SUDIP CHAKRABORTY

SUDIP CHAKRABORTY

1. Modes of reconstitution of a partnership firm, Admission of a new partner

(MODES OF RECONSTITUTION)

A partnership firm may go for reconstitution for various reasons such as;

- Change in the profit-sharing ratio among the Existing Partners.

- Admission of a Partner.

- The Retirement of an Existing Partner.

- Death or Insolvency of a Partner.

ADMISSION OF A PARTNER

- Admission of a partner is one of the modes of reconstitution of partnership firm because when a new partner is admitted, the existing agreement among the partners comes to an end & a new agreement comes into existence which results in change in profit sharing ratio, goodwill valuation & reassessment of assets & liabilities.

- The capital contribution of the new partner, his liabilities, and share of profits is decided upon.

- As per Section 31 of the Indian Partnership Act, the new partner shall not be admitted to the firm without the consent of all existing partners.

- After admission, the new partner gets the following two rights :

- Right to share future profits of the firm

- Right to share in the assets of the firm

- He/she also becomes liable for any liability of the business incurred after admission & any loss incurred by the firm

- The new/incoming partner receives share in future profits that is equal to the sacrifice of profit by an existing partner/partners of the firm & the same new partner has to compensate the partner/partners who are sacrificing their share in profits in his/her favor.

- Such amount paid by the incoming partner is known as Goodwill or Premium for Goodwill.

- Besides Goodwill/Premium for Goodwill, the new partner also contributes in Capital to get the rights in the assets of the firm.

Effects of Admission of Partner

- Old partnership agreement comes to an end & a new agreement is formed.

- New or incoming partner becomes entitled to the future share of profits & losses of the firm.

- New or incoming partner contributes an agreed amount of capital in the firm.

- New or incoming partner gets a right to the assets of the firm.

- Adjustments are made regarding the accumulated profits & losses

- Assets are revalued & liabilities are reassessed & the net change is adjusted in existing or old partner’s capital accounts in their old profit sharing ratio.

- Goodwill of the firm is valued in order to pay the sacrificing partner for their sacrificed share by the gaining partners through their capital accounts.

What are the adjustments required on the admission of a partner?

- Determining new profit sharing ratio

- Valuation of adjustment of goodwill

- Adjustment of profit/loss arising from revaluation of assets & reassessment of liabilities.

- Adjustments of accumulated profits, reserves & losses.

- Adjustment of capital (if agreed)

1. Modes of reconstitution of a partnership firm, Admission of a new partner

- Books Name

- Vision classes Accountancy Book

- Publication

- Vision classes

- Course

- CBSE Class 12

- Subject

- Accountancy

CHAPTER -3

Reconstitution of a Partnership Firm – Admission of a Partner

Partnership is an agreement between two or more persons (called partners) for sharing the profits of a business carried on by all or any of them acting for all. Any change in the existing agreement amounts to reconstitution of the partnership firm. This results in an end of the existing agreement and a new agreement comes into being with a changed relationship among the members of the partnership firm and/or their composition. However, the firm continues. The partners often resort to reconstitution of the firm in various ways such as admission of a new partner, change in profit sharing ratio, retirement of a partner, death or insolvence of a partner. In this chapter we shall have a brief idea about all these and in detail about the accounting implications of admission of a new partner or an on change in the profit sharing ratio.

Modes of Reconstitution of a Partnership Firm

Reconstitution of a partnership firm usually takes place in any of the following ways:

Admission of a new partner: A new partner may be admitted when the firm needs additional capital or managerial help. According to the provisions of Partnership Act 1932 unless it is otherwise provided in the partnership deed a new partner can be admitted only when the existing partners unanimously agree for it. For example, Hari and Haqque are partners sharing profits in the ratio of 3:2. On April 1, 2017 they admitted John as a new partner with 1/6 share in profits of the firm. With this change now there are three partners of the firm and it stands reconstituted.

Change in the profit sharing ratio among the existing partners: Sometimes the partners of a firm may decide to change their existing profit sharing ratio. This may happen an account of a change in the existing partners’ role in the firm. For example, Ram, Mohan and Sohan are partners in a firm sharing profits in the ratio of 3:2:1. With effect from April 1,2017 they decided to share profits equally as Sohan brings in additional capital. This results in a change in the existing agreement leading to reconstitution of the firm.

Retirement of an existing partner: It means withdrawal by a partner from the business of the firm which may be due to his bad health, old age or change in business interests. In fact a partner can retire any time if the partnership is at will. For example, Roy, Ravi and Rao are partners in the firm sharing profits in the ratio of 2:2:1. On account of illness, Ravi retired from the firm on March 31, 2017. This results in reconstitution of the firm now having only two partners.

Death of a partner: Partnership may also stand reconstituted on death of a partner, if the remaining partners decide to continue the business of the firm as usual. For example, X,Y and Z are partners in a firm sharing profits in the ratio 3:2:1. X died on March 31, 2017. Y and Z decide to carry on the business sharing future profits equally. The continuity of business by Y and Z sharing future profits equally leads to reconstitution of the firm.

Admission of a New Partner

When firm requires additional capital or managerial help or both for the expansion of its business a new partner may be admitted to supplement its existing resources. According to the Partnership Act 1932, a new partner can be admitted into the firm only with the consent of all the existing partners unless otherwise agreed upon. With the admission of a new partner, the partnership firm is reconstituted and a new agreement is entered into to carry on the business of the firm.

A newly admitted partner acquires two main rights in the firm–

1. Right to share the assets of the partnership firm; and

2. Right to share the profits of the partnership firm.

For the right to acquire share in the assets and profits of the partnership firm, the partner brings an agreed amount of capital either in cash or in kind. Moreover, in the case of an established firm which may be earning more profits than the normal rate of return on its capital the new partner is required to contribute some additional amount known as premium or goodwill. This is done primarily to compensate the sacrificing partners for loss of their share in super profits of the firm.

Following are the other important points which require attention at the time of admission of a new partner:

1. New profit sharing ratio;

2. Sacrificing ratio;

3. Valuation and adjustment of goodwill;

4. Revaluation of assets and Reassessment of liabilities;

5. Distribution of accumulated profits (reserves); and

6. Adjustment of partners’ capitals.

2. New profit sharing ratio, Sacrificing Ratio

Determination of New Profit Sharing Ratio

The new or incoming partner is entitled to the share of future profits & losses of the firm. Therefore, there will be a change in the existing profit sharing ratio of the old partners since the new partner will acquire his/her share from the existing share of old partners. The new or incoming partners may acquire the share from the old partner in the following ways;

- In their old profit-sharing ratio

- In a particular ratio or surrendered ratio

- In a particular fraction from some of the partners

Let us discuss in detail;

- When a new partner acquires his share from old or existing partners in their old profit sharing ratio;

In this situation, the share of the new partner is given & it is assumed that the new partner has acquired his share from old partners in their old profit sharing ratio. Old partners continue to share the balance profits & losses in their old profit-sharing ratio. Unless otherwise agreed, the profit-sharing ratio of the existing partners remains unchanged & the new profit sharing ratio is determined by deducting new or incoming partner’s share from 1 & then dividing the balance in old profit sharing ratio of the old partners.

- When share of the New partner is given & new ratio of Old Partners is also given;

In this case, the new partner’s share is deducted from 1 & the balance is divided among old partners in their new ratio. Hence, there is a new profit-sharing ratio for all the partners.

- When New or Incoming Partner acquires his share from old or existing partners in a particular ratio;

In such a case, the new or incoming partner acquires a part of share of profits from one partner & a part of share of profits from another partner. The existing partner’s share will change to the extent of share sacrificed on admission of new partner.

- When new or incoming partner acquires his shares by surrender of particular fraction of their shares by the old or existing partners;

In such a case, the shares surrendered by the old partners in favor of the new partners are added & it becomes the share of the new partner. The shares surrendered by the old partners is deducted from their respective share to determine old partner’s share in the reconstituted firm.

The Concept of Sacrificing Ratio

Sacrificing ratio can be explained as the ratio in which existing or old partners sacrifice their share of profits in favor of the new or incoming partner. It can also be defined as the ratio in which the new partner is given a share by the existing partners. This share can be given by all the partners equally or by some of the partners in agreed share. Sacrificing ratio determines the compensation that new partner should pay to the old partners for the share of profits sacrificed by them. The following can be the situations under which sacrificing ratio is determined;

- When the share of new or incoming partner is given without giving the details of the sacrifice made by the old or existing partners

In this situation, there is no change in the profit sharing ratio of old partners because it is assumed that the partners make sacrifices in their old profit sharing ratio & for that reason sacrificing ratio is always in the old profit sharing ratio.

- When the old ratio of old or existing partners & new ratio of all the partners are given

In this case, the sacrificing ratio is the difference between the old ratio & the new ratio.

- When new or incoming partner acquires the share by surrendering a particular fraction of shares by old partners

In such a case, the shares surrendered by the old partner in favor of the new partner are added & it becomes the share of the incoming or new partner. The shares so surrendered by the old partner is deducted from his old share to find out his share in the reconstituted firm.

2. New profit sharing ratio, Sacrificing Ratio

- Books Name

- Vision classes Accountancy Book

- Publication

- Vision classes

- Course

- CBSE Class 12

- Subject

- Accountancy

New Profit Sharing Ratio

When new partner is admitted he acquires his share in profits from the old partners. In other words, on the admission of a new partner, the old partners sacrifice a share of their profit in favour of the new partner. But, what will be the share of new partner and how he will acquire it from the existing partners is decided mutually among the old partners and the new partner. However, if nothing is specified as to how the new partner acquires his share from the old partners; it may be assumed that he gets it from them in their profit sharing ratio. In any case, on admission of a new partner, the profit sharing ratio among the old partners will change keeping in view their respective contribution to the profit sharing ratio of the incoming partner. Hence, there is a need to ascertain the new profit sharing ratio among all the partners. This depends upon how does the new partner acquires his share from the old partners for which there are many possibilities. Let us understand it with the help of the following Revisions.

Revision 1

Solution

Vishal’s new share = 2/5 × 4/5 = 8/25

New profit sharing ratio of Anil, Vishal and Sumit will be 12:8:5.

Note: It has been assumed that the new partner acquired his share from old partners in old ratio

Revision 2

Solution

Dinesh’s share = 1/5 or 2/10

Akshay’s share = 3/5 – 1/10 = 5/10

Bharti’s share = 2/5 – 1/10 = 3/10

New profit sharing ratio between Akshay, Bharati and Dinesh will be 5:3:2.

Revision 3

Anshu and Nitu are partners sharing profits in the ratio of 3:2. They admitted Jyoti as a new partner for 3/10 share which she acquired 2/10 from Anshu and 1/10 from Nitu. Calculate the new profit sharing ratio of Anshu, Nitu and Jyoti.

Solution

Jyoti’s share = 3/10

Anshu’s new share = 3/5 – 2/10 = 4/10

Nitu’s new share = old share – share surrendered

= 2/5 – 1/ 10 = 3/10

The new profit sharing ratio between Anshu, Nitu and Jyoti will be 4 : 3 : 3

Revision 4

Ram and Shyam are partners in a firm sharing profits in the ratio of 3:2. They admit Ghanshyam as a new partner. Ram sacrificed 1/4 of his share and Shyam 1/3 of his share in favour of Ghanshyam. Calculate new profit sharing ratio of Ram, Shyam and Ghanshyam.

Solution

Ram’s old share = 3/5

Share sacrificed by Ram = ¼ of 3/5 = 3/20

Ram’s new share = 3/5 – 3/20 = 9/20

Shyam’s old share = 2/5

Share sacrificed by shyam = 1/3 of 2/5 = 2/15

Shyam’s new share = 2/5 – 2/15 = 4/15

Ghanshyam’s new share = Ram’s sacrifice + Shyam’s Sacrifice

= 3/20 + 2/15 = 17/60

New profit sharing ratio among Ram, Shyam and Ghanshyam will be 27:16:17

Revision 5

Solution

Pal’s share = 1/4

Das’s new share = old share – share surrendered = 4/5 – ¼ = 11/20

Sinha’s new share = 1/5

The new profit sharing ratio among Das, Sinha and Pal will be 11:4:5.

Sacrificing Ratio

The ratio in which the old partners agree to sacrifice their share of profit in favour of the incoming partner is called sacrificing ratio. The sacrifice by a partner is equal to : Old Share of Profit – New Share of Profit

As stated earlier, the new partner is required to compensate the old partner’s for their loss of share in the super profits of the firm for which he brings in an additional amount as premium for goodwill. This amount is shared by the existing partners in the ratio in which they forgo their shares in favour of the new partner which is called sacrificing ratio.

The ratio is normally clearly given as agreed among the partners which could be the old ratio, equal sacrifice, or a specified ratio. The difficulty arises where the ratio in which the new partner acquires his share from the old partners is not specified. Instead, the new profit sharing ratio is given. In such a situation, the sacrificing ratio is to be worked out by deducting each partner’s new share from his old share. Look at the Revisions 6 to 8 and see how sacrificing ratio is calculated in such a situation.

Revision 6

Rohit and Mohit are partners in a firm sharing profits in the ratio of 5:3. They admit Bijoy as a new partner for 1/7 share in the profit. The new profit sharing ratio will be 4:2:1. Calculate the sacrificing ratio of Rohit and Mohit.

Solution

Rohit’s old share = 5/8

Rohit’s new share = 4/7

Rohit’s sacrifice = 5/8 – 4/7 = 3/56

Mohit’s old share = 3/8

Mohit’s new share = 2/7

Mohit’s sacrifice = 3/8 – 2/7 = 5/56

Sacrificing ratio among Rohit and Mohit will be 3:5.

Revision 7

Amar and Bahadur are partners in a firm sharing profits in the ratio of 3:2. They admitted Mary as a new partner for 1/4 share. The new profit sharing ratio between Amar and Bahadur will be 2:1. Calculate their sacrificing ratio.

Solution

Mary’s share = 1/4

Remaining share = 1 – ¼ = 3/4

Therefore,

Amar’s new share = 2/3 of ¾ = 6/12 or 2/4

Bahadur’s new share = 1/3 of ¾ = 3/12 or 1/4

New profit sharing ratio of Amar, Bahadur and Mary will be 2:1:1.

Amar’s sacrifice = 3/5 – 2/4 = 2/20

Bahadur’s sacrifice = 2/5 – ¼ = 3/20

Sacrificing ratio among Amar and Bahadur will be 2:3.

Ramesh and Suresh are partners in a firm sharing profits in the ratio of 4:3. They admitted Mohan as a new partner. The profit sharing ratio of Ramesh, Suresh and Mohan will be 2:3:1. Calculate the gain or sacrifice of old partner.

Solution

Ramesh’s old share = 4/7

Ramesh’s new share = 2/6

Ramesh’s sacrifice = 4/7 – 2/6 = 10/42

Suresh’s new share = 3/6

Suresh’s old share = 3/7

Suresh’s gain = 3/6 – 3/7 = 3/42

Mohan’s share = 1/6 0r 7/ 42

Ramesh’s sacrifice = Suresh’s gain+Mohan’s gain

= 3/42 + 7/42 = 10/ 42

In this case, the whole sacrifice is by Ramesh alone.

3. Goodwill - Meaning, Nature & Valuation

Goodwill:

Goodwill is the value of the reputation of a firm. In other words, a well-established business develops the advantage of a good name, reputation and wide business connections. This helps the business to earn more profits as compared to newly set-up businesses. This advantage in monetary terms is called ‘Goodwill’ & it arises only if a firm is able to earn higher profits than normal.

“Goodwill may be said to be that element arising from the reputation, connections or other advantages possessed by a business which enable it to earn greater profits than the return normally to be expected on the capital represented by the net tangible assets employed in the business.” – Spicer and Pegler

Characteristics of Goodwill:

- Goodwill is an intangible asset

- It is a valuable asset. It helps in earning higher profits than normal.

- It is very difficult to place an exact value on goodwill. It is fluctuating from time to time due to changing circumstances of the business.

- Goodwill is an attractive force that brings in customers.

- Goodwill comes into existence due to various factors.

Factors Affecting the Value of Goodwill

1. Nature of business: Company produces high value-added products or has stable demand in the market. Such a company will have more goodwill and is able to earn more profits.

2. Location: If a business is located in a favorable place, it will attract more customers and therefore will have more goodwill.

3. Efficient Management: Efficient Management brings high productivity and costs efficiency to the business which enables it to earn higher profits and thus more goodwill.

4. Market Situation: A firm under monopoly or limited competition enjoys high profits which leads to a higher value of goodwill.

