Vision classes

Vision classes

- Books Name

- Vision classes Accountancy Book

- Publication

- Vision classes

- Course

- CBSE Class 11

- Subject

- Accountancy

Financial Statements

Various users have diverse informational requirements. Instead of generating particular information useful for specific users, the business prepares a set of financial statements, which in general satisfies the informational needs of the users.

The basic objectives of preparing financial statements are :

(a) To present a true and fair view of the financial performance of the business

(b) To present a true and fair view of the financial position of the business

For this purpose, the firm usually prepares the following financial statements:

1. Trading and Profit and Loss Account

2. Balance Sheet

Trading and Profit and Loss account, also known as Income statement, shows the financial performance in the form of profit earned or loss sustained by the business. Balance Sheet shows financial position in the form of assets, liabilities and capital. These are prepared on the basis of trial balance and additional information, if any.

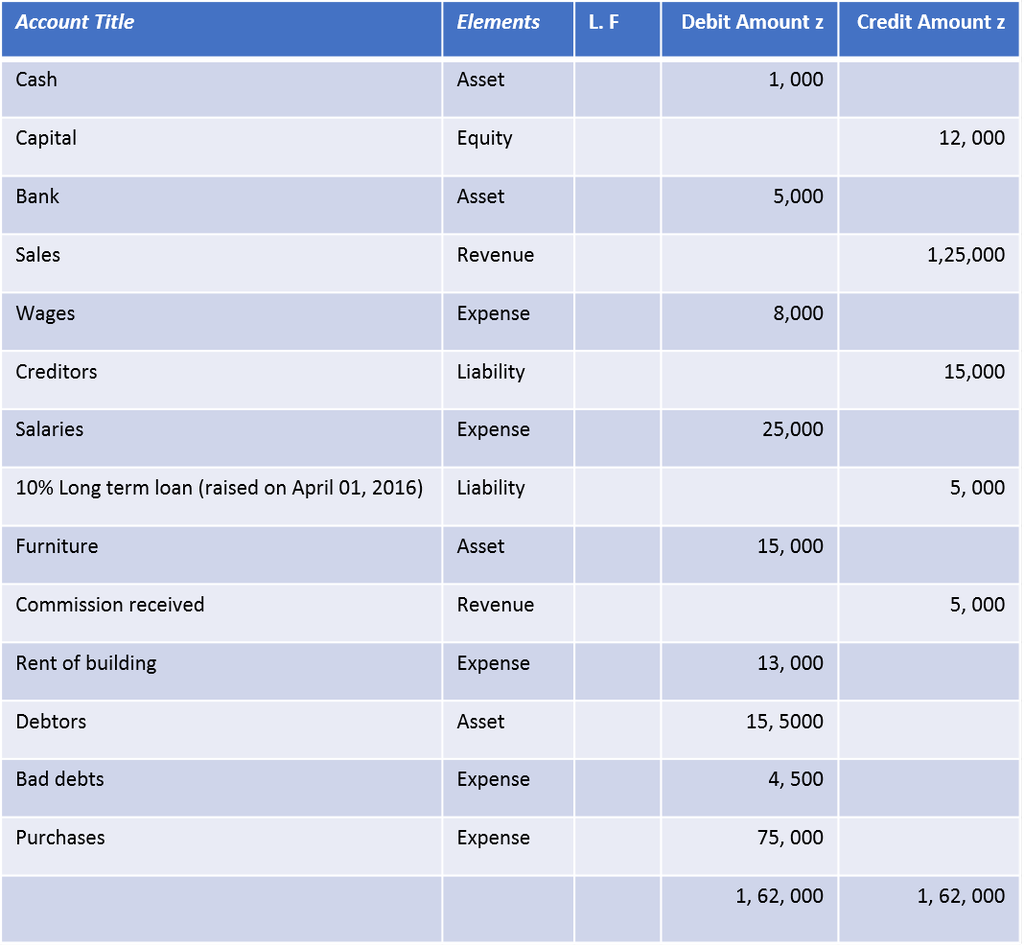

Example 1

Observe the following trial balance and signify correctly the various elements of accounts and you will notice that the debit balances represent either assets or expenses/ losses and the credit balance represent either equity/liabilities or revenue/gains.

Trial Balance as on March 31, 2017

The balance sheet and profit and loss account are now called position statement and statement of profit and loss in the company's financial statements. Analysis of

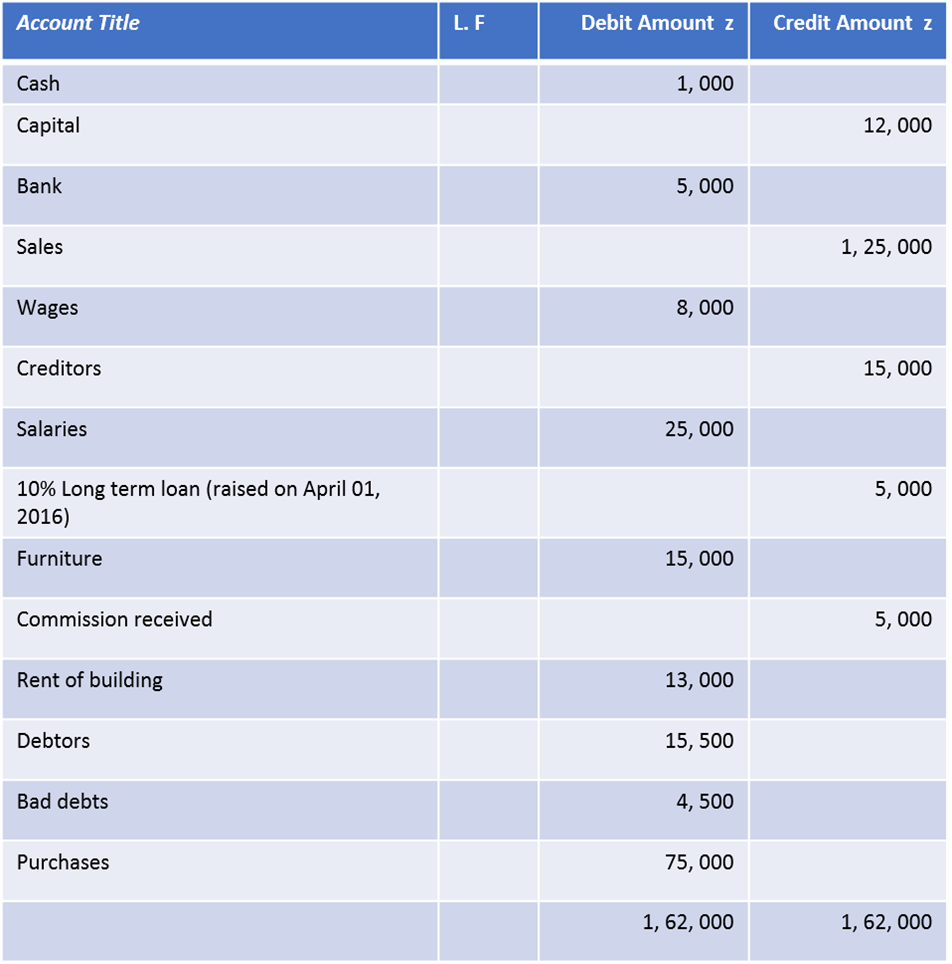

Trial Balance as on March 31, 2017