Vision classes

Vision classes

- Books Name

- Vision classes Accountancy Book

- Publication

- Vision classes

- Course

- CBSE Class 11

- Subject

- Accountancy

CHAPTER -3

RECORDING OF TRANSACTIONS

BUSINESS TRANSACTION AND SOURCE DOCUMENTS

Meaning of Source document:

Business transactions are recorded in the books of accounts on the basis of some written evidence called source document.

Types of sources of documents:

1. Cash memo-when the trader sells and purchase goods for cash he gives and received cash memo.

2. Invoice and bill- when a trader sells goods on credit he prepares a sale invoice which contain of all detail of transaction.

3. Debit note-when a business return goods to supplier business prepare a debit not and send to the supplier with the return goods.

4. Credit note- when goods are received back from a customer a credit not send to him that the customer account has been credited in our books.

5. Pay in slip-this is a form available from a bank and it used to deposit money in the bank.

Meaning of Voucher

Documentary evidence in support of the transaction is known as voucher.

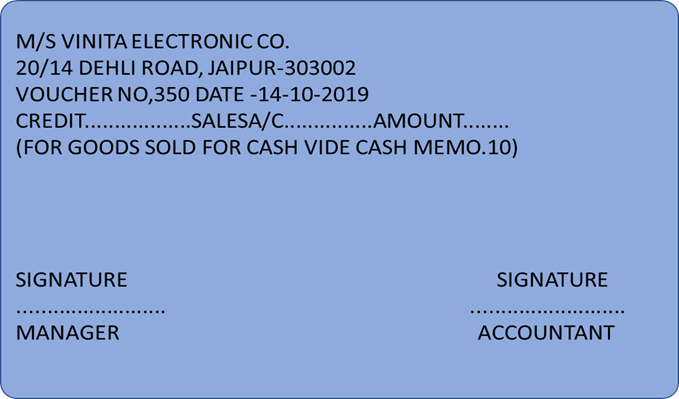

Type of voucher:

1. Cash voucher- Cash voucher is prepared for cash transaction i.e., cash receipt and cash payments. These are two type ;

(i) debit voucher-its prepared for cash payment

(ii) Credit voucher- its prepared for cash receipts.

2. Non –cash voucher-these vouchers are prepared for credit transactions like credit sale and purchase, depreciation, bad debts.

FORMATE OF CREDIT VOUCHER