5. Special Advantages: A firm enjoys a higher value of goodwill if it has special advantages like import licenses, low rate and assured supply of power, long-term contracts for sale and for purchase, patents, trademarks etc.

6. Quality of Products: If the quality of products of the firm is good and regular, then it has more goodwill.

Valuation of Goodwill: Why is it needed?

- At the time of sale of a business;

- Change in the profit-sharing ratio amongst the existing partners;

- Admission of a new partner.

- Retirement of a partner;

- Death of a partner;

- Dissolution of a firm;

- The amalgamation of the partnership firm

Methods of Valuation of Goodwill: There are various methods for the valuation of goodwill in the partnership business. The value of goodwill may differ in different methods. Goodwill is an intangible asset, so it is very difficult to calculate its exact value. As per the money measurement concept of Accounting, anything that cannot be measured in terms of money should not be recorded in books of accounts. Therefore, it is important to convert Goodwill into monetary terms to record it in the books of accounts. The methods followed for valuing goodwill are:

- Average Profit Method

- Super Profit Method

- Capitalisation Method.

1. Average Profit Method: In this method, Goodwill is calculated on the basis of the number of past years profits. In this method, the goodwill is valued at an agreed number of years purchase of the average profits of the past few years. A number of years purchase means the period for which the business would be able to earn profit only on the basis of the Goodwill of the business.

There are two different methods of calculating average profit which are:

1. Simple average

2. Weighted average

Simple Average: In the simple average method, the goodwill is calculated by multiplying the average profit with the agreed number of years of purchase.

Step 1 – Find out normal profit by deducting abnormal gains & non-business incomes & adding abnormal losses & non-business expenses.

Step 2 – Average Profit = Total Profits/Number of years of profit & loss given

Step 3 - Goodwill = Average Profit x No. of years of purchase

Example of Simple Average Profit Method

The following illustration will help in understanding the concept of Average Profit method more clearly.

ABC & Co. has these profits in the following years

2010 – ₹5000

2011- ₹4000

2012- ₹5000

2013- ₹3000

2014- ₹5000

Calculate the goodwill at 4 years of purchase.

Solution

Average Profit = Total Profit / No.of years

= 5000+4000+5000+3000+5000

= 22000/5

= 4400

Goodwill = Average Profit x No. of years of purchase

= 4400 x 4

= 19600

Weighted Average: In the weighted average method, weights are assigned to the profits of each year with more weightage for the recent years. The goodwill is calculated by multiplying the weighted average profit with the number of years of purchase.

Weighted Average Profit = Sum of Weighted profits / Sum of weights

Goodwill = Weighted Average Profit x No. of years of purchase

If the profits remain constant over a period of a few years then there should be equal weightage given for all the years which is the simple average method.

If the profit is fluctuating every year then the preference shifts to the weighted average method with necessary weightage given to profits obtained from recent years.

Super Profit Method: In this method, goodwill is valued on the basis of excess profits earned by a firm in comparison to average profits earned by other firms. When a similar type of business earns a return as a certain percentage of the capital employed, it is called ‘normal return’. The excess of actual profit over the normal profit is called ‘Super Profits’.

For Ex – The other firms are earning profits within @ 15% return whereas a particular firm is earning profits @ 20%. This 5% of extra return is known as Super Profit.

Steps:

- Calculate Actual Average Profit i.e. [ Total Profit No. of Years ]

- Calculate Normal Profit i.e.

= Capital Employed × Normal Rate of Return 100

[Capital Employed = Total Assets – Outside Liabilities] - Find Out Super Profits

Super Profits = Actual Average Profit – Normal Profit

4. Calculate the Value of Goodwill

= Super profit × No. of years purchased

3. Capitalisation Methods: There are two ways of finding out the value of Goodwill through this method;

(a) By capitalizing the average profits

(b) By capitalizing the super-profits.

(a) Capitalisation of Actual Average Profit Method:

- Calculate actual average profit: [ Total Profit No. of Years ]

- Capitalize the average profit on the basis of the normal rate of return:

The capitalized value of the actual average profit

= Actual Average Profit × 100 Normal Rate of Return - Find out the actual capital employed:

Actual Capital Employed = Total Assets at their current value other than [Goodwill, Fictitious assets and non-trade investments] – Outside Liabilities. - Compute the value of Goodwill:

Goodwill = Capitalised value of actual average profit – Actual Capital Employed.

(b) Capitalisation of Super Profit Method:

1. Calculate Actual Capital Employed [same as above].

2. Calculate Super Profit [same as under Super Profit Method].

3. Multiply the Super Profit by the required rate of return multiplier:

Goodwill = Super Profit × 100 Normal Rate of Return

Treatment of Goodwill:

To compensate old partners for the loss (sacrifice) of their share in profits, the incoming partner, who acquires his share of profit from the old partners brings in some additional amount termed as a share of goodwill.

Goodwill, at the time of admission, can be treated in two ways:

- Premium Method

- Revaluation Method.

1. Premium Method:

The premium method is followed when the incoming partner pays his share of goodwill in cash. From the accounting point of view, the following are the different situations related to the treatment of goodwill:

(a) Goodwill (Premium) paid privately (directly to old partners)

[No entry is required]

(b) Goodwill (Premium) brought in cash through the firm

1. Cash A/c or Bank A/c Dr.

To Goodwill A/c

(For the amount of Goodwill brought by new partner)

2. Goodwill A/c Dr.

To Old Partner’s Capital A/c

(For the amount of Goodwill distributed among the old partners in their sacrificing ratio)

Alternatively:

1. Cash A/c or Bank A/c Dr.

To New Partner’s Capital A/c (For the amount of Goodwill brought b> a new partner)

2. New Partner’s Capital A/c Dr.

To Old Partner’s Capital A/c’s (For the amount of Goodwill distributed among the old partners in their sacrificing ratio)

3. If old partners withdrew goodwill (in full or in part) (if any)

Old Partner’s Capital A/c’s Dr.

To Cash A/c or Bank A/c

(For the amount of goodwill withdrawn by the old partners)

When goodwill already exists in books:

If the goodwill already exists in the books of firms and the incoming partner brings his share of goodwill in cash, then the goodwill appearing in the books will have to be written off.

Old Partner’s Capital A/c’s Dr.

To Goodwill A/c

(For Goodwill written-off in old ratio)

After the admission of the partner, all partners may decide to maintain the Goodwill Account in the books of accounts.

Goodwill A/c Dr.

To All Partner’s Capital A/c’s (For Goodwill raised in the new firm after admission of a new partner in new profit sharing ratio)

2. Revaluation Method:

If the incoming partner does not bring in his share of goodwill in cash, then this method is followed. In this case, the goodwill account is raised in the books of accounts. When goodwill account is to be raised in the books there are two possibilities:

(a) No goodwill appears in books at the time of admission.

(b) Goodwill already exists in books at the time of admission,

(a) No goodwill appears in the books:

Goodwill A/c Dr.

To Old Partner’s Capital A/c’s (For Goodwill raised at full value in the old ratio)

If the incoming partner brings in a part of his share of goodwill. In that case, after distributing the amount brought in for goodwill among the old partners in their sacrificing ratio, the goodwill account is raised in the books of accounts based on the portion of premium not brought by the incoming partner.

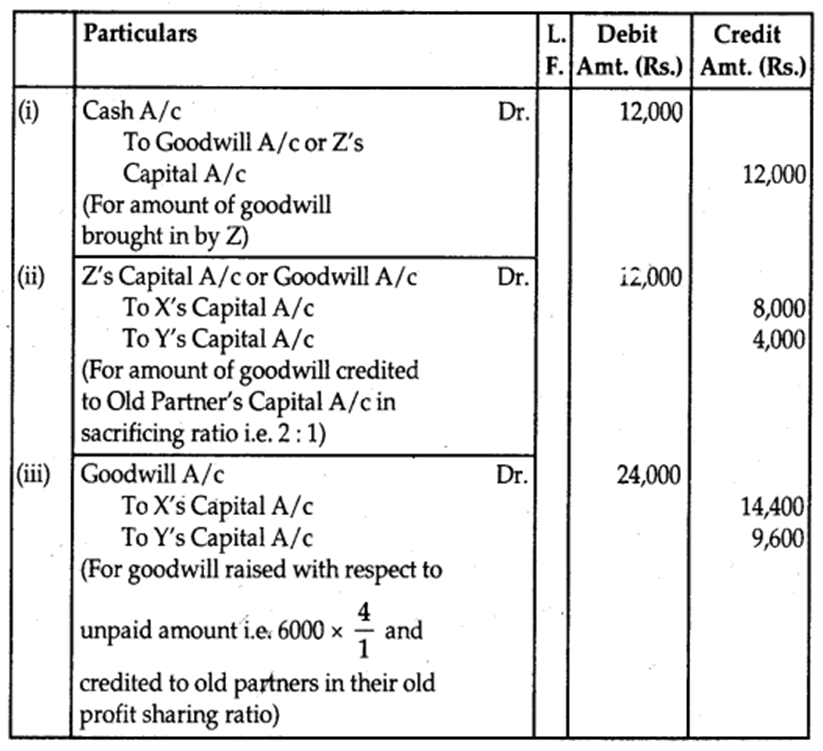

Example: X and Y are partners sharing profits in the ratio of 3: 2. They admit Z as a new partner. 14th share. The sacrificing ratio of X and Y is 2: 1. Z brings Rs. 12,000 as goodwill out of his share of Rs. 18,000. No goodwill account appears in the books of the firm.

Answer:

(b) When Goodwill already exists in the books

1. When the value of goodwill appearing in books is equal to the agreed value:

[No Entry is Required]

2. If the value of goodwill appearing in the books is less than the agreed value:

Goodwill A/c Dr.

To Old Partner’s Capital A/c’s (For Goodwill is raised to its agreed value)

3. If the value of goodwill appearing in the books is more than the agreed value:

Old Partner’s Capital A/c’s Dr.

To Goodwill A/c

(For Goodwill brought down to its agreed value)

If partners, after raising Goodwill in the books and making necessary adjustments decide that the goodwill should not appear in the firm’s balance sheet, then it has to be written off.

All Partners’ Capital A/c’s Dr.

To Goodwill A/c (For Goodwill written off)

Sometimes, the partners may decide not to show goodwill accounts anywhere in books.

New Partner’s Capital A/c Dr.

To Old Partner’s Capital A/c (For adjustment for New Partner’s Share of Goodwill)

Hidden or Inferred Goodwill:

1. To find out the total capital of the firm by new partner’s capital and his share of profit.

Example: New partner’s capital for the 14th share is Rs. 80,000, the entire capital of the new firm will be

80,000 × 41 = Rs. 3,20,000

2. To ascertain the existing total capital of the firm: We will have to ascertain the existing total capital of the new firm by adding the capital (of all partners, including new partner’s capital after adjustments, if any excluding goodwill)

If assets and liabilities are given:

Capital = Assets (at revalued figures) – Liabilities (at revalued figures)

3. Goodwill= Capital from (1) – Capital from (2)

Generally, this method is used, when the incoming partner does not bring his share of goodwill in cash. Here, we find out the total goodwill of the firm. After that, we can find out the new partner’s share of goodwill and treat accordingly.

3. Goodwill - Meaning, Nature & Valuation

- Books Name

- Vision classes Accountancy Book

- Publication

- Vision classes

- Course

- CBSE Class 12

- Subject

- Accountancy

Goodwill

Goodwill is also one of the special aspects of partnership accounts which requires adjustment (also valuation if not specified) at the time of reconstitution of a firm viz., a change in the profit sharing ratio, the admission of a partner or the retirement or death of a partner.

Meaning of Goodwill

Over a period of time, a well-established business develops an advantage of good name, reputation and wide business connections. This helps the business to earn more profits as compared to a newly set up business. In accounting, the monetary value of such advantage is known as “goodwill”. It is as an intangible asset. In other words, goodwill is the value of the reputation of a firm in respect of the profits expected in future over and above the normal profits. It is generally observed that when a person pays for goodwill,he/she pays for something, which places him in the position of being able to earn super profits as compared to the profit earned by other firms in the same industry.

In simple words, goodwill can be defined as “the present value of a firm’s anticipated excess earnings” or as “the capitalised value attached to the differential profit capacity of a business”. Thus, goodwill exists only when the firm earns super profits. Any firm that earns normal profits or is incurring losses has no goodwill.

Factors Affecting the Value of Goodwill

The main factors affecting the value of goodwill are as follows:

Nature of business: A firm that produces high value added products or having a stable demand is able to earn more profits and therefore has more goodwill.

2. Location: If the business is centrally located or is at a place having heavy customer traffic, the goodwill tends to be high.

3. Efficiency of management: A well-managed concern usually enjoys the advantage of high productivity and cost efficiency. This leads to higher profits and so the value of goodwill will also be high.

4. Market situation: The monopoly condition or limited competition enables the concern to earn high profits which leads to higher value of goodwill.

5. Special advantages: The firm that enjoys special advantages like import licences, low rate and assured supply of electricity, long-term contracts for supply of materials, well-known collaborators, patents, trademarks, etc. enjoy higher value of goodwill.

Need for Valuation of Goodwill

Normally, the need for valuation of goodwill arises at the time of sale of a business. But, in the context of a partnership firm it may also arise in the following circumstances:

1. Change in the profit sharing ratio amongst the existing partners;

2. Admission of new partner;

3. Retirement of a partner;

4. Death of a partner; and

5. Dissolution of a firm involving sale of business as a going concern.

6. Amalgamation of partnership firms.

Methods of Valuation of Goodwill

Since goodwill is an intangible asset it is very difficult to accurately calculate its value. Various methods have been advocated for the valuation of goodwill of a partnership firm. Goodwill calculated by one method may differ from the goodwill calculated by another method. Hence, the method by which goodwill is to be calculated, may be specifically decided between the existing partners and the incoming partner.

The important methods of valuation of goodwill are as follows:

1. Average Profits Method

2. Super Profits Method

3. Capitalisation Method

Average Profits Method

Under this method, the goodwill is valued at agreed number of ‘years’ purchase of the average profits of the past few years. It is based on the assumption that a new business will not be able to earn any profits during the first few years of its operations. Hence, the person who purchases a running business must pay in the form of goodwill a sum which is equal to the profits he is likely to receive for the first few years. The goodwill, therefore, should be calculated by multiplying the past average profits by the number of years during which the anticipated profits are expected to accrue.

For example, if the past average profits of a business works out at Rs. 20,000

and it is expected that such profits are likely to continue for another three years, the value of goodwill will be Rs. 60,000 (Rs. 20,000 × 3).

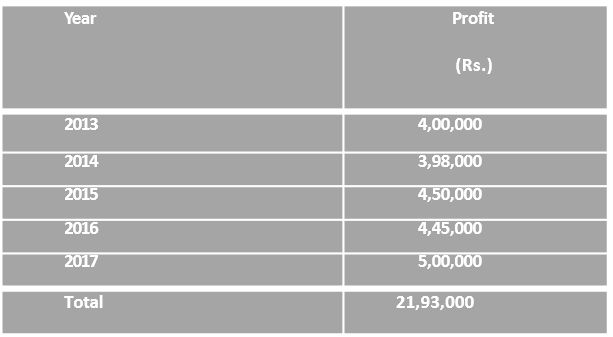

Revision 9

The profit for the five years of a firm are as follows – year 2013 Rs. 4,00,000; year 2014 Rs. 3,98,000; year 2015 Rs. 4,50,000; year 2016 Rs. 4,45,000 and year 2017 Rs. 5,00,000. Calculate goodwill of the firm on the basis of 4 years purchase of 5 years average profits.

Solution

Average Profit Total Profit of Last 5 Years/ No. of years

= Rs 21, 93, 000/5 = Rs 4, 38, 600

Goodwill = Average Profits x No. of years purchased

= Rs. 4,38,600 × 4 = Rs. 17,54,400

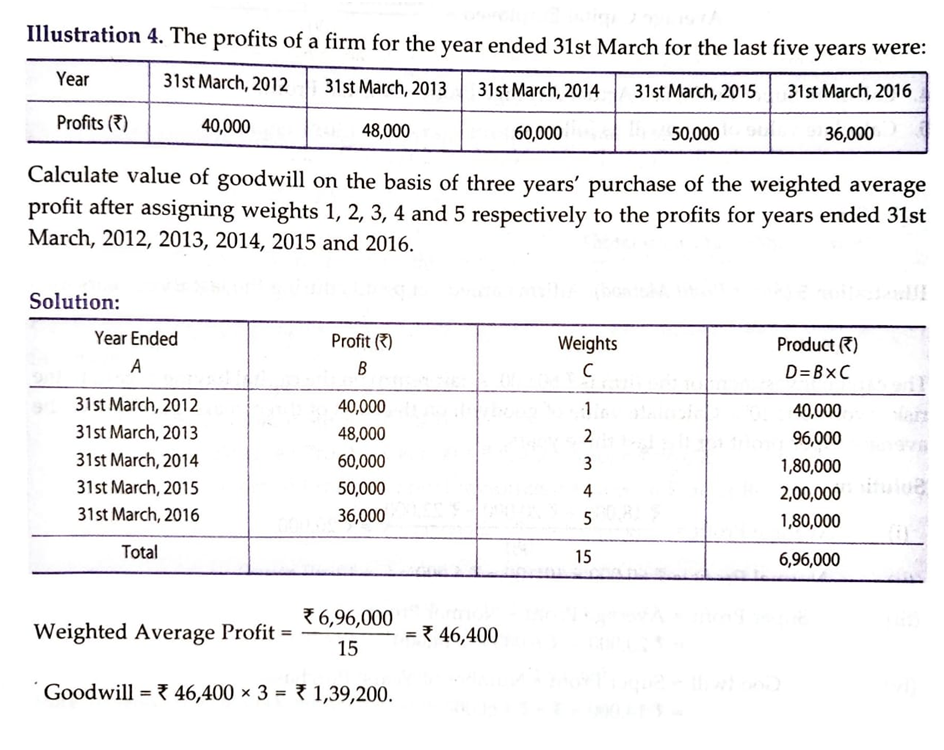

The above calculation of goodwill is based on the assumption that no change in the overall situation of profits is expected in the future. The above Revision is based on simple average. Sometimes, if there exists an increasing on decreasing trend, it is considered to be better to give a higher weightage to the profits to the recent years than those of the earlier years. Hence, it is a advisable to work out weighted average based on specified weights like 1, 2, 3, 4 for respective year’s profit. However, weighted average should be used only if specified. (See Revisions 10 and 11).

Revision 10

The profits of firm for the five years are as follows:

Solution

Weighted Average Profit = Rs 3, 48, 000/ 15 = Rs 23, 200

Goodwill = Rs. 23,200 × 3 = Rs. 69,600

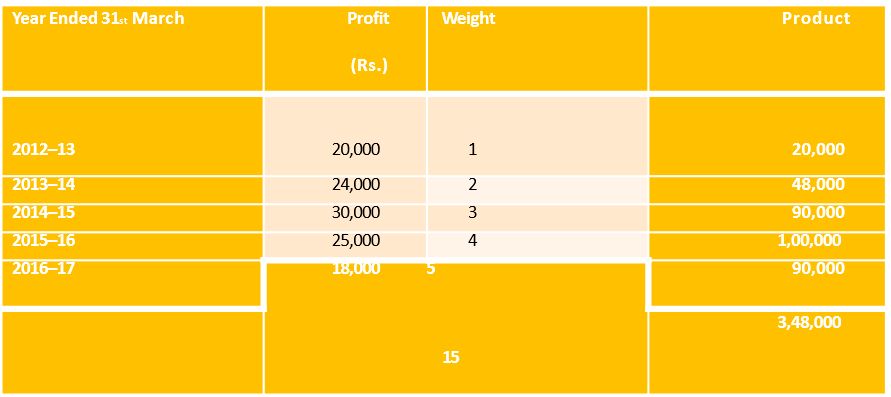

Revision 11

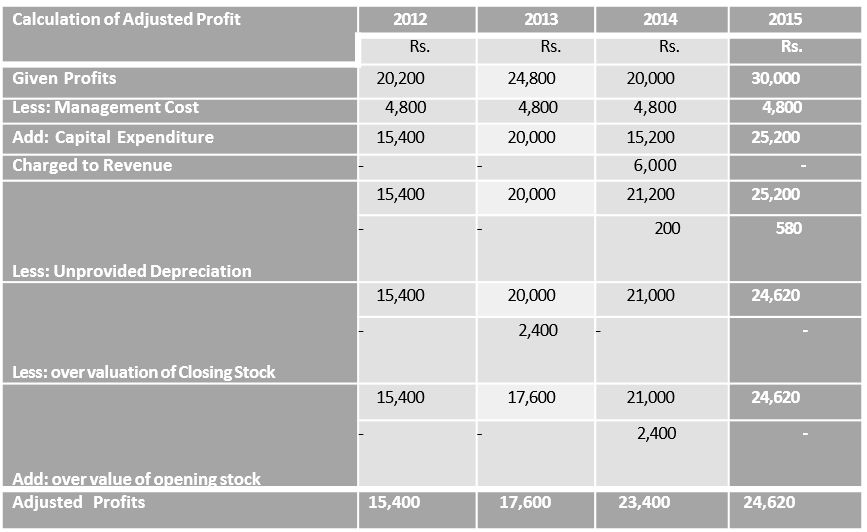

Calculate goodwill of a firm on the basis of three year’ purchase of the weighted average profits of the last four years. The profit of the last four years were: 2012 Rs. 20,200; 2013 Rs. 24,800; 2014 Rs. 20,000 and 2015 Rs. 30,000. The weights assigned to each year are : 2012 – 1; 2013 – 2; 2014 – 3 and 2015 – 4. You are supplied the following information:

1. On September 1, 2014 a major plant repair was undertaken for Rs. 6,000, which was charged to revenue. The said sum is to be capitalised for goodwill calculation subject to adjustment of depreciation of 10% p.a. on reducing balance method.

2. The Closing Stock for the year 2013 was overvalued by Rs. 2,400.

3. To cover management cost an annual charge of Rs. 4,800 should be made for purpose of goodwill valuation.

Solution

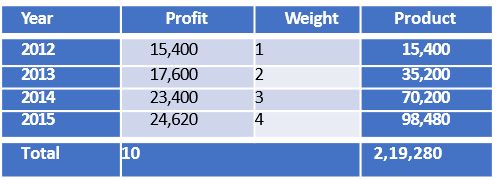

Calculation of weighted average profits:

Weight Average Profit = Rs 2, 19, 280/ 10 = Rs 21, 928

Goodwill = Rs. 21,928 × 3 = Rs. 65,784

Notes to Solution

- Depreciation of 2014 = 10% of Rs. 6000 for 4 months

- Depreciation of 2015 = 10% of Rs. 6000 – Rs. 200 for one year

- Closing Stock of 2014 will become opening stock for the year 2015.

Super Profits Method

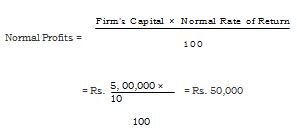

The basic assumption in the average profits (simple or weighted) method of calculating goodwill is that if a new business is set up, it will not be able to earn any profits during the first few years of its operations. Hence, the person who purchases an existing business has to pay in the form of goodwill a sum equal to the total profits he is likely to receive for the first ‘few years’. But it is contended that the buyer’s real benefit does not lie in total profits; it is limited to such amounts of profits which are in excess of the normal return on capital employed in similar business. Therefore, it is desirable to value, goodwill on the basis of the excess profits and not the actual profits. The excess of actual profits over the normal profits is termed as super profits.

![]()

Firms capital includes partners capital and reserves and surplus but excludes fictitious assets and goodwill. Suppose an existing firm earns Rs. 18,000 on the capital of Rs. 1,50,000 and the normal rate of return is 10%. The Normal profits will work out at Rs. 15,000 (1,50,000 × 10/100). The super profits in this case will be Rs. 3,000 (Rs. 18,000 – 15,000). The goodwill under the super profit method is ascertained by multiplying the super profits by certain number of years’ purchase. If, in the above example, it is expected that the benefit of super profits is likely to be available for 5 years in future, the goodwill will be valued at Rs. 15,000 (3,000 × 5). Thus, the steps involved under the method are:

- Calculate the average profit.

- Calculate the normal profit on the firm’s capital on the basis of the normal rate of return.

- Calculate the super profits by deducting normal profit from the average profits.

- Calculate goodwill by multiplying the super profits by the given number of years’ purchase.

Revision 12

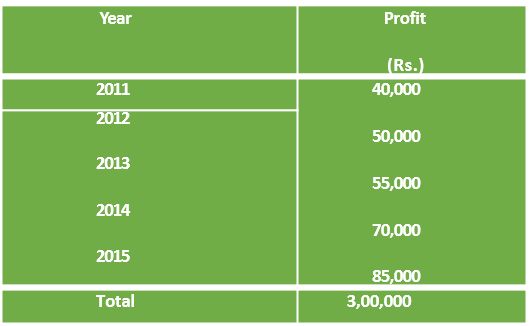

The books of a business showed that the firm’s capital employed on December 31, 2015, Rs. 5,00,000 and the profits for the last five years were: 2010–Rs. 40,000: 2012-Rs. 50,000; 2013-Rs. 55,000; 2014- Rs.70,000 and 2015-Rs. 85,000. You are required to find out the value of goodwill based on 3 years purchase of the super profits of the business, given that the normal rate of return is 10%.

Solution

Average Profits:

Average Profits = Rs. 3,00,000/5 = Rs. 60,000

Super Profit = Rs. 60,000 – Rs. 50,000 = Rs. 10,000

Revision 13

The capital of the firm of Anu and Benu is Rs. 1,00,000 and the market rate of interest is 15%. Annual salary to partners is Rs. 6,000 each. The profits for the last 3 years were Rs. 30,000; Rs. 36,000 and Rs. 42,000. Goodwill is to be valued at 2 years purchase of the last 3 years’ average super profits. Calculate the goodwill of the firm.

Solution

Interest on capital = 1,00,000 × 15/100 = Rs 15, 000 (i)

Normal Profit(i+ii) = Rs. 27,000

Average Profit = Rs. 30,000+Rs.36,000+Rs.42,000 = Rs. 1, 08, 000/3 = Rs 36, 000

Super Profit = Average Profit–Normal Profit

= Rs. 36,000–Rs. 27,000

= Rs. 9,000

Goodwill = Super Profit × No of years’ purchase

= Rs. 9,000 × 2

= Rs. 18,000

Capitalisation Method

Under this method the goodwill can be calculated in two ways: (a) by capitalizing the average profits, or (b) by capitalising the super profits.

(a) Capitalisation of Average Profits: Under this method, the value of goodwill is ascertained by deducting the actual firm’s capital in the business from the capitalized value of the average profits on the basis of normal rate of return. This involves the following steps:

(i) Ascertain the average profits based on the past few years’ performance.

(ii) Capitalize the average profits on the basis of the normal rate of return to ascertain the capitalised value of average profits as follows:

Average Profits × 100/Normal Rate of Return

(iii) Ascertain the actual firm’s capital (net assets) by deducting outside liabilities from the total assets (excluding goodwill and ficticious assets).

Firms’ Capital = Total Assets (excluding goodwill) – Outside Liabilities

Where outside Liabilities include both long term and short term Liabilities.

(iv Compute the value of goodwill by deducting net assets from the capitalised value of average profits, i.e. (ii) – (iii).

Revision 14

A business has earned average profits of Rs. 1,00,000 during the last few years and the normal rate of return in a similar business is 10%. Ascertain the value of goodwill by capitalisation average profits method, given that the value of net assets of the business is Rs. 8,20,000.

Solution

Capitalised Value of Average Profits

Rs 1, 00, 000 × 100/ 10 = Rs 10, 00, 000

Goodwill = Capitalised value – Net Assets

= Rs. 10,00,000 – Rs. 8,20,000

= Rs.1,80,000

(b Capitalisation of Super Profits: Goodwill can also be ascertained by capitalising the super profit directly. Under this method there is no need to work out the capitalised value of average profits. It involves the following steps.

- Calculate capital of the firm, which is equal to total assets (excluding goodwill and ficticious assets) minus outside liabilities.

- Calculate normal profits on capital employed.

- Calculate average profit for past years, as specified.

- Calculate super profits by deducting normal profits from average profits.

- Multiply the super profits by the required rate of return multiplier, that is, Goodwill = Super Profits × 100 Normal Rate of Return

In other words, goodwill is the capitalised value of super profits. The amount of goodwill worked out by this method will be exactly the same as calculated by capitalising the average profits.

Rs 18, 000 × 100/10 = Rs 1, 80, 000

Revision 15

1. The goodwill of a firm is to be worked out at three years’ purchase of the average profits of the last five years which are as follows:

2. The capital of the firm is Rs. 1,00,000 and normal rate of return is 8%, the average profits for last 5 years are Rs. 12,000 and goodwill is to be worked out at 3 years’ purchase of super profits.

3. Rama Brothers earn an average profit of Rs. 30,000 with a capital of

Rs. 2,00,000. The normal rate of return in the business is 10%. Using capitalisation of super profits method work out the value the goodwill of the firm.

Solution

1. Total Profits = Rs. 10,000 + Rs. 15,000 + Rs. 4,000 + Rs. 6,000 – Rs. 5,000 = Rs. 30,000

Average Profits = Rs. 30,000/5 = Rs. 6,000

2. Normal Profit = Rs.1,00,000 × 8 / 10 0 = Rs 8, 000

Super Profit=Average Profit – Normal profit = Rs. 12,000 – Rs. 8,000

= Rs 4, 000

3. Normal Profit= Rs. 2,00,000 × 10/100 = Rs. 20,000

Super Profit = Average Profit – Normal Profit = Rs. 30,000 – Rs. 20,000

= Rs 10, 000

Treatment of Goodwill

As stated earlier, the incoming partner who acquires his share in the profits of the firm from the existing partners brings in additional amount to compensate them for loss of their share in super profits. It is termed as his share of goodwill (also called premium for goodwill).

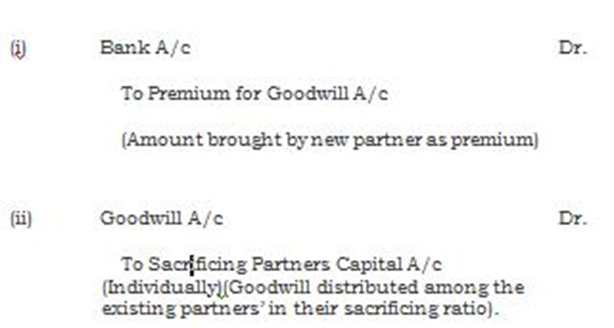

When the new Partner brings goodwill in cash.

The amount of premium brought in by the new partner is shared by the existing partners in their ratio of sacrifice. If this amount is paid to the old partners directly (privately) by the new partner, no entry is passed in the books of the firm. But, when the amount is paid through the firm, which is generally the case, the following journal entries are passed:

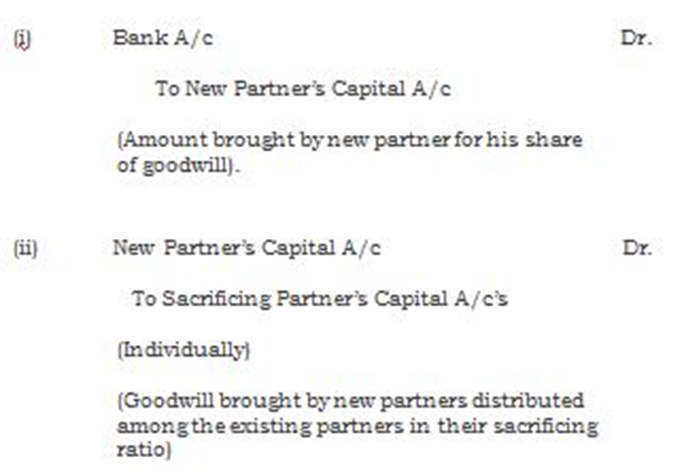

Alternatively, it is credited to the new partner’s capital account and then adjusted in favour of the existing partners in their sacrificing ratio. In that case the journal entries will be as follows:

If the partners decide that the amount of premium for goodwill credited to their capital accounts should be retained in business, an additional entry is not passed. If, however, they decide to withdraw their amounts, (in full or in part) the following additional entry will be passed:

Existing Partner’s Capital A/c (Individually)

Dr. To Bank A/c

(The amount of goodwill withdrawn by the existing partners)

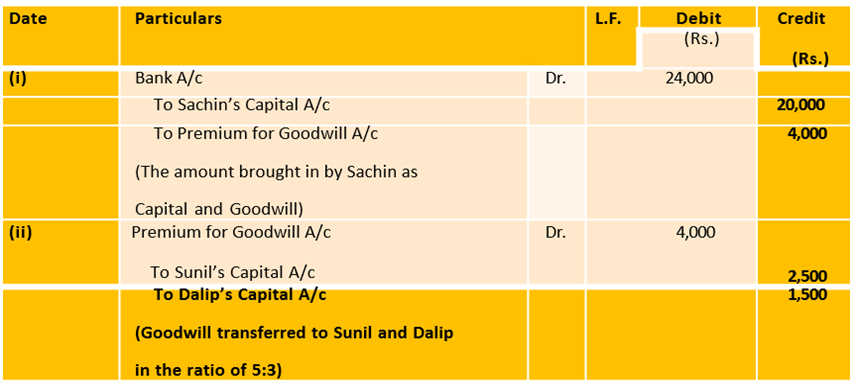

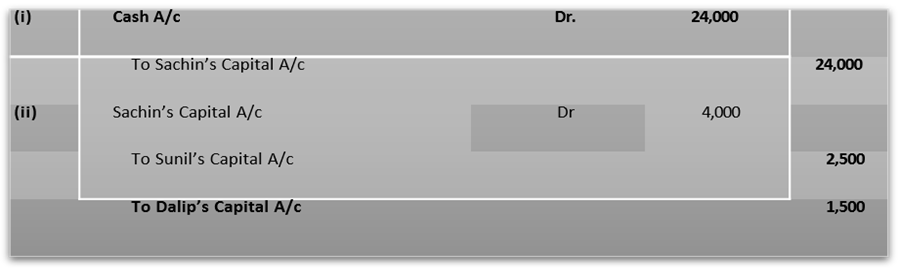

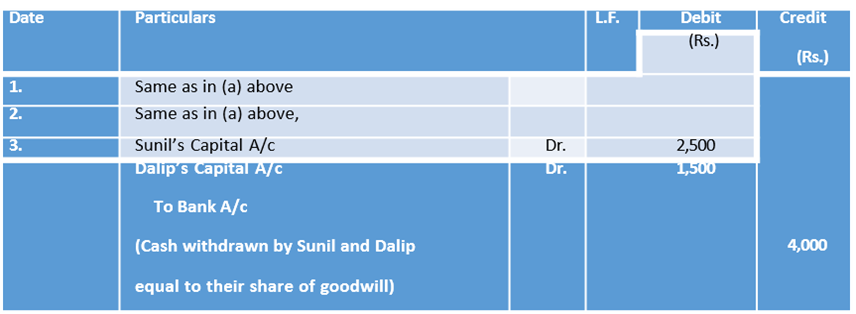

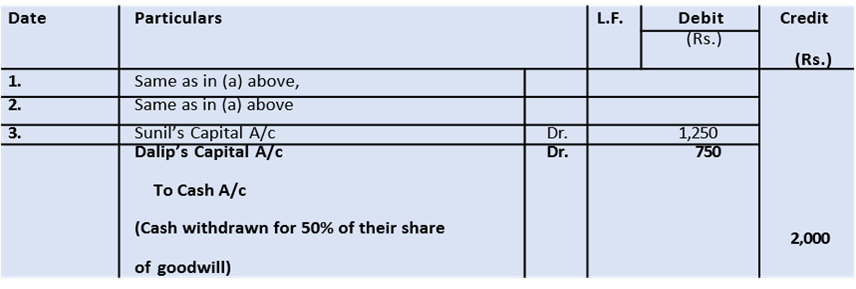

Revision 16

Sunil and Dalip are partners in a firm sharing profits and losses in the ratio of

Sachin is admitted in the firm for 1/5th share of profits. He brings in Rs. 20,000 as capital and Rs. 4,000 as his share of goodwill by cheque. Give the necessary journal entries,

(a) When partners decided to retain goodwill in business.

(b) When the amount of goodwill is fully withdrawn.

(c) When 50% of the amount of goodwill is withdrawn.

Solution

(a) When the amount of goodwill credited to existing partners is retained in business.

Books of Sunil and Dalip Journal

Alternatively,

Note: It assumed that the sacrificing ratio is the same as old profit sharing ratio.

(b) When the amount of goodwill credited to existing partners is fully withdrawn.

Journal

(c) When 50% of the amount of goodwill credited to existing partners is withdrawn.

Journal

Revision 17

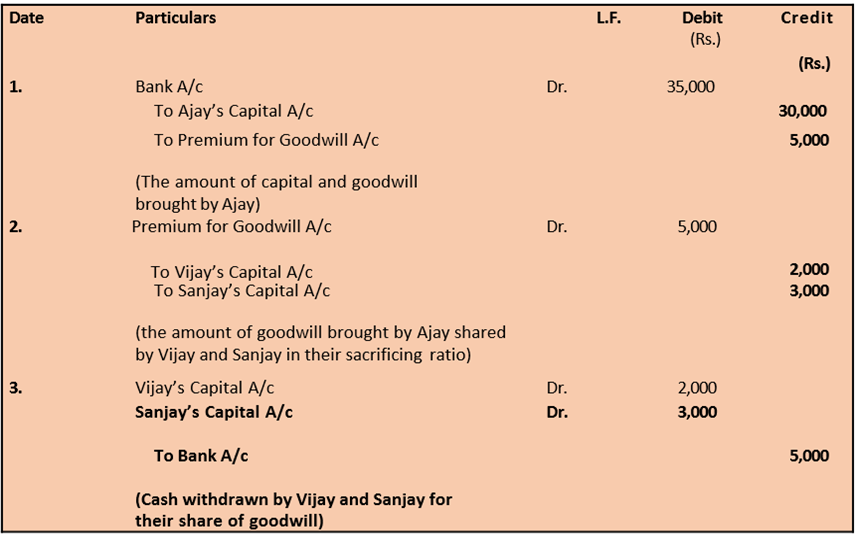

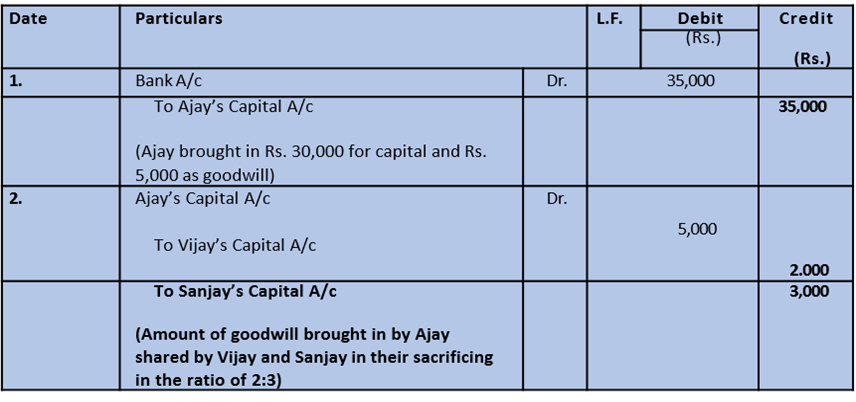

Vijay and Sanjay are partners in a firm sharing profits and losses in the ratio of 3:2. They admitted Ajay into partnership with 1/4 share in profits. Ajay brings in Rs. 30,000 for capital and the requisite amount of premium in cash. The goodwill of the firm is valued at Rs. 20,000. The new profit sharing ratio is 2:1:1. Vijay and Sanjay withdraw their share of goodwill. Give necessary journal entries.

Solution

(a) Ajay will bring Rs. 5,000 (1/4 of Rs. 20,000) as his share of goodwill (premium)

(b) Sacrificing Ratio is 2:3 as calculated below:

For Sanjay, old ratio is 2/5 and the new ratio is 1/4, hence, his sacrificing Ratio is = 2/5 – ¼ = 8 – 5/20 = 3/20

Books of Vijay and Sanjay Journal

Note: Alternatively, journal entries (1) and (2) could be as follows

Books of Vijay and Sanjay Journal

When goodwill already exists in books: Goodwill, if existing in the books of the firm, it is written off at the time of admission of a partner.

For example, in Revision 17, the goodwill of the firm is valued at Rs. 20,000 and Ajay who is admitted to 1/4 share in its profits, brings in Rs. 5,000 as his share of goodwill. Suppose, goodwill already appeared in books at Rs. 10,000 the following additional journal entry shall be passed for writing off the existing amount of goodwill.

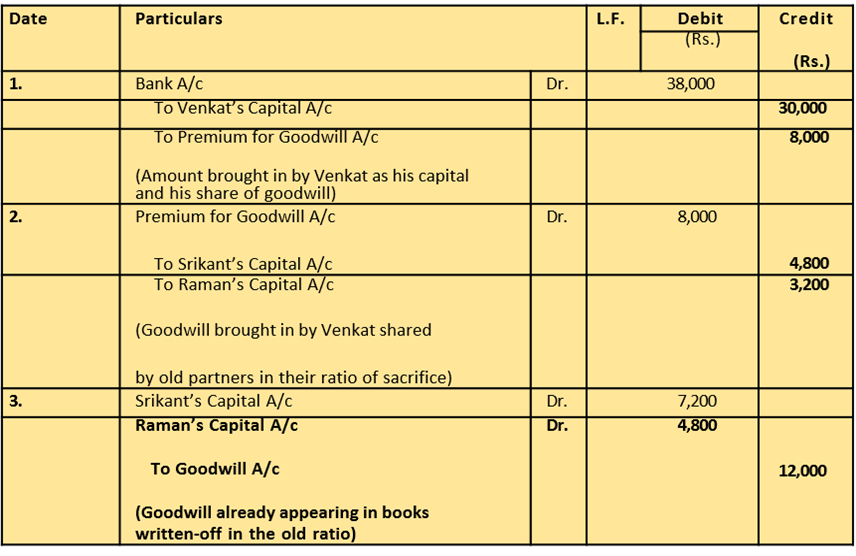

Revision 18

Srikant and Raman are partners in a firm sharing profits and losses in the ratio of 3:2. They admit Venkat into partnership with 1/3 share in the profits. Venkat brings in Rs. 30,000 as his capital. He also brings in the necessary amount for his share of goodwill. On the date of admission, the goodwill is valued at Rs. 24,000 and the goodwill account appears in the books at Rs.

12,000. Venkat brings in the necessary amount for his share of goodwill and agrees that the existing goodwill account be written off. Record the necessary journal entries in the books of the firm.

Solution

Books of Srikant and Raman Journal

Note: Since nothing is given about the ratio in which the new partner acquires his share of profit from Srikant and Raman, it is implied that they sacrifice their share of profit in favour of Venkat in the old ratio i.e., 3:2.

When the new partner does not bring goodwill in cash, partly or fully Goodwill not brought by the new partner will be debited to current account of new partner while sacrificing partners' capital accounts will be credited for their respective shares. When the new partner does not bring the share of goodwill, there exists two possibilities :

(a) Goodwill does not exist in the books.

(b) Goodwill exists in the books.

Goodwill does not exist in the books.

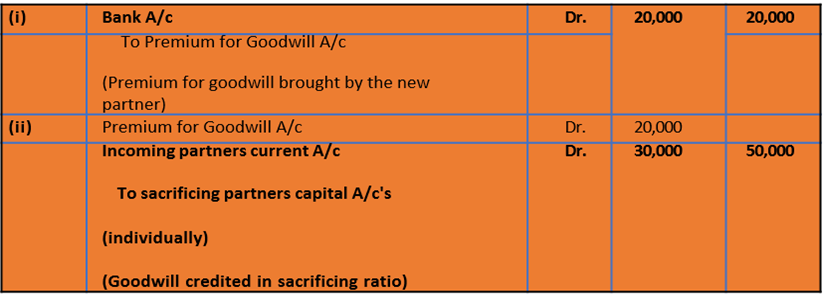

When goodwill does not exist in the books, sacrificing partners are credited with their share of goodwill and new partner is debited by the amount of goodwill not brought by him. The journal entry in this case is :

Incoming (New) Partners Current A/c Dr.

To Sacrificing Partners Capital A/c (individually) (Account of goodwill not brought in by new partner) Sometimes the new partner brings part of premium for goodwill in cash. In such a situation, new partners current account will be debited by the amount not brought by new partner.

For example, for the share of goodwill of Rs. 50,000 the new partner brings

Rs. 20,000 only. In this situation the journal entry will be :

Revision 19

Ahuja and Barua are partners in a firm sharing profits and losses in the ratio of

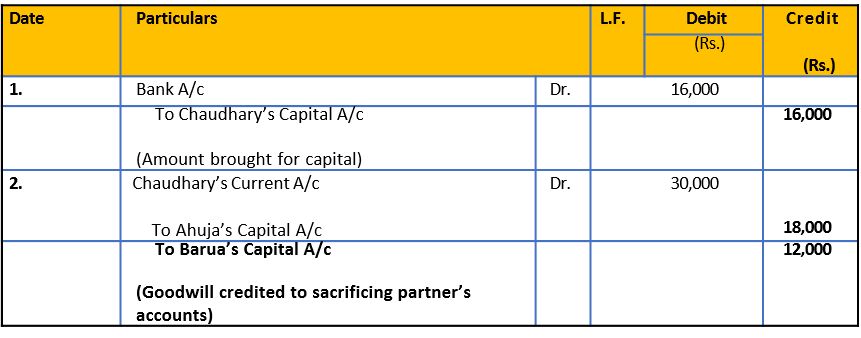

3:2. They decide to admit Chaudhary into partnership for 1/5 share of profits, which he acquires equally from Ahuja and Barua. Goodwill is valued at Rs. 30,000. Chaudhary brings in Rs. 16,000 as his capital but is not in a position to bring any amount for goodwill. No goodwill account exists in books of the firm. Goodwill account is to be raised at full value. Record the necessary journal entries.

Solution

Book of Ahuja and Barua Journal

When goodwill exists in the books

Goodwill appearing in the books will be written-off by debiting old partners' capital accounts in their old profit sharing ratio. Thereafter new value of goodwill will be given effect by crediting sacrificing partners' capital accounts and debiting new partners' current account.

Revision 20

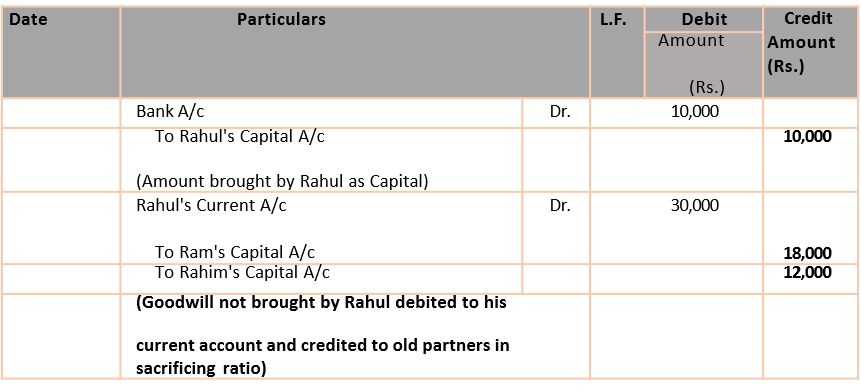

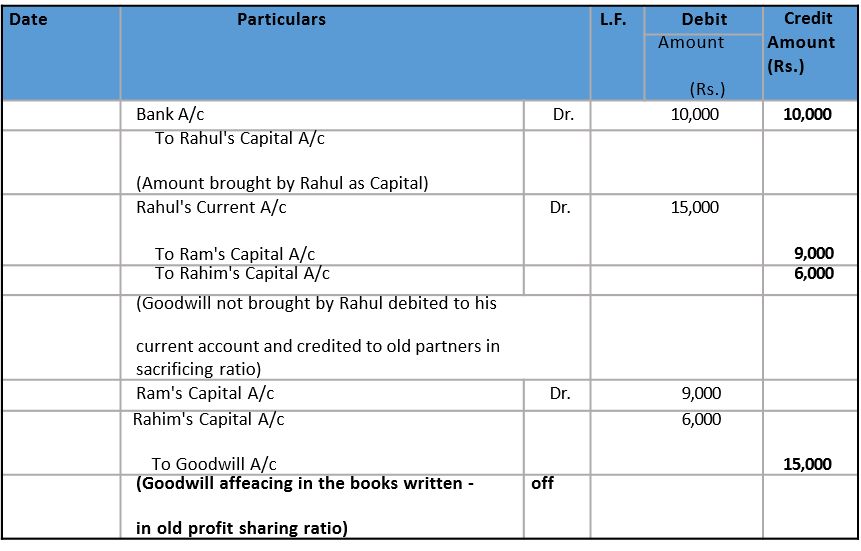

Ram and Rahim are partners in a firm sharing profits and losses in the ratio of

3:2. Rahul is admitted into partnership for 1/3 share in profits. He brings in Rs.

10,000 as capital, but is not in a position to bring any amount for his share of

goodwill which has been valued at Rs. 30,000. Give necessary journal entries under each of the following situations:

(a) When there is no goodwill appearing in the books of the firm; and

(b) When the goodwill appears at Rs 15,000 in the books of the firm;

Solution

(a) When no goodwill appears in the books

Books of Ram and Rahim Journal

(b) When goodwill appears in the books at Rs. 15,000

Applicability of Accounting Standard 26: Intangible Assets

The Standard comes into effect in respect of expenditure incurred on intangible items during the accounting periods commencing on or after April 1, 2003. As per the Standard, Intangible Asset under AS 26 is defined as an identifiable, non monetary, without physical existence and held for use in the production or supply of goods or services for rental to others or for administrative purposes.

Significant requirements of AS 26 w.r.t Intangible Assets:

1. Intangible asset should be recognised by fulfilling the criteria as recognized under AS 26.

2. If an in asset does not satisfy recognition criteria, it should be expensed.

3. Internally generated goodwill should not be recognised as an asset.

4. Internally generated brands, mastheads, and publishing titles and other similar in substance should not be recognised as intangible assets.

5. Internally generated assets other than the goodwill, brands, mastheads, and publishing titles may be recognised provided they satisfy recognition criteria as prescribed by AS 26.

6. Intangible assets should be written off as early as possible but not exceeding its estimated life, which normally should not be beyond 10 years.

Accounting Standard 26 implies that:

(a) Purchased goodwill may be accounted for in the books and shown as an asset, where it is accounted for in the books and shown as assets, it should be written off as early as possible, but where it is to be written- off in more than one accounting year, it should be written off in a period not exceeding 10 years. In line with what is prescribed by the Accounting Standard, goodwill appearing in the balance sheet in written off at the time of firm's reconstitution.

(b) Self - generated goodwill is not accounted for in the books and shown as an asset. Thus if self generated goodwill be debited to goodwill account it should be written - off in the same financial year and should not be shown as an asset in the balance sheet. Alternatively value of goodwill may be adjusted by deducting new partners' current account and crediting in their sacrificing ratio. The effect under both the methods is same.

Hidden Goodwill

Sometimes the value of goodwill is not given at the time of admission of a new partner. In such a situation it has to be inferred from the arrangement of the capital and profit sharing ratio. Suppose, A and B are partners sharing profits equally with capitals of Rs. 45,000 each. They admitted C as a new partner for one-third share in the profit. C brings in Rs. 60,000 as his capital. Based on the amount brought in by C and his share in profit, the total capital of the newly constituted firm works out to be Rs.1,80,000 (Rs. 60,000 × 3). But the actual total capital of A, B and C works out as Rs. 1,50,000 (Rs. 45,000 + Rs. 45,000

+ Rs. 60,000). Hence, it can be inferred that the difference is on account of goodwill i.e., Rs. 30,000 (Rs. 1,80,000 – Rs. 1,50,000). Which is to be shared equally (old ratio) by A and B. This shall raise their capital accounts to Rs. 60,000 each and total capital of the firm to Rs. 1,80,000. In this, C’s Current account will be debited by Rs. 10,000 (his share of goodwill) and A and B’s Capital accounts credited by Rs. 5,000 each.

Revision 22

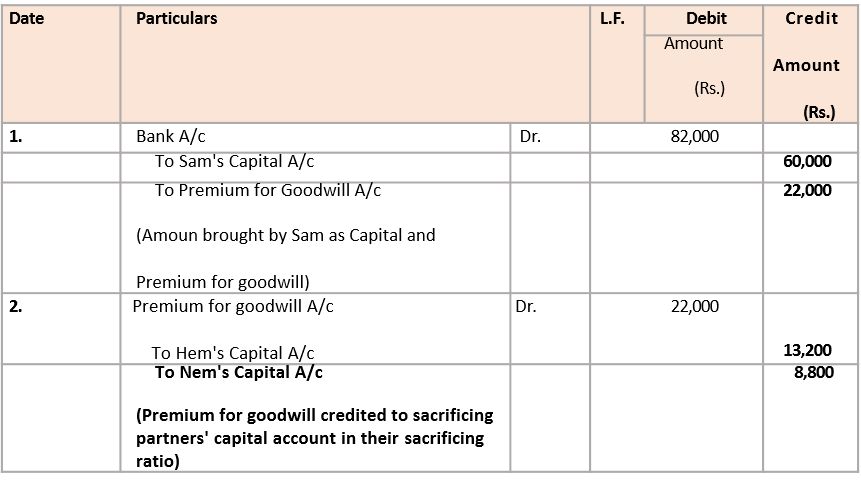

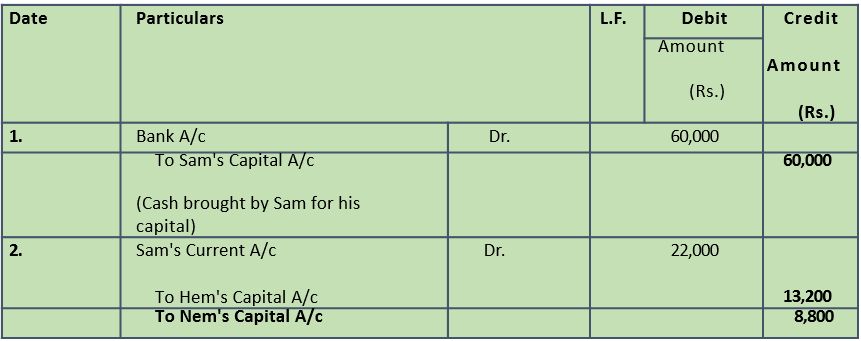

Hem and Nem are partners in a firm sharing profits in the ratio of 3:2. Their capitals were Rs. 80,000 and Rs. 50,000 respectively. They admitted Sam on Jan. 1, 2017 as a new partner for 1/5 share in the future profits. Sam brought Rs. 60,000 as his capital. Calculate the value of goodwill of the firm and record necessary journal entries on Sam’s admission, if:

(a) Sam brings his share of goodwill

(b) Sam does not bring his share of goodwill

Solution

(a) Sam brings his share of goodwill

Books of Hem, Nem and Samb Journal

(b) Sam does not bring his share of goodwill

Books of Hem, Nem and Sam Journal

Working Notes :

Value of Firm's goodwill

Sam's Capital = Rs. 60,000

4. Adjustments of accumulated profits & losses,

Adjustment for Accumulated (Undistributed) Profits and Losses:

1. For Undistributed Profits, Reserves etc.

(For distribution of accumulated profits and reserves to old partners in old profit sharing ratio)

General Reserves A/c Dr.

Reserve fund A/c Dr.

Profit and Loss A/c Dr.

Workmen’s Compensation Fund A/c Dr.

To Old Partner’s Capital A/c’s

(For distribution of accumulated profits and reserves to old partners in old profit sharing ratio)

2. For Undistributed Losses:

Old Partner’s Capital A/c’s Dr.

To Profit and Loss A/c

(For distribution of accumulated losses to old partners in old profit sharing ratio)

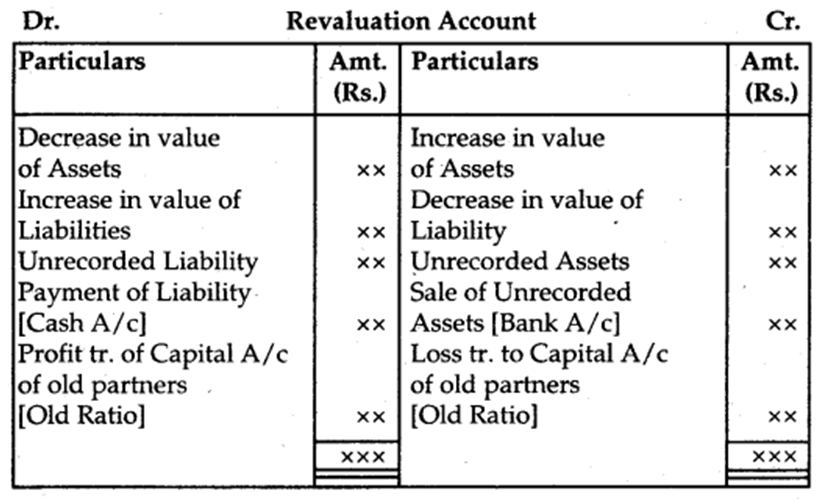

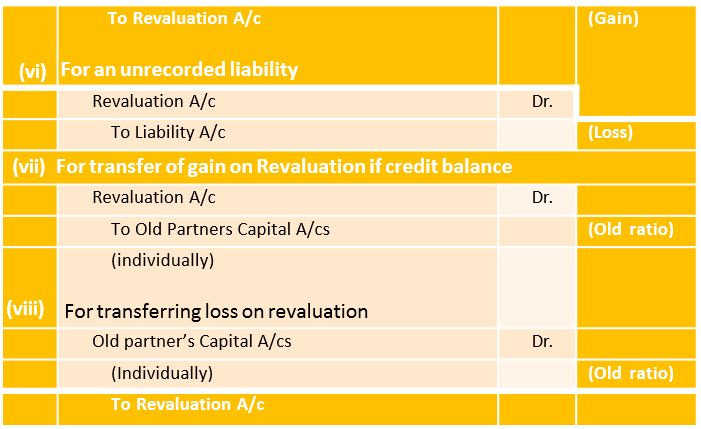

Revaluation of Assets and Reassessment of Liabilities: Revaluation of Assets and Reassessment of Liabilities is done with the help of ‘Revaluation Account’ or ‘Profit and Loss Adjustment Account’.

The journal entries recorded for revaluation of assets and reassessment of liabilities are the following:

1. For increase in the value of an Assets

Assets A/c Dr.

To Revaluation A/c (Gain)

2. For decrease in the value of an Assets

Revaluation A/c Dr.

To Assets A/c (Loss)

3. For appreciation in the amount of Liability

Revaluation A/c Dr.

To Liability A/c (Loss)

4. For reduction in the amount of a Liability

Liability A/c Dr.

To Revaluation A/c (Gain)

5. For recording an unrecorded Assets

Unrecorded Assets A/c Dr.

To Revaluation A/c (Gain)

6. For recording an unrecorded Liability

Revaluation A/c Dr.

To Unrecorded Liability A/c (Loss)

7. For the sale of unrecorded Assets

Cash A/c or Bank A/c Dr.

To Revaluation A/c (Gain)

8. For payment of unrecorded Liability

Revaluation A/c Dr.

To Cash A/c or Bank A/c (Loss)

9. For transfer of gain on Revaluation if the credit balance

Revaluation A/c Dr.

To Old Partner’s Capital A/c’s (Old Ratio)

10. For transfer of loss on Revaluation if debit balance

Old Partner’s Capital A/c’s Dr.

To Revaluation A/c (Old Ratio)

Adjustment of Capitals:

1. When the new partner brings in proportionate capital OR On the basis of the old partner’s capital.

(a) Calculate the adjusted capital of old partners (after all adjustments)

(b) Total capital of the firm

= Combined Adjusted Capital × Reciprocal proportion of the share of old partners

(c) New Partner’s Capital

= Total Capital × Proportion of share of a new partner.

2. On the basis of the new partner’s capital:

(a) Total Capital of the firm = New Partner’s Capital × Reciprocal proportion of his share.

(b) Distribute Total Capital in New Profit Sharing Ratio.

(c) Calculate adjusted capital of old partners.

(d) Calculate the difference between New Capital and Adjusted Capital.

- If the debit side of the Capital Account is bigger then it means he has excess capital

Partner’s ( capital Accounts Dr.

To Cash A /c or Bank A/c or Current A/c - If the credit side is bigger then it means that he has short capital

Cash A/c or Bank A/c or Current A/c Dr.

To Partner’s Capital A/c’s

Change in Profit Sharing Ratio among the Existing Partners:

Sometimes the existing partners of the firm may decide to change their profit-sharing ratio. In such a case, some partners will gain in future profits and some will lose. Here the gaining partners should compensate the losing partners unless otherwise agreed upon. In such a situation, first of all, the loss and gain in the value of goodwill (if any) will have to adjust.

1. Goodwill A/c Dr.

To Partner’s Capital A/c’s (For raising the amount of Goodwill in old ratio)

2. Partner’s Capital A/c’s Dr.

To Goodwill A/c

(For writing off the amount of Goodwill in New Profit sharing ratio)

Alternatively:

Gaining Partner’s Capital A/c’s Dr.

To Losing Partner’s Capital A/c’s (For adjustment due to change in profit sharing ratio)

Accounting Treatment of Goodwill

In case of change in profit sharing ratio, the gaining partner must components the sacrificing partner by paying the proportionate amount of goodwill.

Note :(i) Increase in the value of an Asset and decrease in the value of a liability result in profit.

Assets A/cDr.

To Revaluation

(ii) Decrease in the value of any asset and increase in the value of liability gives loss.

Revaluation A/cDr.

To Assets A/c

(iii) For an increase in the value of liabilities.

Revaluation A/cDr.

To Liabilities A/c

(Increase in value of Liability)

(iv) For a decrease in the value of Liabilities

Liabilities A/cDr.

To Revaluation A/c

(Decrease in the value of Liabilities)

(v) When the Revaluation account shows profit

Revaluation A/cDr.

To Partner’s Capital A/c

(Profit credited to Partner’s Capital A/c in old ratio)

(vi) In case of Revaluation Loss

Partner’s Capital A/c’sDr.

To Revaluation A/c

(Loss debited to Partner’s Capital A/cs in old ratio)

4. Adjustments of accumulated profits & losses,

- Books Name

- Vision classes Accountancy Book

- Publication

- Vision classes

- Course

- CBSE Class 12

- Subject

- Accountancy

Adjustment for Accumulated Profits and Losses And Revaluation of Assets and Reassessment of Liabilities

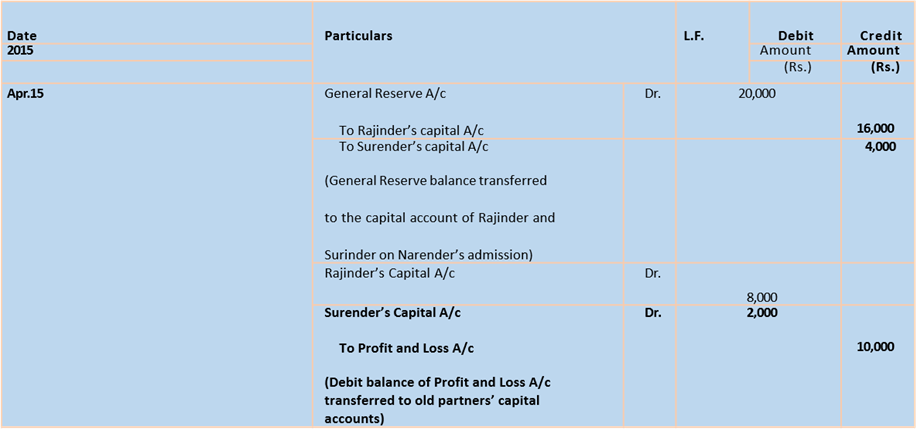

Sometimes a firm may have accumulated profits not yet transferred to capital accounts of the partners. These are usually in the form of general reserve, reserve and/or Profit and Loss Account. The new partner is not entitled to have any share in such accumulated profits. These are distributed among the partners by transferring it to their capital current accounts in old profit sharing ratio. Similarly, if there are some accumulated losses in the form of a debit balance of profit and loss account and/or deferred revenue expenditure appearing in the balance sheet of the firm. It should be transferred to the old partners’ capital accounts (see Revision 23).

Revision 23

Rajinder and Surinder are partners in a firm sharing profits in the ratio of 4:1. On April 15, 2017 they admit Narender as a new partner. On that date there was a balance of Rs. 20,000 in general reserve and a debit balance of Rs. 10,000 in the profit and loss account of the firm. Pass necessary journal entries regarding adjustment of a accumulate a profit or loss.

Solution

Books of Rajinder, Surinder and Narender Journal

At the time of admission of a new partner, it is always desirable to ascertain whether the assets of the firm are shown in books at their current values. In case the assets are overstated or understated, these are revalued. Similarly, a reassessment of the liabilities is also done so that these are brought in the books at their correct values. At times there may also be some unrecorded assets and liabilities of the firm. These also have to be brought into the books of the firm. For this purpose the firm has to prepare the Revaluation Account. The gain or loss on revaluation of each asset and liability is transferred to this account and finally its balance is transferred to the capital accounts of the old partners in their old profit sharing ratio. In other words, the revaluation account is credited with increase in the value of each asset and decrease in its liabilities because it is a gain and is debited with decrease in the value of assets and increase in its liabilities is debited to revaluation account because it is a loss. Similarly unrecorded assets are credited and unrecorded liabilities are debited to the revaluation account. If the revaluation account finally shows a credit balance then it indicates net gain and if there is a debit balance then it indicates net loss. Which will be transferred to the capital accounts of the old partners in old ratio.

The journal entries recorded for revaluation of assets and reassessment of liabilities are as follows:

(i) For increase in the value of an asset

Asset A/c Dr.

To Revaluation A/c (Gain)

(ii) For reduction in the value of an asset

Revaluation A/c Dr.

To Asset A/c (Loss)

(iii) For appreciation in the amount of a liability

Revaluation A/c Dr.

To Liability A/c (Loss)

(iv) For reduction in the amount of a liability

Liability A/c Dr.

To Revaluation A/c (Gain)

(v) For an unrecorded asset

Asset A/c Dr.

Note: Entries (i), (ii), (iii) and (iv) are recorded only with the amount increase and decrease in the value of assets and liabilities.

Revision 24

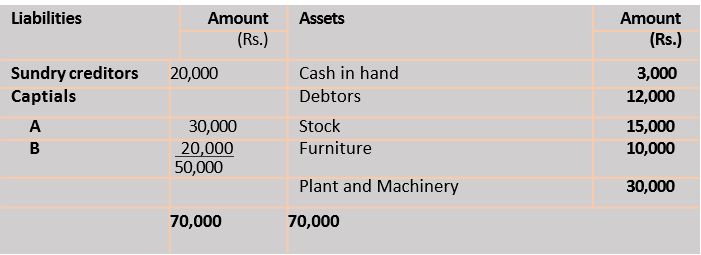

Following in Balance Sheet of A and B who share profits in the ratio of 3:2.

Balance Sheet of A and B as on April 1, 2015

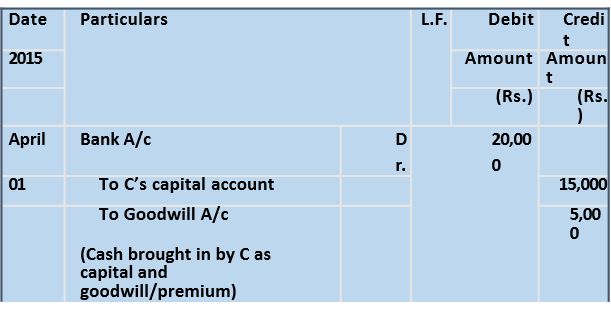

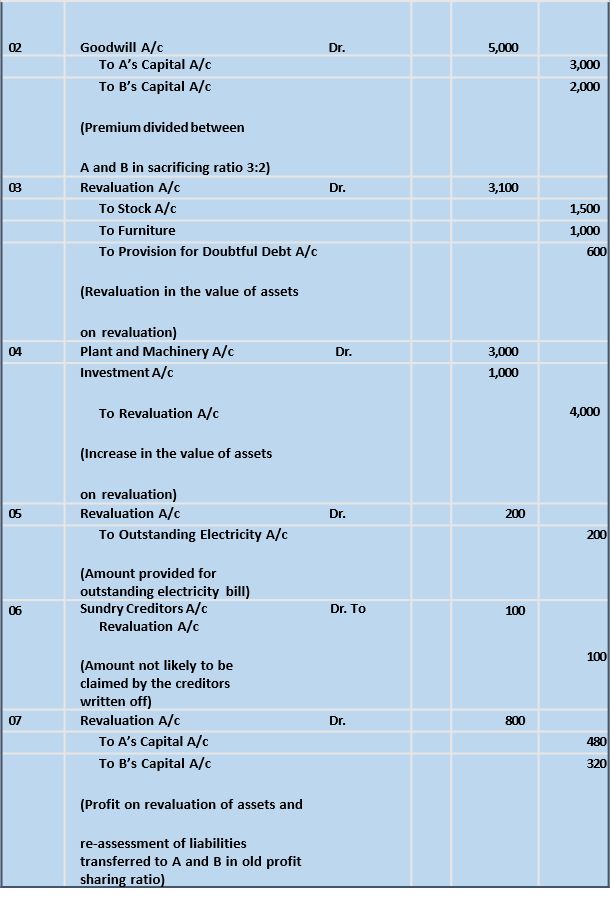

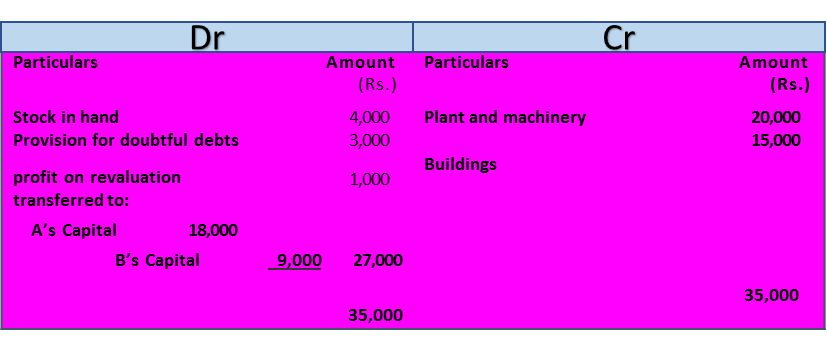

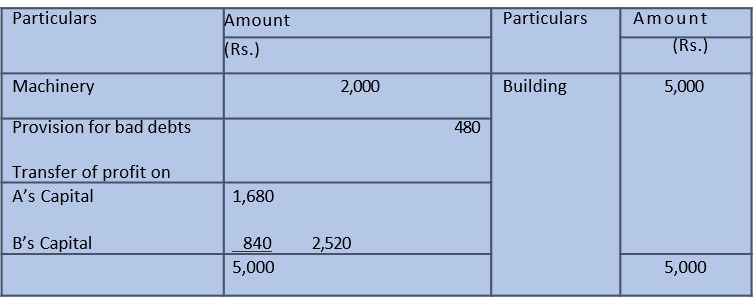

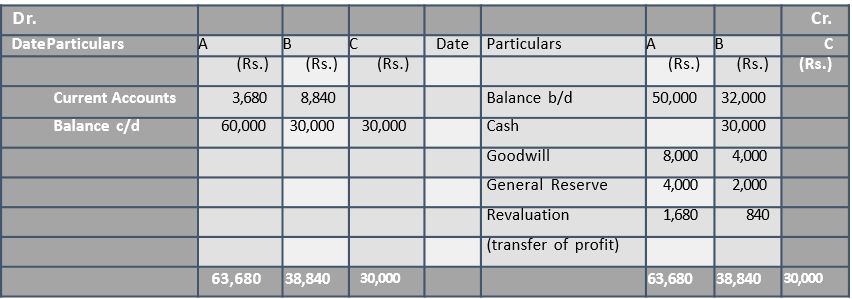

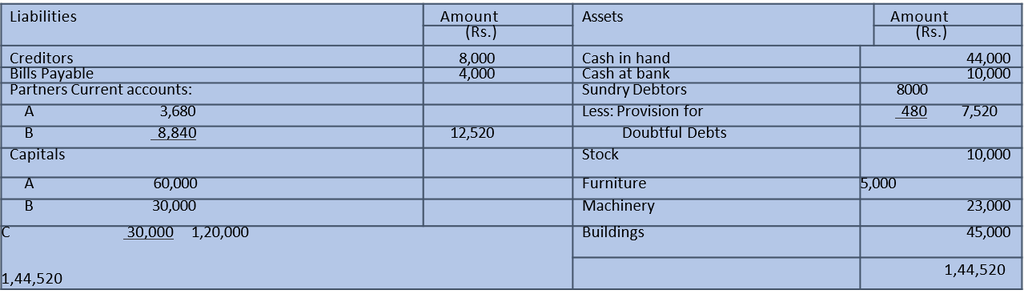

On that date C is admitted into the partnership on the following terms:

- C is to bring in Rs. 15,000 as capital and Rs. 5,000 as premium for goodwill for 1/6 share.

- The value of stock is reduced by 10% while plant and machinery is appreciated by 10%.

- Furniture is revalued at Rs. 9,000.

- A provision for doubtful debts is to be created on sundry debtors at 5% and Rs. 200 is to be provided for an electricity bill.

- Investment worth Rs. 1,000 (not mentioned in the balance sheet) is to be taken into account.

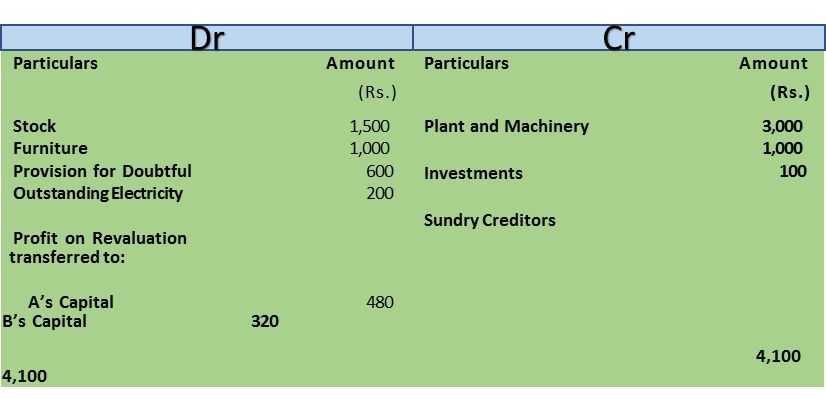

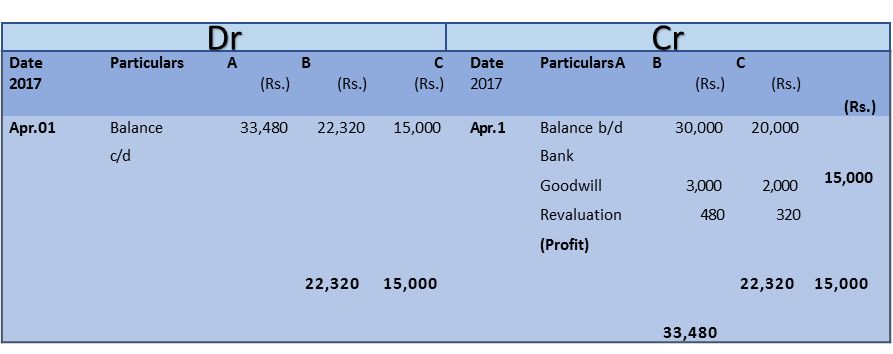

- A creditor of Rs. 100 is not likely to claim his money and is to be written off.Record journal entries and prepare revaluation account and capital account of partners.

Books of A, B and C Journal

Revaluation Account

Partner’s Capital Accounts

Revision 25

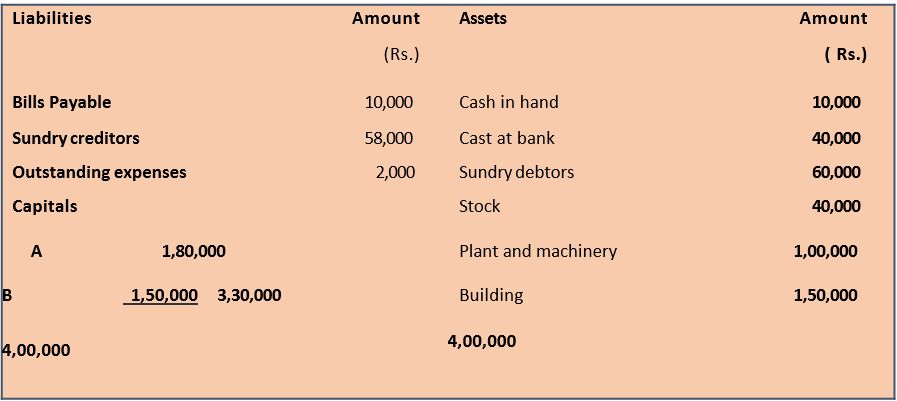

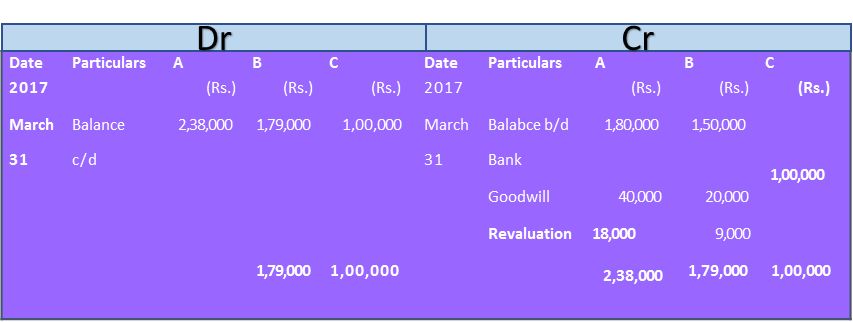

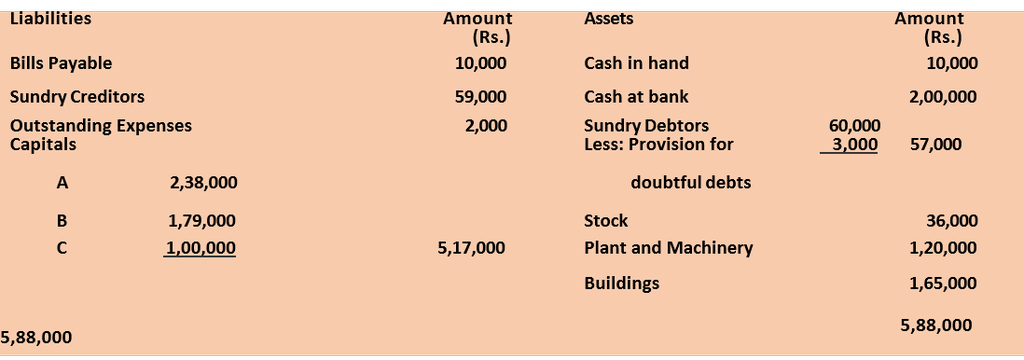

Given below is the Balance Sheet of A and B, who are carrying on partnership business as on March 31,2017. A and B share profits in the ratio of 2:1.

Balance Sheet of A and B as at March 31, 2017

C is admitted as a partner on the date of the balance sheet on the following terms:

1. C will bring in Rs 1,00,000 as his capital and Rs 60,000 as his share of

goodwill for 1/4 share in profits.

2. Plant is to be appreciated to Rs 1,20,000 and the value of buildings is to appreciated by 10%.

3. Stock is found overvalued by Rs 4,000.

4. A provision for doubtful debts is to be created at 5% of debtors.

5. Creditors were unrecorded to the extend of Rs 1,000.

Record revaluation Account, partners’ capital accounts, and the Balance Sheet of the constituted firm after admission of the new partner.

Solution

Books of A and B Revaluation Account

Balance Sheet of A, B and C as on April 01, 2016

Adjustment of Capitals

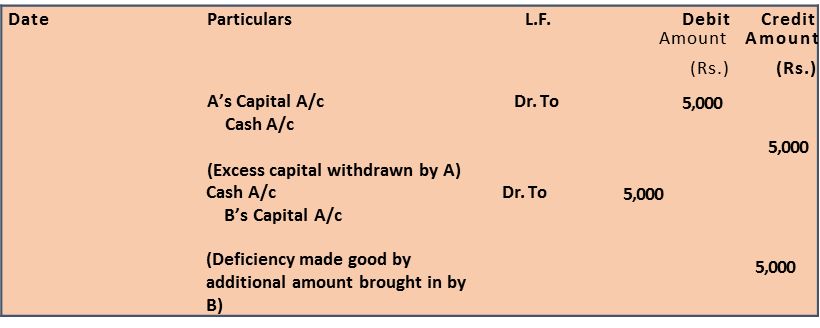

Sometimes, at the time of admission, the partners agree that their capitals should also be adjusted so as to be proportionate to their profit sharing ratio. In such a situation, if the capital of the new partner is given, the same can be used as a base for calculating the new capitals of the old partners. The capitals thus ascertained should be compared with their old capitals after all adjustments relating to goodwill reserves and revaluation of assets and liabilities, etc. have been made; and then the partner whose capital falls short, will bring in the necessary amount to cover the shortage and the partner who has a surplus, will withdraw the excess amount of capital. (See Revision 26)

Revision 26

A and B are partners sharing profits in the ratio of 2:1. C is admitted into the firm for 1/4 share of profits. C brings in Rs. 20,000 in respect of his capital. The capitals of old partners A and B, after all adjustments relating to goodwill, revaluation of assets and liabilities, etc., are Rs. 45,000 and Rs. 15,000 respectively. It is agreed that partners’ capitals should be according to the new profit sharing ratio.

Determine the new capitals of A and B and record the necessary journal entries assuming that the partner whose capital falls short, brings in the amount of deficiency and the partner who has an excess, withdraws the excess amount.

Solution

Calculation of new profit sharing ratio: Assuming the new partner C quires his share from A and B in their old profit sharing ratio, i.e 2:1.

C’s Share = ¼

Remaining Shares = 1- ¼ - ¾

A’s New Share = ¾ × 2/3 – 6/12

B’s New Share = ¾ × 1/5 – 3/12

C’s New Share = ¼ × 3/5 – 3/12

Thus, new profit sharing ratio between A,B and C is 6:3:3 or 2:1:1.

Required Capital of A and B

C’s capital (who has 1/4 share in profits) is Rs. 20,000. B’s new share in profits

1/4. Hence his capital will also be Rs. 20,000. A’s new share is 2/4 which is double of C’s share. Hence his capital will be Rs. 40,000.

Alternatively, based on C’s capital, the total capital of the firm works out at Rs. 80,000 (4/1 × Rs.20,000). Hence, based on their share in profits, the capital of A and B will be:

A’s capital = 2/4 of 80, 000 = Rs 40, 000

B’s capital = ¼ of 80, 000 = Rs 20,000

The capital of A and B after all adjustments have been made, are Rs. 45,000 and Rs. 15,000 respectively. Hence, A will withdraw Rs. 5,000 (Rs. 45,000– Rs.40,000) from the firm whereas B will contribute additional amount of Rs. 5,000 (Rs. 20,000–Rs.15,000). The journal entries will be :

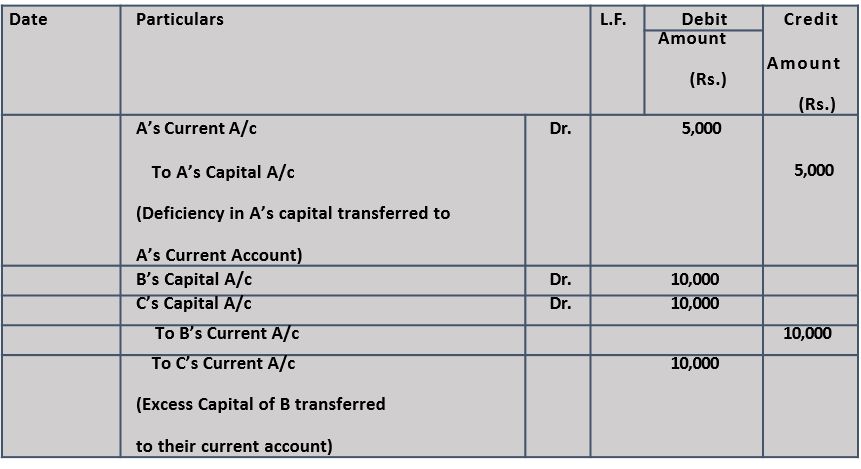

Sometimes, the total capital of the firm may clearly be specified and it is agreed that the capital of each partner should be proportionate to his share in profits. In such a situation each partner’s capital (including the new partner’s capital to be brought by him) is calculated on the basis of his share in profits. By bringing in additional amount or withdrawal of excess amount, the final capital of each partner can be brought up to the required level. It may be noted that subject to agreement among the partners, surplus or deficiency in each old partners’ capital accounts can also be taken care of simply by transfer to their respective current accounts. (See Revision 27)

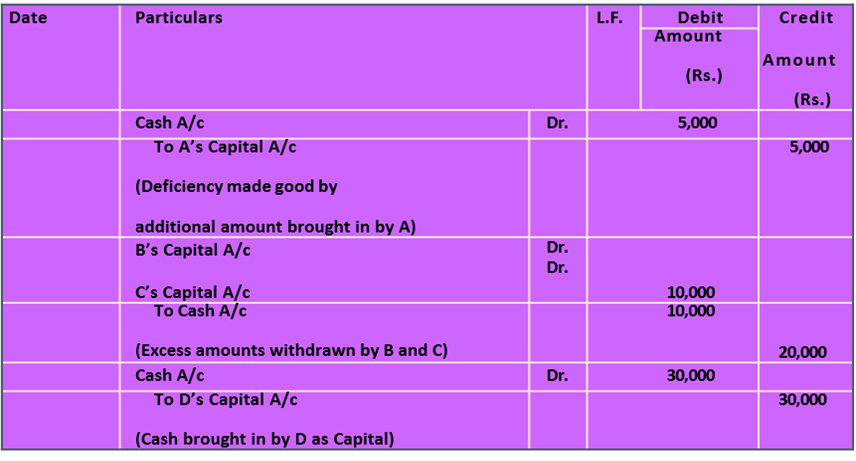

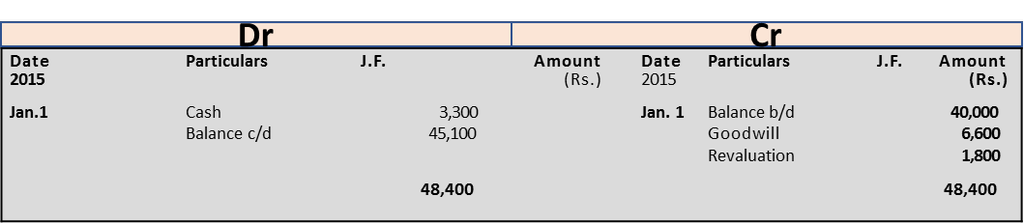

Revision 27

A, B and C are partners in a firm sharing profits the ratio of 3:2:1. D is admitted into the firm for 1/4 share in profits, which he gets as 1/8 from A and 1/8 from B. The total capital of the firm is agreed upon as Rs. 1,20,000 and D is to bring in cash equivalent to 1/4 of this amount as his capital. The capitals of other partners are also to be adjusted in the ratio of their respective shares in profits. The capitals of A, B and C after all adjustments are Rs. 40,000, Rs. 35,000 and Rs. 30,000 respectively. Calculate the new capitals of A,B and C, and record the necessary journal entries.

Solution

Calculation of new profit sharing ratio:

A = ½ - 1/8 = 3/8

B = 1/3 – 1/8 = 5/24

C will continue to get 1/6 as his share in the profits.

Thus, the new profit sharing ratio between A,B,C and D will be:

3/8 : 5/24 : 1/6 or 9/24 : 5/ 24 : 4/24 : 6/24 or 9 : 5 : 4 : 6

Required capitals of all partners:

A’s Capital = Rs. 1,20,000 = 9/24 = Rs 45, 000

B’s Capital = Rs. 1,20,000 × 5/24 = Rs 25, 000

C’s Capital = Rs. 1,20,000 × 4/24 = Rs 20, 000

D’s Capital = Rs. 1,20,000 × 6/24 = Rs 30, 000

Hence, A will bring in Rs. 5,000 (Rs. 45,000 – Rs. 40,000), B will withdraw

Rs. 10,000 (Rs. 35,000 – Rs. 25,000), C will withdraw Rs. 10,000 (Rs. 30,000– Rs, 20,000) and D will bring in Rs. 30,000. Alternatively, the current accounts can be opened and the amounts to be brought in or withdrawn by A, B and C will be transferred to their respective current accounts subject to the agreement among the partners. The journal entries in this regard will be recorded as follows:

Books of A, B, C and D Journal

Alternatively, for entries (2) and (3) above shall be

Books of A, B, C and D Journal

Revision 28

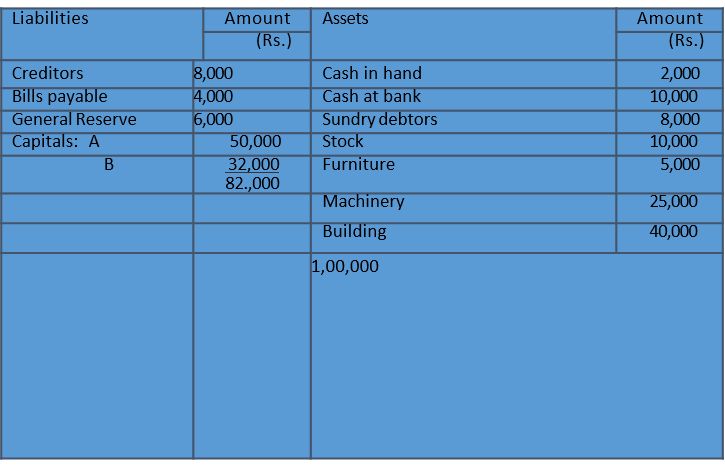

A and B are partners in a firm sharing profits in the ratio 2:1. C is admitted into the firm with 1/4 share in profits. He will bring in Rs. 30,000 as capital and capitals of A and B are to be adjusted in the profit sharing ratio. The Balance Sheet of A and B as on March 31, 2017 (before C’s admission) was as under:

Balance Sheet of A and B as at March 31,2017

Other terms of agreement are as under:

1. C will bring in Rs. 12,000 as his share of goodwill.

2. Building was valued at Rs. 45,000 and Machinery at Rs. 23,000.

3. A provision for bad debts is to be created @ 6% on debtors.

4. The capital accounts of A and B are to be adjusted by opening current accounts.

Record necessary journal entries, show necessary ledger accounts and prepare fund’s Balance Sheet after C’s admission.

Books of A, B and C Journal

Revaluation Account

Partners’ Capital Accounts

Partners’ Current Accounts

Balance Sheet of A, B and C as on March 31, 2017

Notes

Since nothing is given as to how C acquired his share from A and B. It is assumed that A

and B, between themselves continue to share the profit in the old ratio of 2:1.

C’s Share of Profits = ¼

Remaining Share = 1 – ¼ = ¾

A’s New Share = 2/3 of ¾ = 6/12 = ½

B’s New Share = 1/3 of ¾ = 3/12 = ¼

Thus, new profit sharing ratio between A, B and C is 2:1:1

New Capitals of A and B

C’s capital is Rs 30,000 and his share of profits is 1/4. Based on C’s capital, the total capital of the firm will work out at Rs 1,20,000 (4/1 × 30,000) and the respective capitals of A and B will be as follows :

A’s Capital = 2/4 of 1, 20, 000 = Rs 60, 000

B’s Capital = ¼ of 1, 20, 000 = Rs 30, 000

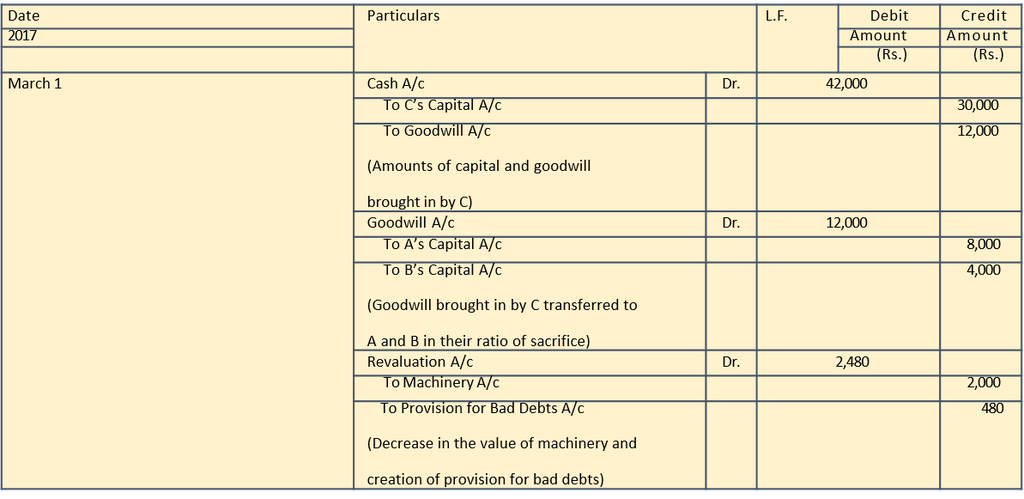

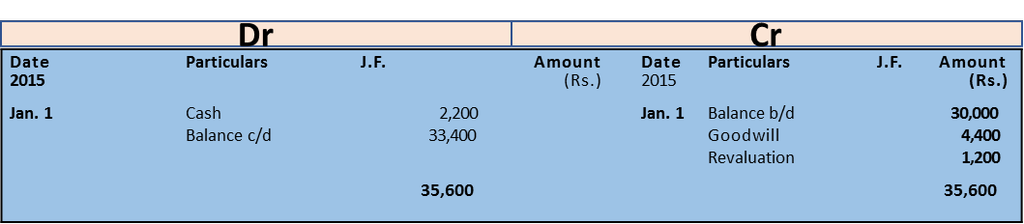

Revision 29

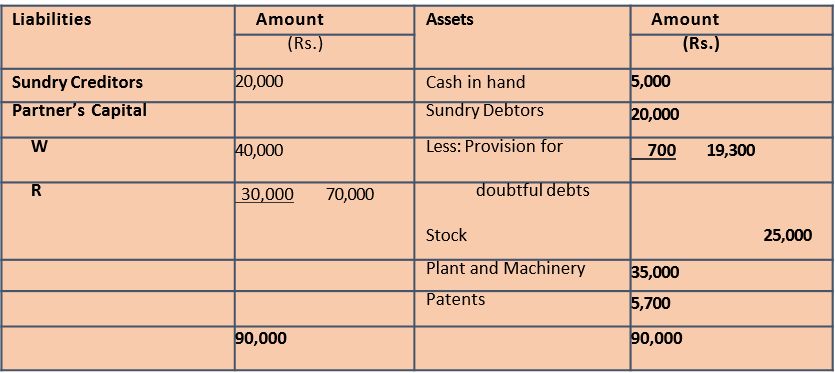

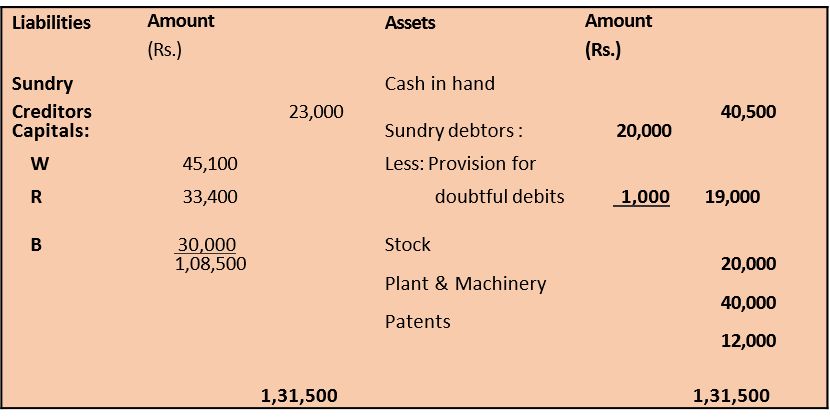

The Balance Sheet of W and R who shared profits in the ratio of 3 : 2 was as follows on January. 01, 2015.

Balance Sheet of W and R as on Jan. 01, 2015

On this date B was admitted as a partner on the following conditions:

1. He was to get 4/15 share of profit.

2. He had to bring in Rs 30,000 as his capital.

3. He would pay cash for goodwill which would be based on 2 ½ years purchase of the profits of the past four years.

4. W and R would withdraw half the amount of goodwill premium brought by B.

5. The assets would be revalued as: Sundry Debtors at book value less a provision of 5%; Stock at Rs 20,000; Plant and Machinery at Rs 40,000; and Patents at Rs 12,000.

6. Liabilities were valued at Rs 23,000, one bill for goods purchased having been omitted from books.

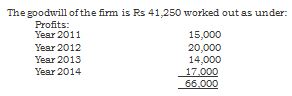

7. Profit for the past four years were :

2011 15,000 2013 14,000

2012 20,000 2014 17,000

Give necessary journal entries and ledger accounts to record the above, and prepare the Balance Sheet after B’s admission.

Solution

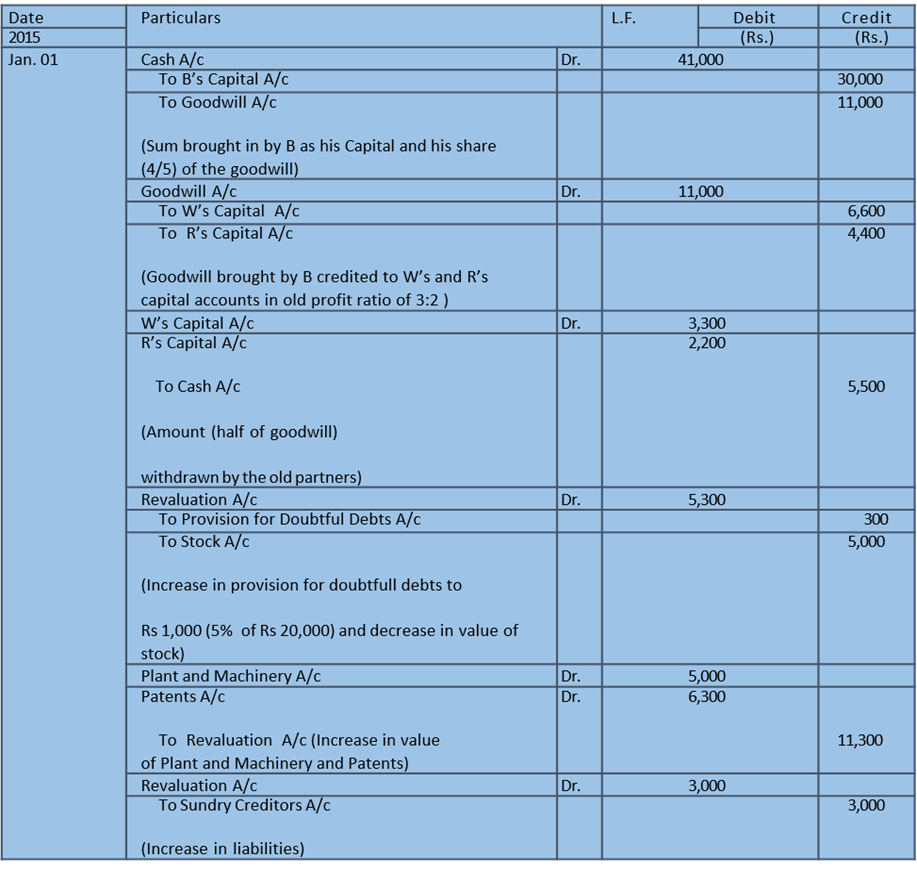

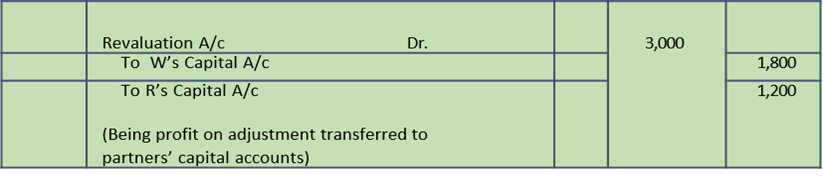

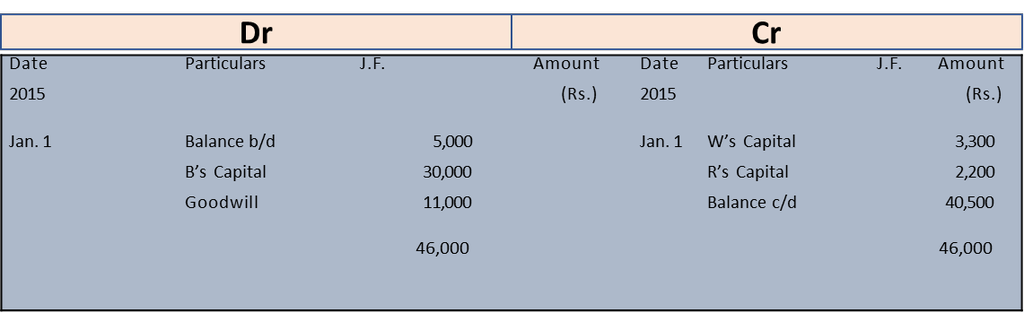

Average Profits = Rs 66, 000/4 = Rs 16, 500

Goodwill at 2 ½ Years purchase = Rs .16,500 × 5/2 = Rs 41, 250

B’s share of goodwill = Rs. 41,250 × 4/15 = Rs 11, 000

Cash Account

B’s Capital Account

W’s Capital Account

R’s Capital Account

Balance Sheet of W, R and B as on January 01, 2015

The new profit sharing ratio will be:

W = (1- 4/15 ) × 3/5 = 11/15 × 3/5 = 33/75

R = ( 1 – 4/15 ) × 2/5 = 11/15 × 2/5 = 22/ 75

B = 4/15 = 20/75

The new ratio is 33 : 22 : 20.

Change in Profit Sharing Ratio among the Existing Partners

Sometimes, the partners of a firm decide to change their existing profit sharing ratio without any admission or retirement of a partner. This results in a gain of additional share in future profits of the firm for some partners while a loss of a part thereof for other partners. For example, A, B and C are partners in a firm

sharing profits in the ratios of 8:5:3 It is felt that A will no more be able to actively participate in the affairs of the firm. Hence, with effect from April 1, 2007, they decided that, in future they will share the profits in the ratio of 5:6:5. This result in A losing 3/16 (8/16 – 5/16) share in profits while B and C gaining 1/16 (6/16 – 5/16) and 2/16 (5/16 – 3/16). In such a situation, the loss and gain in the value of goodwill (if any) will have to be adjusted. This is done by crediting sacrificing partner's and debiting gaining partner's with appropriate amounts, as is explained earlier in the context of the admission of a new partners.

Any change, in the profit sharing ratio, like admission of partner, may also involve adjustments in respect of revaluation of assets and liabilities, transfer of accumulated profit and losses to partners' capital accounts in the old profit sharing ratio and adjustment of partners' capitals, if specified, so as to make them proportionate to the new profit sharing ratio. All this is done in the same way as in case of admission of a partner.

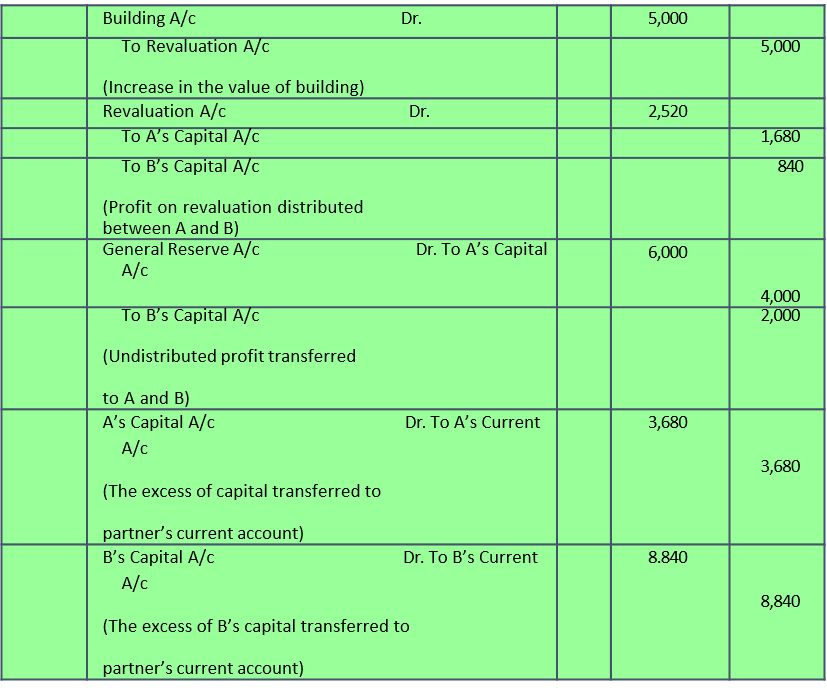

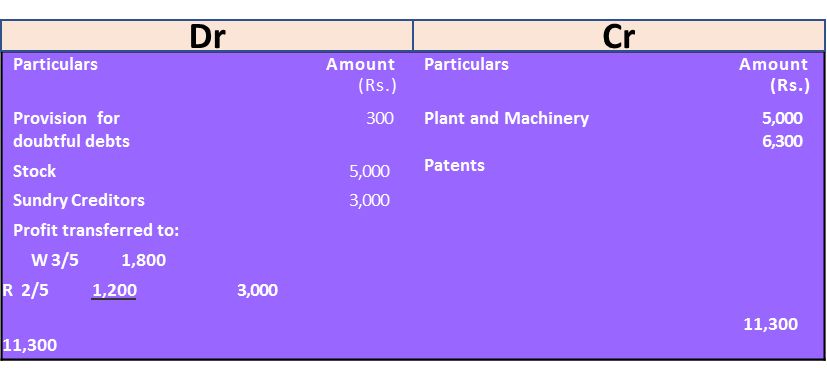

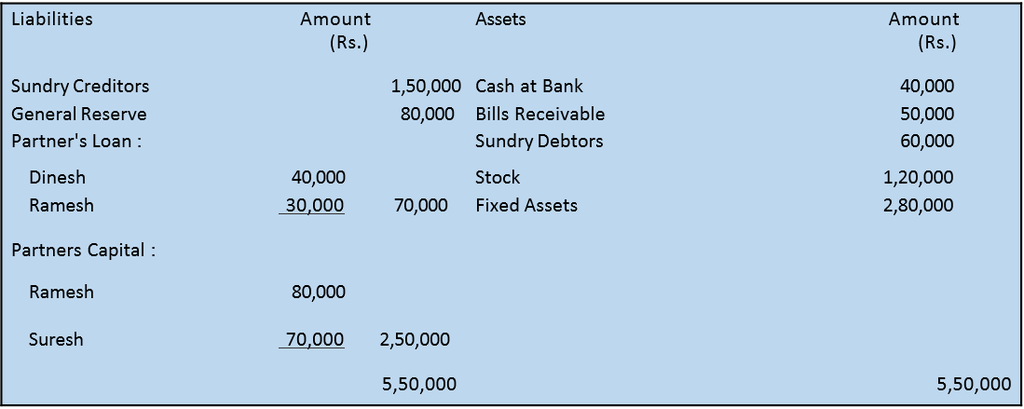

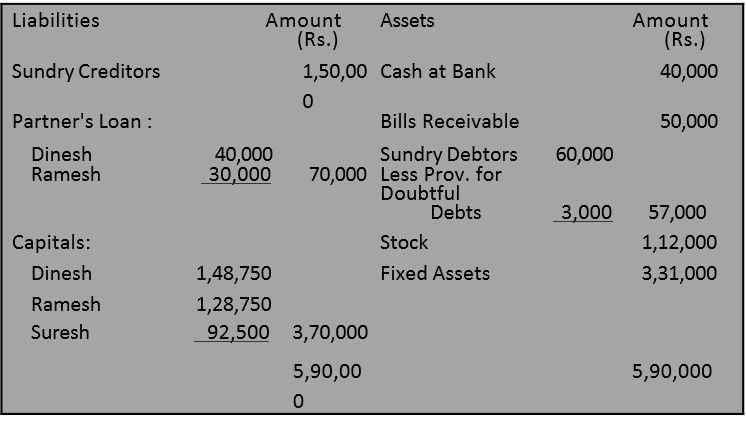

Revision 30

Dinesh, Ramesh and Suresh are partners in a firm sharing profits and losses in the ratio of 3:3:2. They decided to share the profits equally w.e.f. April 1, 2015. Their Balance Sheet as on March 31, 2016 was as follows :

It was also decide that :

- The fixed assets should be valued at Rs. 3,31,000.

- A provisions of 5% on sundry debtors be made doubtful debts.

- The goodwill of the firm at this date be valued at

years purchase of the average net profits of last, five years which were Rs. 14,000; Rs. 17,000; Rs. 20,000; Rs. 22,000 and Rs. 27,000 respectively.

years purchase of the average net profits of last, five years which were Rs. 14,000; Rs. 17,000; Rs. 20,000; Rs. 22,000 and Rs. 27,000 respectively. - The value of stock be reduced to Rs. 1,12,000.

- Goodwill was not to appear in the books. Pass the necessary journal entries and prepare the revised Balance sheet of the firm.

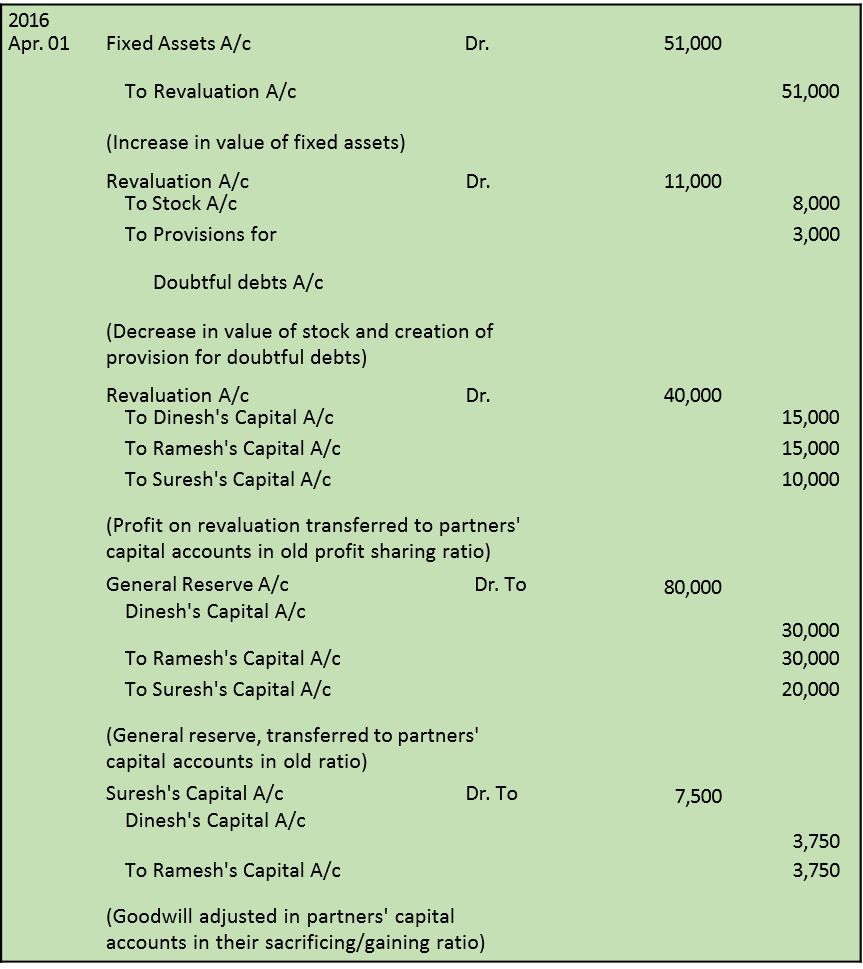

Solution

Books of Dinesh, Ramesh and Suresh Journal

Working Notes:

1. Gain or sacrifice of partners

2. Goodwill

Total Profits : Rs. 14,000 + Rs. 17,000 + Rs. 20,000 + Rs. 22,000 + Rs. 27,000

= Rs. 1,00,000

Average Profits = Rs. 1,00,000/5 = Rs. 20,000

Goodwill = Rs. 20,000 × ![]() = Rs 90, 000

= Rs 90, 000

Suresh in expected to bring in Rs. 7,500

as he gain 2/24 shares in profits.

Dinesh in expected to receive Rs. 3,750

as he sacrifices 1/24 share in profits

Ramesh is expected to receive Rs. 3,750

as he sacrifices 1/24 share in profits

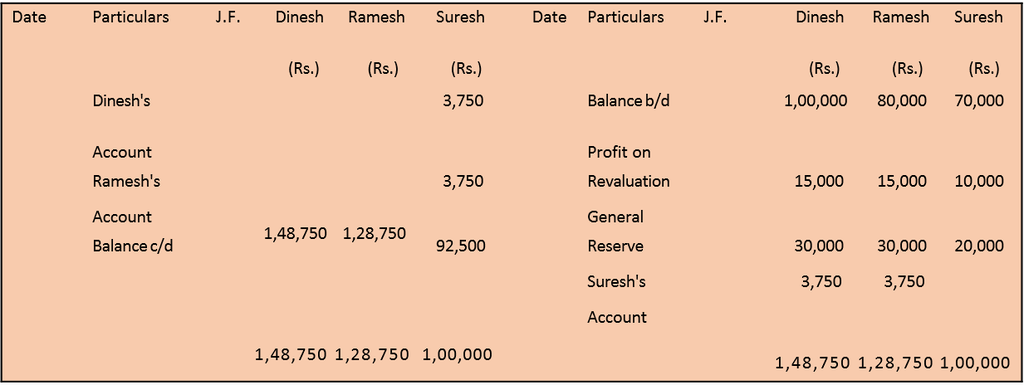

3. capital Accounts

![]() Balance Sheet as on April 01, 2015

Balance Sheet as on April 01, 2015

Summary

1. Matters requiring adjustments at the time of admission of a partner: Various matters which need adjustments in the books of firm at the time of admission of a new partner are : goodwill, revaluation of assets and liabilities, reserves and other accumulated profits and losses and the capitals of the old partners’ (if agreed).