Trading activity is also known as incidentals, these are the gratuities and the fees or costs which are incurred in addition to the main item, service or event paid for during the trading pursuits.

Trading pursuits like a hospital or a chemist shop or even a beauty parlor or canteen, all these places can also in use to furnish certain provisions to the members or public. In this scenario, the trading A/c has to be drawn to determine the outcome of this incidental pursuit. The profit from these trading pursuits is solicited to accomplish the primary objectives which satisfy the cause for which the establishment was set up, then it is transferred to the Income and Expenditure A/c.

In Relation to the Above, the following are the Details:

- The trading A/c has to be outlined to ascertain either profit or loss due to incidental commercial pursuit. All these costs and revenues in a straight way and principally are associated with such pursuits, are documented in the trading A/c. After this, the Balance of the trading A/c is being transferred to the Income and Expenditure A/c

- Income and Expenditure A/c documents, also the trading profit (or loss), and all other incomes and expenses are not documented in the Trading A/c. Surfeit or deficit is disclosed by the Income and Expenditure A/c as is being transferred to the capital or general fund.