SS MUKHI

SS MUKHI

- Books Name

- CA Shivali kedia Accountancy Book

- Publication

- CA Shivali kedia

- Course

- CBSE Class 11

- Subject

- Accountancy

Basic Terms of Accounting

Follow the Story

17-year-old Harsh

Harsh is a commerce student in class 12th who is very confident and smart and wants to run a business like his father.

Although, he was average in his studies but had a smart business mind.

He wanted to start a business of opening a small café in his locality after his school.

He discussed this idea with his father.

His father wanted him to open this business but only if he pursues college along side

His father liked his business Idea and Gave him Rs.10 lacs to start the cafe

Exercise for students:

List down how will Harsh spend this 10 Lac Rupees to start his café.

1)_____________

2)_____________

3)_____________

4)_____________

5)_____________

6)_____________

7)____________

Starting the cafe

1) Place to run business (either Buy or Rent)

2) Hire a Cook and Staff (Salary)

•3)Raw materials (Breads, Eggs, vegetables)

•4) Griller, Deep freezer

•5) Registration and other expenses, etc

How many did you get right?

Accountancy is very closely related to practical and day-to-day life.

Let us understand the basic terms

Capital

Money which is invested by the Owner in starting the business is called capital.

Remember, when Harsh needed 10 Lacs rupees, his father gave him this money for free. Its Harsh’s (owners) money.

Harsh started his café with RsLacs of his own money, called capital which he does have to pay back to his father.

Assets

•Assets are resources which are owned by “Business” which has some value.

•In Harsh Story What are the items whchhasrh purchased (Which has a value)

•Deep freeze, Griller, oven, raw materials like cheese, bread, spices, etc

•If Harsh wants to see any of these, at any point, he will get some value.

•Assets are further classified into 2 broad categories

Assets Classification

Non Current Asset

•Some assets have a life of more than one year.

•Furniture, Air condition, Car, Truck, Plant and Machinery

•Land, Building, Long term investments etc

•We will talk more on this later

Current Assets

•On the other hand, some assets have a short shelf life

•Inventory (Stock), Debtors, Cash, Bank, Current investments

Liabilities

•Let us assume, that Harsh, spent all the 1Rs,10,00,000 and required 5 lacs more to run the business.

•He went to his father who refused to give him more money for the business

Harsh’s father asked him to reach out to the Bank.

Because Banks gives us loan repayable after a certain point.

Harsh will have to pay Interest on this loan

•Harsh gets 5 lac rupees from bank as Loan loan repayable in 5 years with 10% interest p.a

Although Harsh is happy that he got to money to start his business.

Please remember that he will have to pay back the bank this loan or bank will forfeit his assets.

This is a liability of Harsh’s Café, an obligation which needs to be paid in the future.

Liabilities classification

Non CurrentLiabilites

Bank Loans (Repayabale after1 year)

Other Long term loans

Current Liabilites

•Bank Loans (Repayable in less than 1 year)

•Creditors

•Bills Payable

Loan and capital ?

Capital

•Money which is invested by the Owner in starting the business is called capital.

•Example: Money Harsh received from his father which he doesn’t need to pay be to his father.

Loan

•Money invested in the business, which has to be repaid to a third party, after a point of time with interest is called Loan

•Example: Money Harsh received from Bank which has to be paud back after 5 years with interest.

Harsh successfully Opens his Café

Lets move ahead in our story!!

Sales

The café sells its first burger i.e. makes it first “SALE”

Sales are total Revenues from good and services sold to consumers in a given year.

Sales can be made in cash, called cash sales.

Sales can also be made on credit called credit sales

It’s the owners decision and industry standards on cash and credit sale depending on the product and service.

Sales and revenue

Sales

•Sales are total Revenues from good and services sold to consumers in a given year.

•Eg: Selling of Burgers and sandwiches in the café and taking service charge from customers for the services provided by the café

Revenue/Income

•Revenue is the sum total of Sales and other income

•Other Income includes income earned by business from sources, other than its “main operations”

•Example: Harsh’s café sells and old AC foe 15000. This 15000 is not sales but is “other income “for the café

Now the café became profitable. Lets understand how

Expenses

For generating sales, all the cost incurred by the business is called expenses.

In Harsh’s café, think of the expenses incurred to sell that one burger:

1)Salary to cook and staff2)Electricity expenses

3)Purchase of raw material

There are a lot of other expenses which I leave to the students to think and list.

Expenses and Expenditure

Expenses

•Costs incurred by business for generating sales. •It’s recurring in nature.

•Wages, salaries, electricity bill, water bills, repairs, purchases etc

•Expenses are subtracted from sales to calculate profits for the year.

Expenses are a yearly concept, that is, the benefit of this expense is exhausted within a year

Expenditure

•Cost incurred by business for some benefit, generating sales or acquiring property for business

•Wages, salaries, purchases, land purchased, revenue purchased

•The benefit of expenditure is not exhausted in one year.

If café purchases delivery scooter, the scooter will run for more than one year. The benefit accrues for more than one year unlike expenses

Profit = Revenue – Related expenses

•Related expenses means expenses reated to business. Eg: Salary, wages, etc.

•Unrelated expenses are expenses which are not related to business of café.

For the café, unrelated expenses eg. Repairs made for colony gate where café is situated

Profit and Gain

Profit

•Excess of revenue over related expenses is called Profit.

•If selling price of burger is Rs 500 and total cost of making that burger is Rs 200. Then profit will be Rs. 300.

Gain

•Gains are profit arising from a transaction which is not the main operations of the business

•For example: :Harsh’s café sells and old AC and made a profit of 5000. This 5000 will not be called proft but is gain to the business the café

Loss

The excess of expenses of a given period (Financial year) , over Income (Revenue) of a given period is called Loss.

In our Café,

1)let’s say Total Revenue for the year 2022-2023 is Rs, 12,00,000

2)Expenses of salaries, purchases of raw materials, bills is 14,00,000

3)So the the year 2022-2023, Harsh’s café made a loss of (2,00,000)

Inventory (Stock/Goods)

Inventory are goods used in production process, as well as, finished goods produced thereafter.

Inventory also includes good lying with the trading concerns where no production process is carried on.

In Harsh’s Café, the café used raw materials (eg: Vegetables, milk, bakery products) , to produced finished goods Eg: (Pizza, Sandwiches), etc. All these will be considered as Inventory

Goods and Stock

•Goods are the products which are being purchased and sold by the business. Goods and Inventory is often used interchangeably.

•Please note, there are various products which the business purchases in its day to day working. Such items are not categorised as goods, for example in Harsh café, stationary (like bill rolls, pens, stapler) will be purchased. These will not be categorised as goods.

•Inventory are goods used in production process, as well as, finished goods produced thereafter.

•Inventory also includes good lying with the trading concerns where no production process is carried on.

Drawings

No, Not what you are thinking!

These are not doodling or drawing, literally.

When the owner withdraws money or any other asset from business for his “ personal needs” is called Drawings.

In Harsh’s example,

Lets say, after making the business protitable, now he wants to take a vacation with his family to Paris. He withdraws Rs, 5,00,000 from the business Bank Account. These Rs, 5 lacs will be considered drawings in the accounts of the business.

Purchases

•Purchases are expense incurred by the owner on purchase of inventory, on cash or credit.

Note for Students: Don’t think about purchases you would make as an individual

•Think from the company's or proprietor’s viewpoint. It has to be a purchase the business

•In Harsh’s café, if you purchase a burger, it’s a Sale for the business.

•But the purchases made by the café to make that one burger will be a Purchase for the business.

Discount

•Consider this example,

•You are a friend of Harsh and you visit his café to have dinner with your family. You bill comes out to Rs. 2,500.

•Harsh Gives you a discount of 20% and you end up paying only Rs. 2,000.

•Harsh gave you a discount of Rs,500. It is a loss to the business.

•Discount is the reduction on the sale price of the sales.

•In Accounting Discount is of two kinds. Lets discuss this on the next slide

Trade Discount & Discount (Cash Discount

Trade Discount

•This discount is given when a customer places an order in bulk.

•Higher Sales orders are always preferred by sellers and businesses. To encourage that, Trade discount is given to the customer on bulk orders

Cash Discount

•Usually in businesses, Sale/purchase happen on a Credit basis, from buyers and sellers.

•If a customer is willing to make the puchase in Cash, they are given a discount. Because cash is a preferred mode of payment.

•Cash is dear to the business.

Debtors (Credit Sales)

•When a business makes a sale and agrees to the terms of receiving the sales value, at some future date from the customer, the customer becomes debtor of the company.

If a Harsh’s café sells a big order of Rs.10,000 to a customer (Mr. A) who agrees to clear the bill in one month’s time. Mr. A becomes the debtor to the company.

Creditor (Credit Purchases)

•When a business purchases goods from a seller, say Mr. X and agrees to pay Mr. X the money at a future date. Mr. X becomes a creditor to the business.

•It becomes a liability or obligation for the business to pa Mr. X at a future date.

•In our example:

•If Harsh’s café purchases bread on credit from the bakery owner and pay on later date (say end of every month).

•Then the Bakery owner will be accounted as Creditor in the books of harsh’s case Business.

Business Entity

Harsh Opened a Café and named it “Harsh’s Café”. He registered his business are a sole proprietorship (You will learn about this in class 11 business studies).

After he got his form registered, Harsh and Harsh’s café as 2 different persons in the eyes of law.

As soon as the owner registers the business, a new person is born in the eyes of the law, different from its owner.

Transaction

Transaction means an event or activity where one party is a receiver and other is a giver. It can be anything, like paying electricity bills, purchase of raw materials, making sales, etc

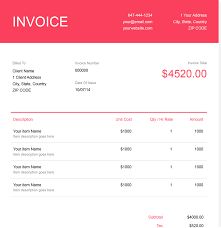

Voucher

Voucher is a evidence of the transaction in the court of law. Please look at the sales voucher below: