Vision classes

Vision classes

- Books Name

- Vision classes Accountancy Book

- Publication

- Vision classes

- Course

- CBSE Class 12

- Subject

- Accountancy

Income and Expenditure Account

It is the summary of income and expenditure for the accounting year. It is just like a profit and loss account prepared on accrual basis in case of the business organisations. It includes only revenue items and the balance at the end represents surplus or deficit. The Income and Expenditure Account serves the same purpose as the profit and loss account of a business organisation does. All the revenue items relating to the current period are shown in this account, the expenses and losses on the expenditure side and incomes and gains on the income side of the account. It shows the net operating result in the form of surplus (i.e. excess of income over expenditure) or deficit (i.e. excess of expenditure over income), which is transferred to the capital fund shown in the balance sheet.

The Income and Expenditure Account is prepared on accrual basis with the help of Receipts and Payments Account along with additional information regarding outstanding and prepaid expenses and depreciation etc. Hence, many items appearing in the Receipts and Payments need to be adjusted. For example, as shown in Example 1, (Page No. 10) subscription amount of Rs.2, 65,000 received during the year 2014-15 appearing on the receipts side of the Receipt and Payment Account includes receipts for the periods other than the current period. But the subscription amount of Rs. 2,25,000 pertaining to the current year only will be shown as income in Income and Expenditure Account for the year 2014-15.

Steps in the Preparation of Income and Expenditure Account

Following steps may be helpful in preparing an Income and Expenditure Account from a given Receipt and Payment Account:

1. Persue the Receipt and Payment Account thoroughly.

2. Exclude the opening and closing balances of cash and bank as they are not an income.

3. Exclude the capital receipts and capital payments as these are to be shown in the Balance Sheet.

4. Consider only the revenue receipts to be shown on the income side of Income and Expenditure Account. Some of these need to be adjusted by excluding the amounts relating to the preceding and the succeeding periods and including the amounts relating to the current year not yet received.

5. Take the revenue expenses to the expenditure side of the Income and Expenditure Account with due adjustments as per the additional information provided relating to the amounts received in advance and those not yet received.

6. Consider the following items not appearing in the Receipt and Payment Account that need to be taken into account for determining the surplus/ deficit for the current year :

a. Depreciation of fixed assets.

b. Provision for doubtful debts, if required.

c. Profit or loss on sale of fixed assets.

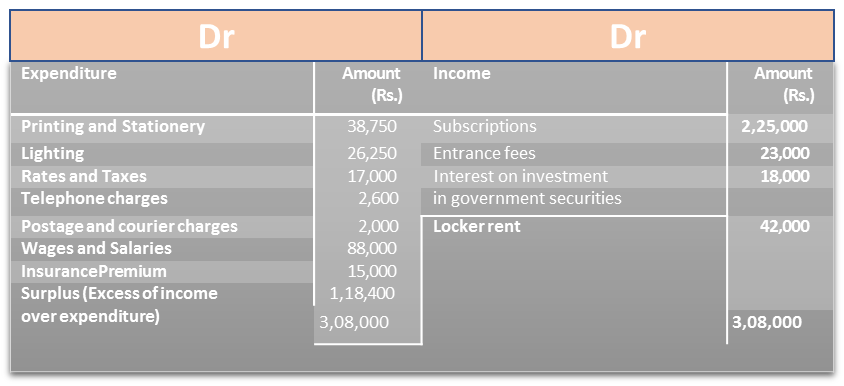

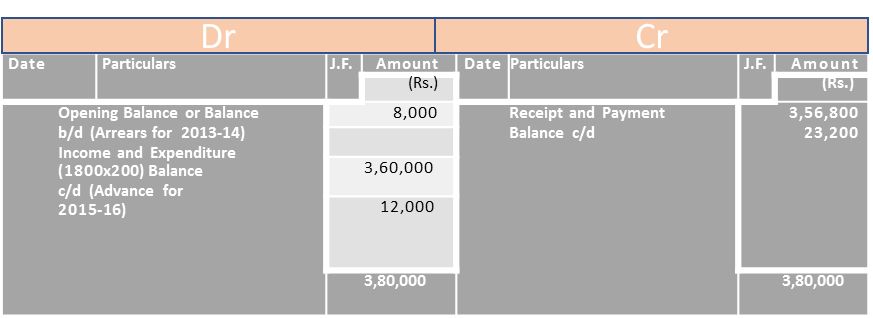

Now you will observe how the income and expenditure account is prepared from the receipts and payments account given in example 1, on page 10.

Income and Expenditure Account for the year ending on March 31, 2015

Note that-

- Opening and closing cash/bank balances have been excluded.

- Payment for purchase of Government securities being capital expenditure has been excluded.

- Amount of subscriptions received for the year 2013-14 and 2015-16 have been excluded.

- Life membership fee is an item of capital receipt and so excluded.

- Donation for building is a receipt for a specific purpose and so excluded.

Revision 2

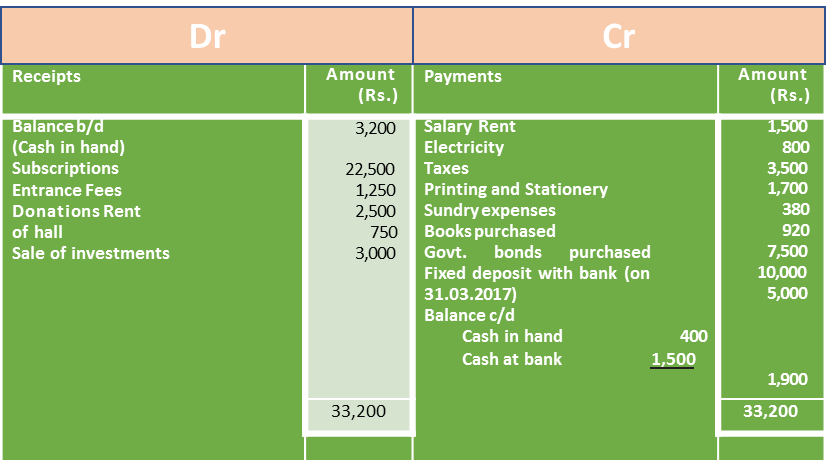

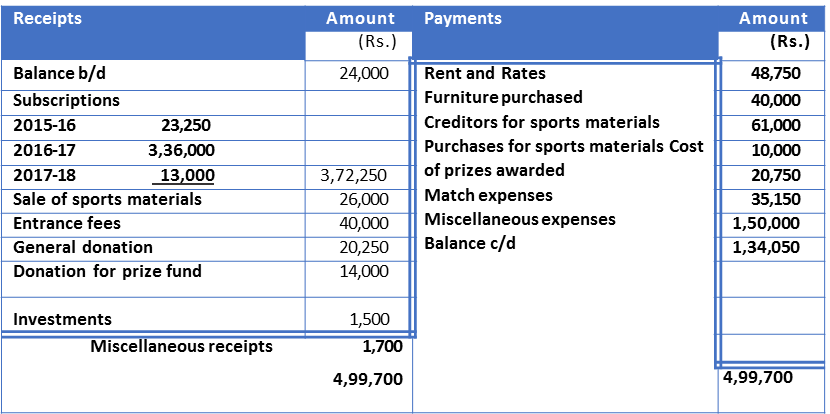

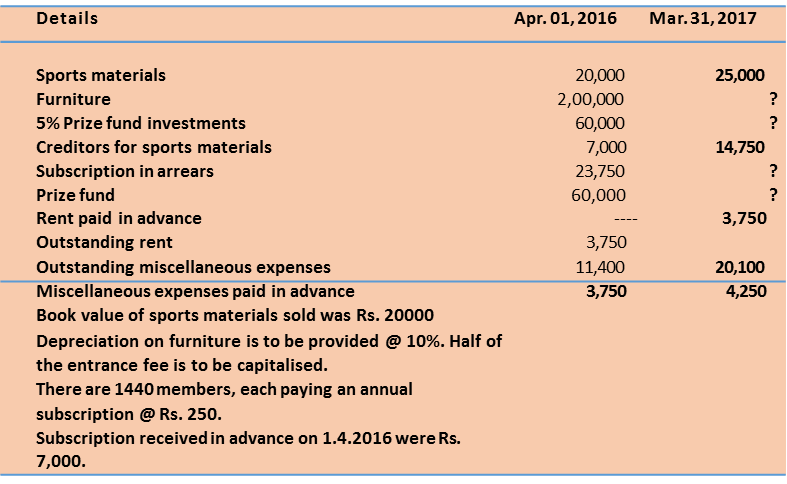

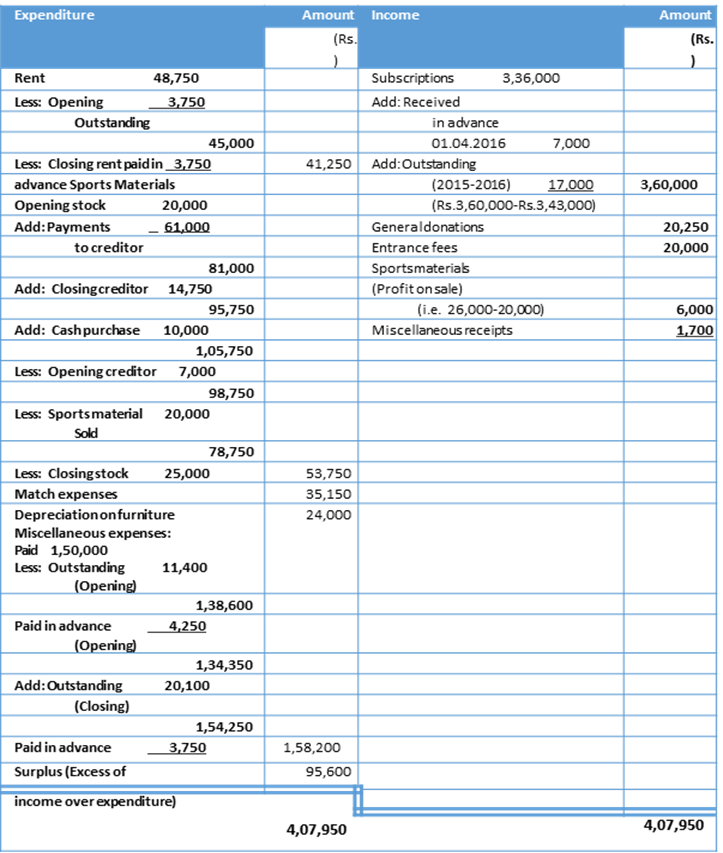

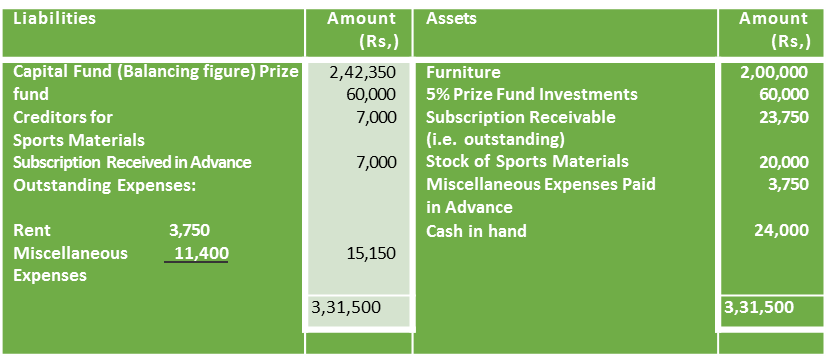

From the Receipt and Payment Account given below, prepare the Income and Expenditure Account of Clean Delhi Club for the year ended March 31, 2017.

Receipt and Payment Account for the year ending March 31, 2017

Solution

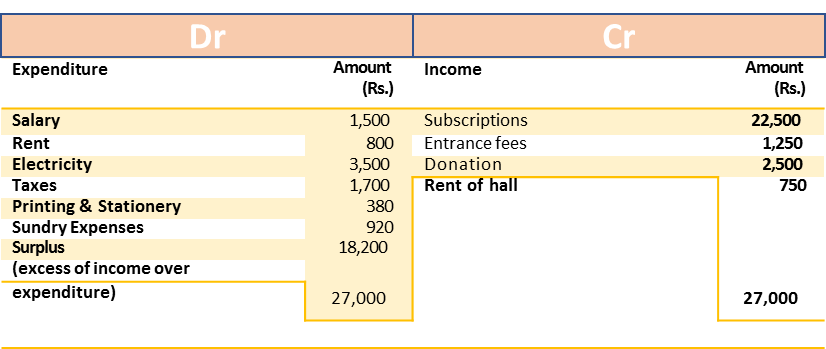

Books of Clean Delhi Club

Income and Expenditure Account for the year ending March 31, 2017

Revision3

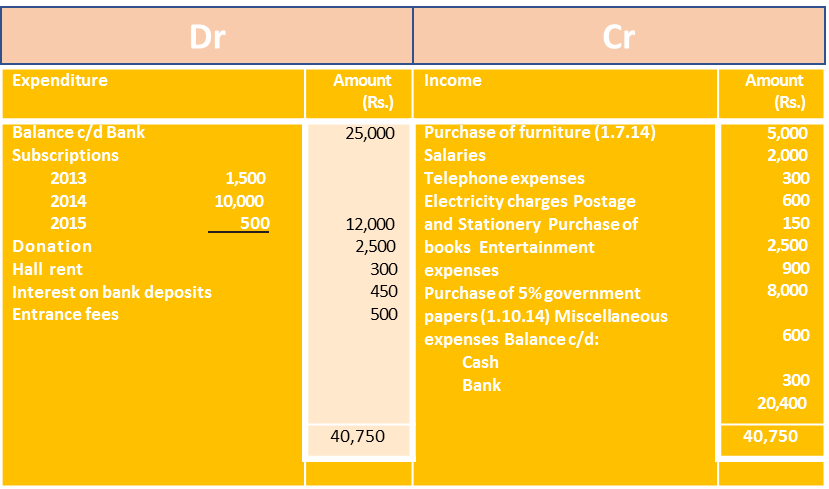

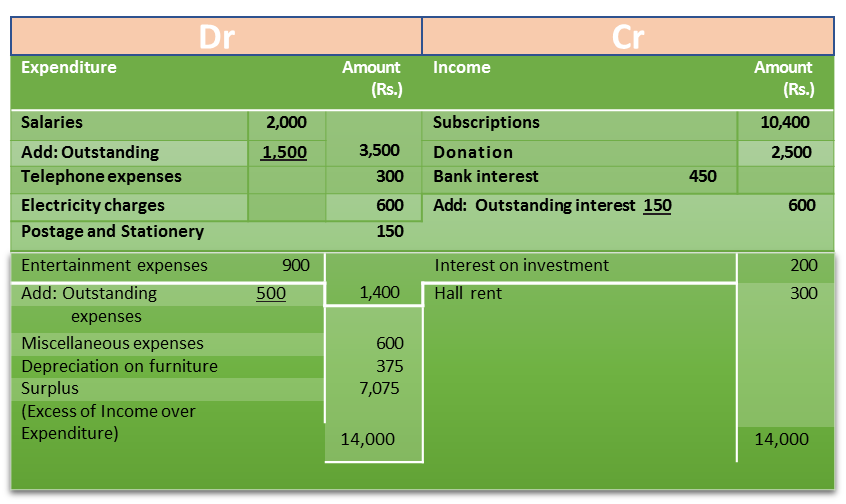

From the following Receipt and Payment Account for the year ending March 31, 2015 of Negi's Club, prepare Income and Expenditure Account for the same period:

Receipt and Payment Account for the year ending March 31, 2015

The following additional information is available:

- Salaries outstanding – Rs. 1,500;

- Entertainment expenses outstanding – Rs. 500;

- Bank interest receivable – Rs. 150;

- Subscriptions accrued – Rs. 400;

- 50 per cent of entrance fees is to be capitalised;

- Furniture is to be depreciated at 10 per cent per annum.

Solution

Books of Negi's Club

Income and Expenditure Account for the year ending 31.3.2015

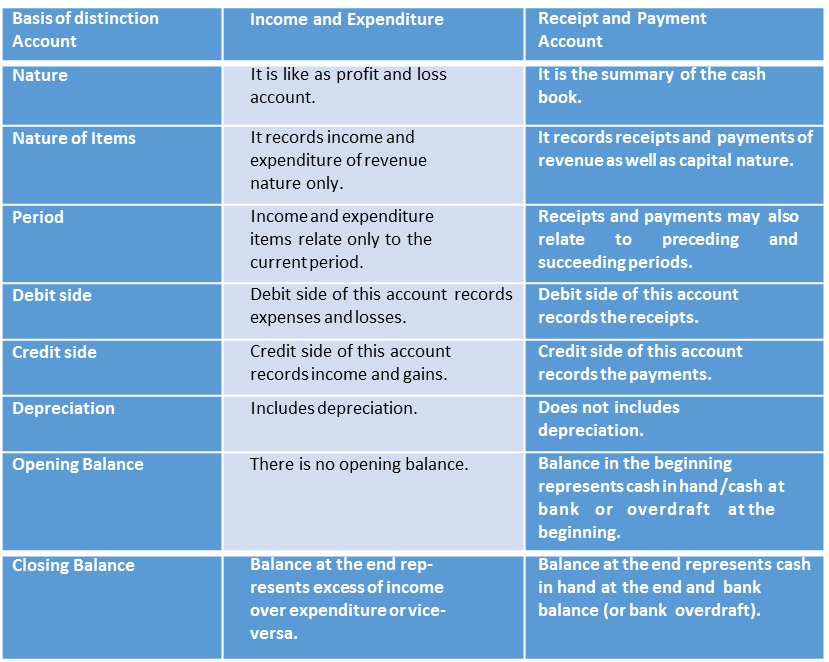

Distinction between Income and Expenditure Account and Receipt and Payment Account

Based upon discussion made in regard to the Receipts and Payments Account and the Income and Expenditure Account we make the distinction between Income and Expenditure Account and Receipts and Payments Account in the tabular form:

Balance Sheet

‘Not-for-Profit’ Organisations prepare Balance Sheet for ascertaining the financial position of the organisation. The preparation of their Balance Sheet is on the same pattern as that of the business entities. It shows assets and liabilities as at the end of the year. Assets are shown on the right hand side and the liabilities on the left hand side. However, there will be a Capital Fund or General Fund in place of the Capital and the surplus or deficit as per Income and Expenditure Account which is either added to/deducted from the capital fund, as the case may be. It is also a common practice to add some of the capitalised items like legacies, entrance fees and life membership fees directly in the capital fund.

Besides the Capital or General Fund, there may be other funds created for specific purposes or to meet the requirements of the contributors/donors such as building fund, sports fund, etc. Such funds are shown separately in the liabilities side of the balance sheet.

Some times it becomes necessary to prepare Balance Sheet as at the beginning of the year in order to find out the opening balance of the capital/general fund.

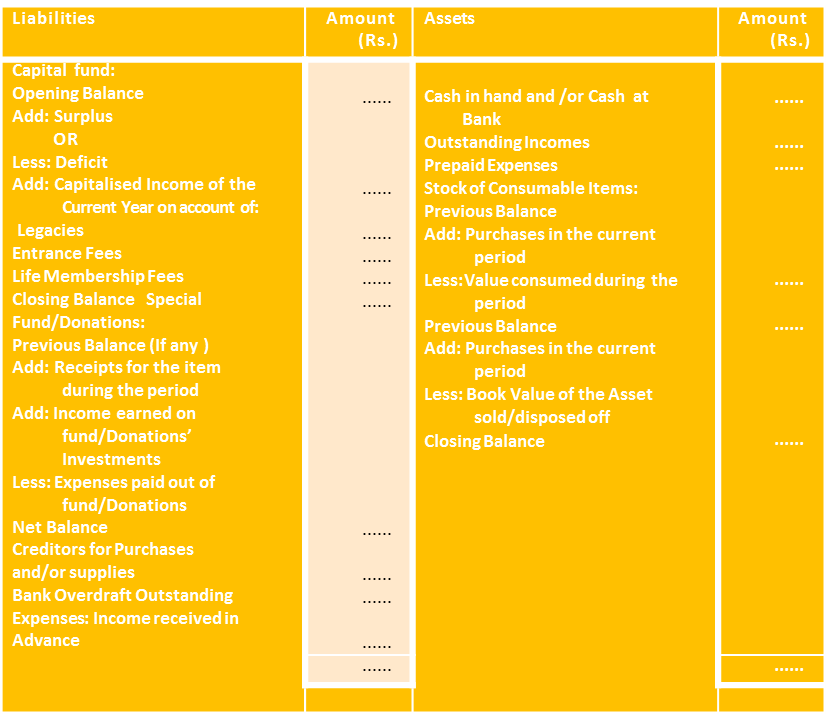

Preparation of Balance Sheet

The following procedure is adopted to prepare the Balance Sheet:

1. Take the Capital/General Fund as per the opening balance sheet and add surplus from the Income and Expenditure Account. Further, add entrance fees, legacies, life membership fees, etc. received during the year.

2. Take all the fixed assets (not sold/discarded/or destroyed during the year) with additions (from the Receipts and Payments account) after charging depreciation (as per Income and Expenditure account) and show them on the assets side.

3. Compare items on the receipts side of the Receipts and Payments Account with income side of the Income and Expenditure Account. This is to ascertain the amounts of: (a) subscriptions due but not yet received: (b) incomes received in advance; (c) sale of fixed assets made during the year; (d) items to be capitalised (i.e. taken directly to the Balance Sheet) e.g. legacies, interest on specific fund investment and so on.

4. Similarly compare, items on the payments side of the Receipt and Payment Account with expenditure side of the Income and Expenditure Account. This is to ascertain the amounts if: (a) outstanding expenses; (b) prepaid expenses; (c) purchase of a fixed asset during the year; (d) depreciation on fixed assets; (e) stock of consumable items like stationery in hand; (f) Closing balance of cash in hand and cash at bank as, and so on.

A proforma Balance Sheet is given for the proper understanding of preparing the balance sheet.

Balance Sheet of as on ...............

Fig. 1.2: Proforma Balance Sheet

Revision4

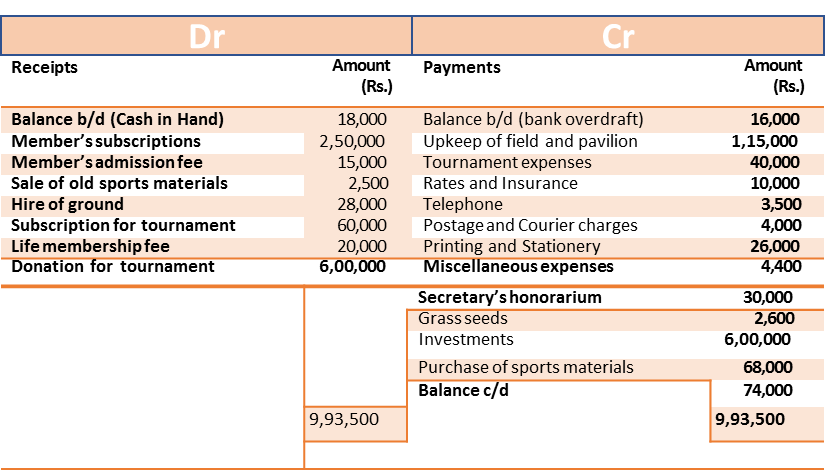

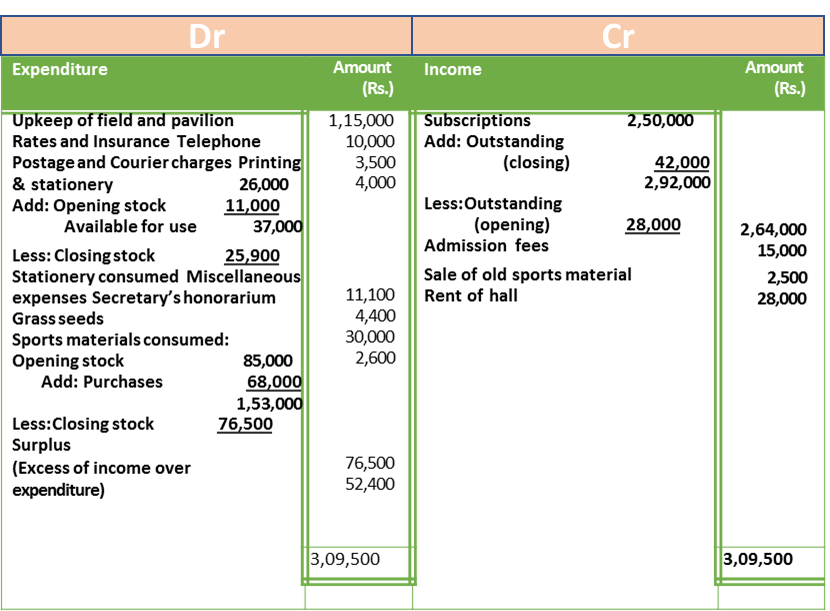

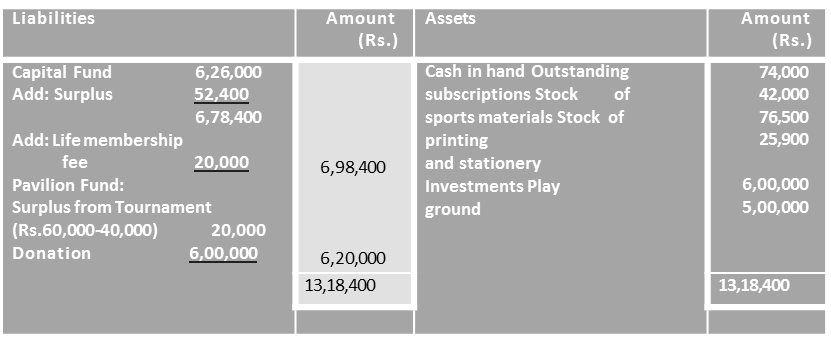

Donations and Surplus on account of tournament are to be kept in Reserve for a permanent pavilion. Subscriptions due on March 31, 2015 were Rs. 42,000. Write-off fifty per cent of sports materials and thirty per cent of printing and stationery.

Solution

Books of Excellent Cricket Club Income and Expenditure Account for the year ending on March 31, 2015

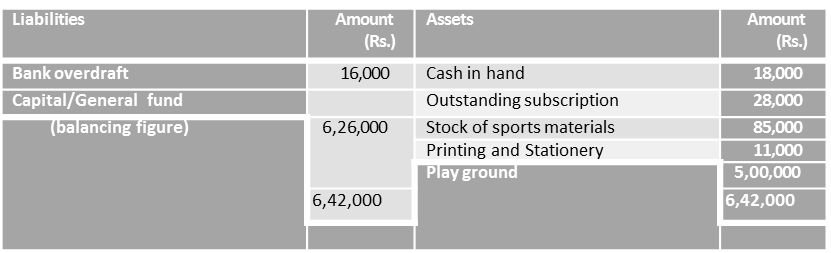

Note: Since the opening balance of the capital fund is not given, the same has been ascertained by preparing opening balance sheet.

Balance Sheet of Excellent Cricket Club as on March 31, 2015

Balance Sheet of Excellent Cricket Club as on March 31, 2014

Some Peculiar Items

Final accounts of the Not-for-Profit organisations are prepared on the similar pattern as that of a business orgnisation. However, a few items of income and expenses of such orgnisations are somewhat different in nature and need special attention in their treatment in final accounts. They are peculiar to these orgnisations. Some of the common peculiar items are explained as under:

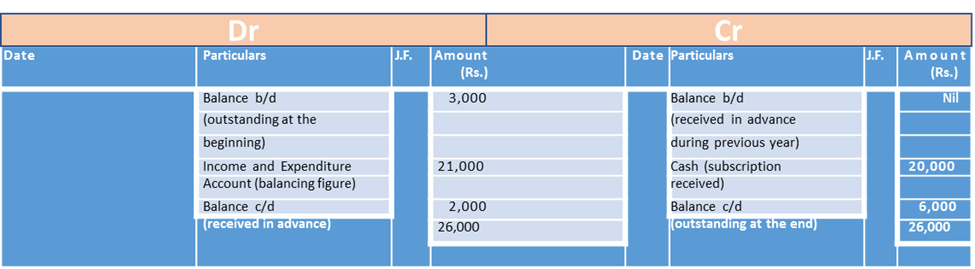

Subscriptions:

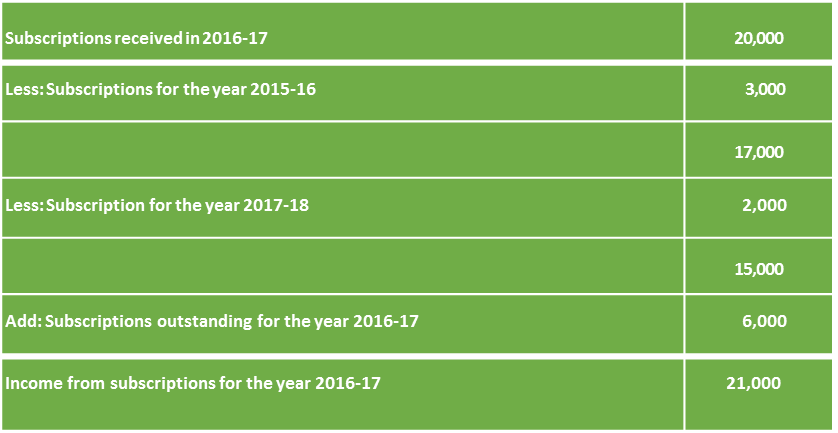

Subscription is a membership fee paid by the member on annual basis. This is the main source of income of such orgnisations. Subscription paid by the members is shown as receipt in the Receipt and Payment Account and as income in the Income and Expenditure Account. It may be noted that Receipt and Payment Account shows the total amount of subscription actually received during the year while the amount shown in Income and Expenditure Account is confined to the figure related to the current period only irrespective of the fact whether it has been received or not. For example, a club received Rs. 20,000 as subscriptions during the year 2016-17 of which Rs.3,000 relate to year 2015-16 and Rs.2,000 to 2017-18, and at the end of the year 2016-17 Rs.6,000 are still receivable. In this case, the Receipt and Payment Account will show Rs.20,000 as receipt from subscriptions. But the Income and Expenditure Account will show Rs. 21,000 as income from subscriptions for the year 2016-17, the calculation of which is given as below:

The above amount of subscriptions to be shown as income can also be ascertained by preparing the subscription account as follows:

Subscription Account

Revision 5

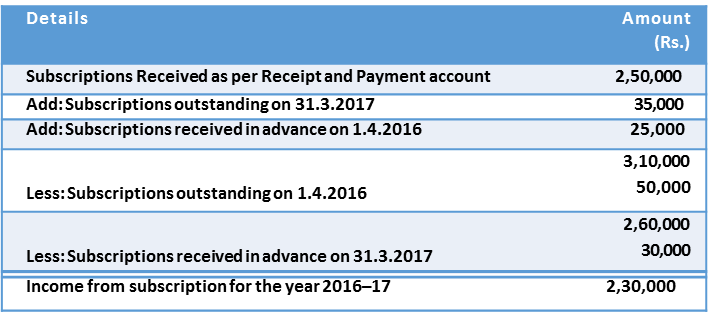

As per Receipt and Payment Account for the year ended on March 31, 2017, the subscriptions received were Rs. 2,50,000. Additional Information given is as follows:

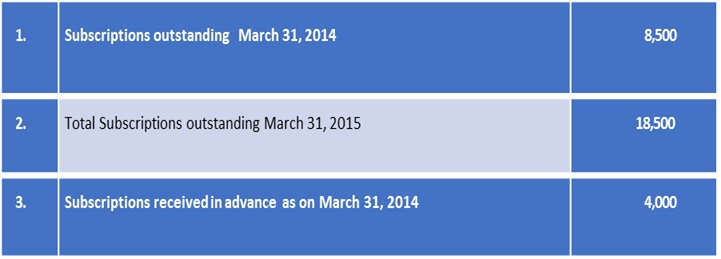

- Subscriptions Outstanding on 1.4.2016 Rs. 50,000

- Subscriptions Outstanding on 31.3.2017 Rs.35,000

- Subscriptions Received in Advance as on 1.4.2016 Rs.25,000

- Subscriptions Received in Advance as on 31.3.2017 Rs.30,000

Ascertain the amount of income from subscriptions for the year 2016–17 and show how relevant items of subscriptions appear in opening and closing balance sheets.

Solution

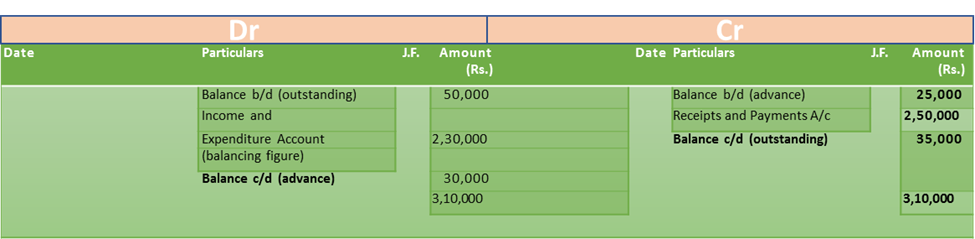

Alternately, income received from subscriptions can be calculated by preparing a Subscriptions account as under.

Subscription Account

Relevant items of subscription can be shown in the opening and closing balance sheet as under:

Balance Sheet as on March 31, 2014

Relevant data only

Balance Sheet as on March 31, 2015

Relevant data only

Revision 6

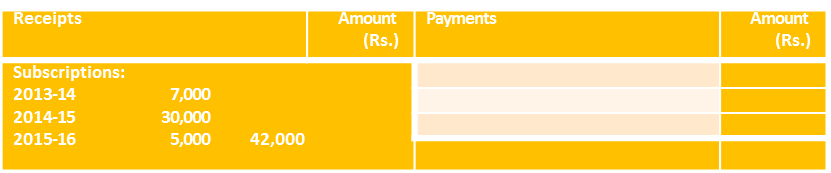

Extracts of Receipt and Payment Account for the year ended March 31, 2017 are given below:

Receipt Subscriptions (Rs.)

2015-16 2,500

2016-17 26,750

2017-18 1,000

30,250

Additional Information:

Total number of members: 230. Annual membership fee: Rs. 125.

Subscriptions outstandings on April 1, 2016: Rs. 2,750.

Prepare a statement showing all relevant items of subscriptions viz., income, advance, outstandings, etc.

Solution

Amount of subscription due for the year 2016-17 irrespective of cash Rs. 28,750 (i.e. Rs. 125 × Rs. 230).

Note: The amount of subscriptions outstanding as on 01-04-2017 has been ascertained as follows:

Revision 7

From the following extract of Receipt and Payment Account and the additional information, compute the amount of income from subscriptions and show as how they would appear in the Income and Expenditure Account for the year ending March 31, 2015 and the Balance Sheet.

Receipt and Payment Account for the year ending March 31, 2015

Additional Information:

Solution

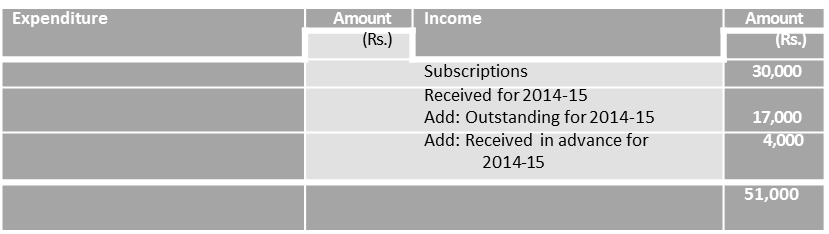

Income and expenditure account for the year ending on march 31, 2015

Note: Total amount of subscriptions outstanding as on 31-3-2015 are Rs. 18,500. This, includes Rs. 1,500 (Rs. 8,500 - Rs. 7,000) for subscriptions still outstanding for 2013-14. Hence, the subscriptions outstanding for 2014-15 are Rs. 17,000 (Rs. 18,500 - Rs. 1,500)

Balance Sheet (Relevant Data) as on March 31, 2015

Relevant data only

Donations:

It is a sort of gift in cash or property received from some person or organisation. It appears on the receipts side of the Receipts and Payments Account. Donation can be for specific purposes or for general purposes.

(i) Specific Donations: If donation received is to be utilised to achieve specified

purpose, it is called Specific Donation. The specific purpose can be an extension of the existing building, construction of new computer laboratory, creation of a book bank, etc. Such donation is to be capitalised and shown on the liabilities side of the Balance Sheet irrespective of the fact whether the amount is big or small. The intention is to utilise the amount for the specified purpose only.

(ii) General Donations: Such donations are to be utilised to promote the general purpose of the organisation. These are treated as revenue receipts as it is a regular source of income hence, it is taken to the income side of the Income and Expenditure Account of the current year.

Legacies:

It is the amount received as per the will of a deceased person who may or may not specify the use of the amount. Legacies, use of which is specified are specific legacy and is shown in the balance sheet as liability. If the use is not specified it is considered as revenue nature and credited to income and expenditure account.

Life Membership Fees:

Some members prefer to pay lump sum amount as life membership fee instead of paying periodic subscription. Such amount is treated as capital receipt and credited directly to the capital/general fund.

Entrance Fees:

Entrance fee also known as admission fee is paid only once by the member at the time of becoming a member. In case of organisations like clubs and some charitable institutions, is limited and the amount of entrance fees is quite high. Hence, it is treated as non-recurring item and credited directly to capital/general fund.

Sale of old asset:

Receipts from the sale of an old asset appear in the Receipts and Payments Account of the year in which it is sold. But any gain or loss on the sale of asset is taken to the Income and Expenditure Account of the year. For example, if an item furniture with a book value of Rs. 800 is sold for Rs. 700, this amount of Rs. 700 will be shown as receipt in Receipts and Payments Account and Rs. 100 on the expenditure side of the Income and Expenditure Account as a loss on sale of old asset and while showing furniture in the balance sheet Rs. 800 will be deducted from its total book value.

Sale of Periodicals:

It is an item of recurring nature and shown as the income side of the Income and Expenditure Account.

Sale of Sports Materials:

Sale of sports materials (used materials like old balls, bats, nets, etc) is the regular feature with any Sports Club. It is usually shown as an income in the Income and Expenditure Account.

Payments of Honorarium:

It is the amount paid to the person who is not the regular employee of the institution. Payment to an artist for giving performance at the club is an example of honorarium. This payment of honorarium is shown on the expenditure side of the Income and Expenditure Account.

Endowment Fund:

It is a fund arising from a bequest or gift, the income of which is devoted for a specific purpose. Hence, it is a capital receipt and shown on the Liabilities side of the Balance Sheet as an item of a specific purpose fund.

Government Grant:

Schools, colleges, public hospitals, etc. depend upon government grant for their activities. The recurring grants in the form of maintenance grant is treated as revenue receipt (i.e. income of the current year) and credited to Income and Expenditure account. However, grants such as building grant are treated as capital receipt and transferred to the building fund account. It may be noted that some Not-for-Profit organisations receive cash subsidy from the government or government agencies. This subsidy is also treated as revenue income for the year in which it is received.

Special Funds

The Not-for-Profit Organisations office create special funds for certain purposes/activities such as 'prize funds', 'match fund' and 'sports fund', etc. Such funds are invested in securities and the income earned on such investments is added to the respective fund, not credited to Income and Expenditure Account. Similarly, the expenses incurred on such specific purposes are also deducted from the special fund. For example, a club may maintain a special fund for sports activities. In such a situation, the interest income on sports fund investments is added to the sports fund and all expenses on sports deducted there from. The special funds are shown in balance sheet. However, if, after adjustment of income and expenses the balance in specific or special fund is negative, it is transferred to the debit side of the Income and Expenditure Account or adjusted as per prescribed directions. (see Illustrations 8 and 9.)

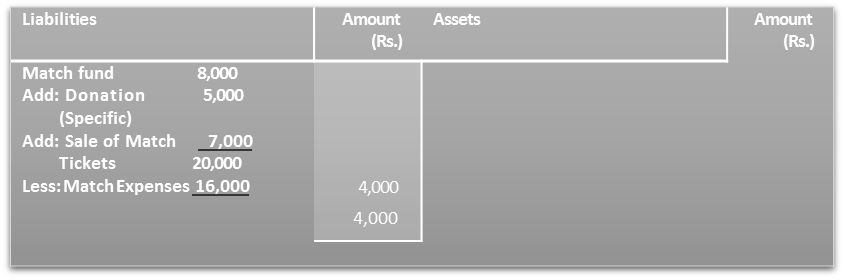

Revision 8

Show how you would deal with the following items in the financial statements of a Club:

Solution

Revision 9

(a) Show the following information in financial statements of a ' Not-for-Profit' Organisation:

(b) What will be the effect, if match expenses go up by Rs. 6,000 other things remaining the same?

Solution

(a) Balance Sheet as on………..*

Only relevant data.

(b) If match expenses go up by Rs. 6,000, the net balance of the match fund becomes negative i.e. Debit exceeds the Credit, and the resultant debit balance of Rs. 2,000 shall be charged to the Income and Expenditure Account of that year.

Revision 10

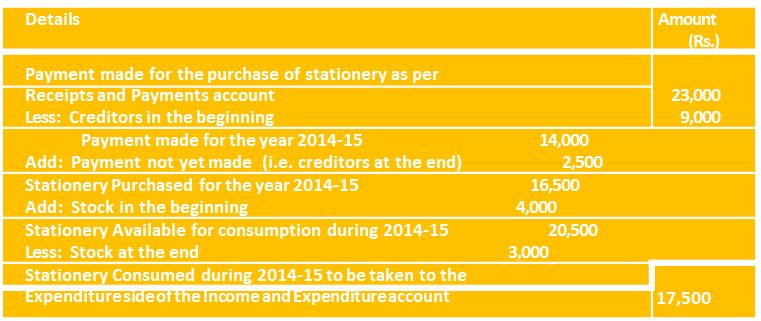

Extract of a Receipt and Payment Account for the year ended on March 31, 2015:

Payments: Stationery Rs. 23,000

Additional Information:

Solution

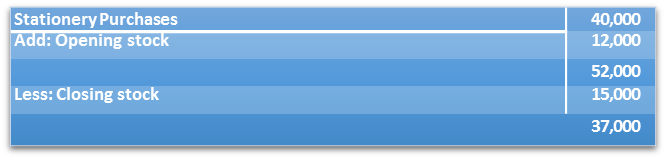

Stationery:

Normally expenses incurred on stationary, a consumable items are charged to Income and Expenditure Account. But in case stock of stationery (opening and/or closing) is given, the approach would be make necessary adjustments in purchases of stationery and work out cost of stationery consumed and show that amount in Income and Expenditure Account and its stock in the balance sheet. For example, the Receipt and Payment Account shows a payment for stationery amounting to Rs. 40,000 and there is an opening and closing stationery amounting to Rs. 12,000 and Rs. 15,000. The amount of expense on stationery will be worked out as follows:

In case stationery is also purchased on credit, the amount of its consumption will be worked out as given in Revision12.

Revision 11

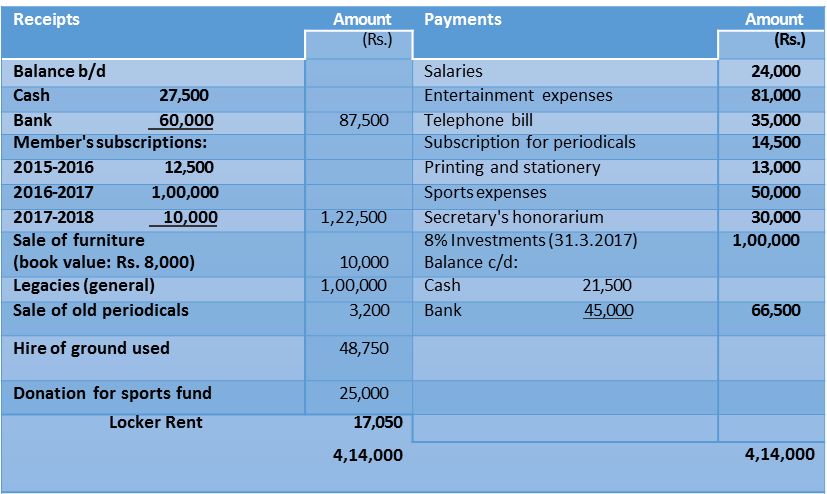

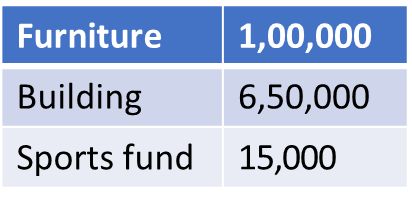

Following is the Receipt and Payment Account of an Entertainment Club for the period April 1, 2016 to March 31, 2017.

Receipt and Payment Account for the year ending March 31, 2017

Additional Information

- The club had 225 members, each paying an annual subscription of Rs. 500. Subscription outstanding as on 31 March 2016 Rs. 15,000.

- Telephone bill outstanding for the year 2016-2017 is Rs. 2,000.

- Locker Rent Rs. 3,050 outstanding for the year 2015-16 and Rs. 1,500 for 2016-17.

- Salary outstanding for the year 2016-17 Rs. 4,000.

- Opening Stock of Printing and stationery Rs. 2,000 and closing stock of printing and stationery is Rs. 3,000 for the year 2016-17.

- On 1st April 2016 other balances were as under:

- Depreciation Furniture and Building @ 12.5% and 5% respectively assuming that it is on reducing balance for the year ending March 31,2017

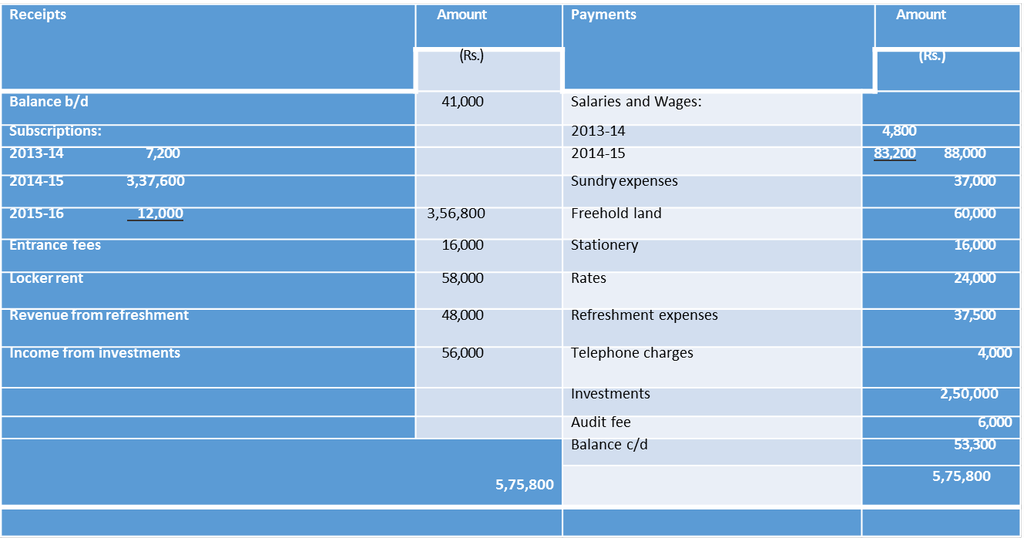

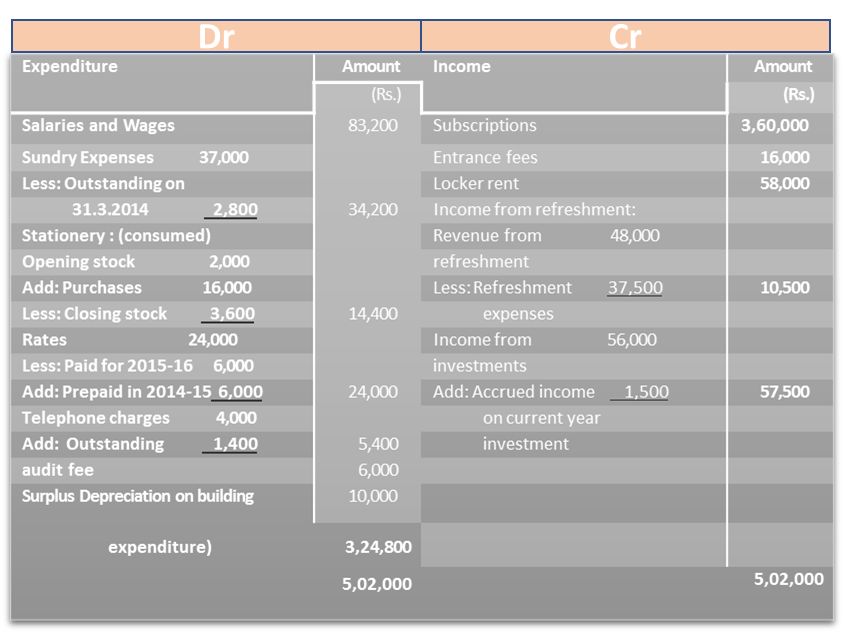

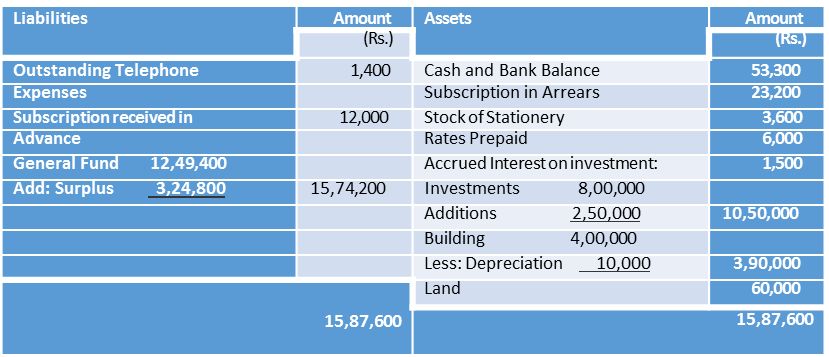

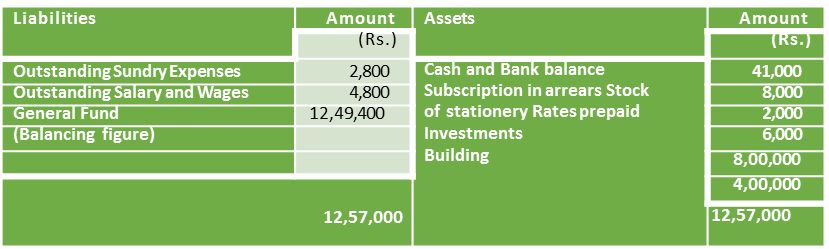

Prepare Income and Expenditure account and Balance Sheet as on that date.

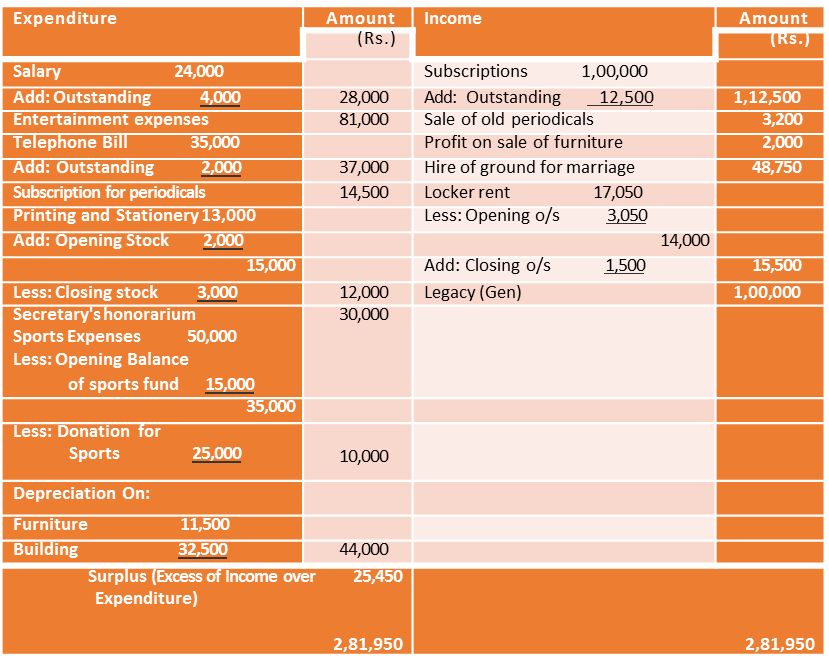

Book of entertainment club

Income and expenditure account for the year ending on march 31, 2017

Solution

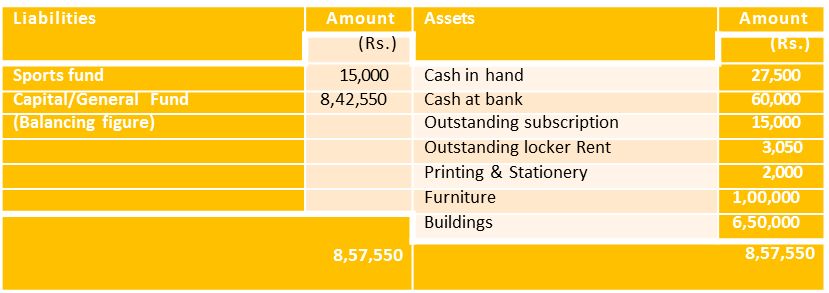

Balance Sheet of Entertainment Club as on March 31, 2016

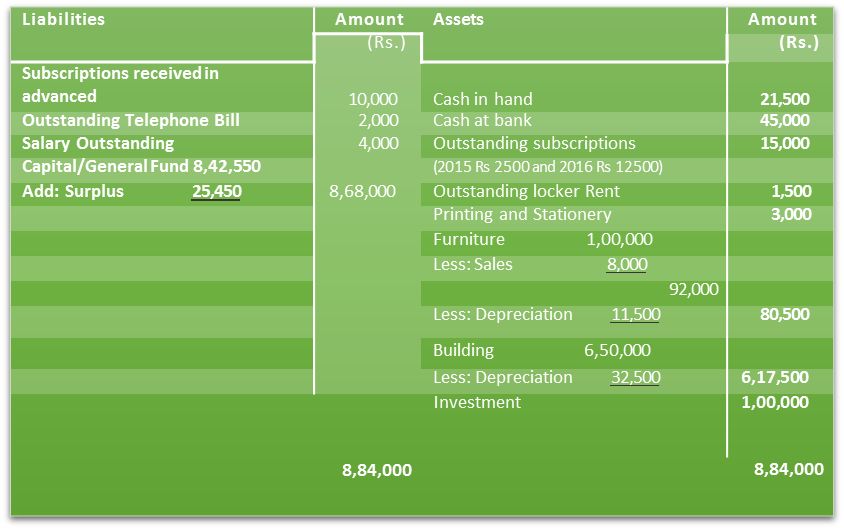

Balance Sheet of Entertainment Club as on March 31, 2017

Revision 12

Prepare Income and Expenditure Account and Balance Sheet for the year ended

March 31, 2015 from the following information.

Receipt and Payment Account for the year ending March 31, 2015

The following additional information is provided to you:

1. There are 1800 members each paying an annual subscription of

Rs. 200, Rs. 8,000 were in arrears for 2013-14 as on April 1, 2014.

2. On March 31, 2015 the rates were prepaid to June 2015; the charge paid every year being Rs. 24,000.

3. There was an outstanding telephone bill for Rs. 1,400 on March 31, 2015.

4. Outstanding sundry expenses as on March 31, 2014 totaled Rs. 2,800.

5. Stock of stationery as on March 31, 2014 was Rs. 2000; on March 31, 2015, it was Rs. 3,600.

6. On March 31, 2014 Building stood at Rs. 4,00,000 and it was subject to depreciation @ 2.5% p. a.

7. Investment on March 31, 2014 stood at Rs. 8,00,000.

8. On March 31, 2015, income accrued on investments purchased during the year amounted to Rs. 1,500.

Solution

Income and Expenditure Account for the year ending on March 31, 2015

Balance Sheet as on March 31, 2015

Balance Sheet as on March 31, 2014

Working Note :

Revision 13

Following is the Receipt and Payment Account of Friendship Club in respect of the Year on 31.3.2016

Receipt and Payment Account for the year ending March 31, 2016.

Additional Information :

1. There are 500 members, each paying an annual subscription of Rs. 50, Rs. 17,500 being in arrears for 2014-15 at the beginning of 2015-16. During 2014-15, subscriptions were paid in advance by 40 members for 2015-16.

2. Stock of stationery on March 31, 2015, was Rs. 1,500 and on March 31, 2016, Rs. 2,000.

3. On March 31, 2016, the rates and taxes were prepaid to the following January 31, the annual charge being Rs. 1,500.

4. Telephone bill unpaid as on March 31, 2015 Rs. 3,000 and on March 31, 2016 Rs. 1,500.

5. Sundry expenses accruing at 31.3.2015 were Rs. 250 and at March 31, 2016 Rs. 300.

6. On March 31, 2015 Building stood in the books at Rs. 2,00,000 and it is required to write off depreciation @ 10% p.a.

7. Value of 8% Government Securities on March 31, 2015 was Rs. 75,000 which were purchased at that date at Par. Additional Government Securities worth Rs. 25,000 are purchased on March 31, 2016.

You are required to prepare:

(a) An Income and Expenditure Account for the year ended on 31.3.2016 (b) A Balance Sheet on that date.

Solution

Books of Friendship Club

Balance sheet as on march 31, 2015

Income and Expenditure Account for the year ending on March 31, 2015

Verification: 500 x 50 = 25000.

Balance Sheet of Friendship Club as on March 31, 2016

Income and Expenditure Account based on Trial Balance

In case of not-for-profit organisations, normally the Income and Expenditure Account and Balance Sheet is prepared based on the Receipts and Payments Account and the additional information given. But, sometimes, the trial balance along with some additional information is given for this purpose. See Revision 14.

Revision 14

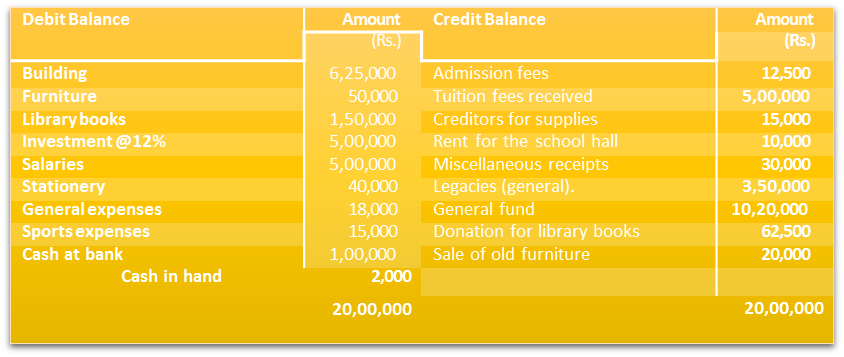

From the trial balance and other information given below for a school, prepare Income and Expenditure Account for the year ended on 31.3.2017 and a Balance Sheet as on that date:

Additional Information:

(i) Tution fee yet to be received for the year are Rs. 25,000.

(ii) Salaries yet to be paid amount to Rs.30,000.

(iii) Furniture costing Rs. 40000 was purchased on October 1, 2016 was sold for Rs. 20,000.

(iv) The book value of the furniture sold was Rs. 50,000 on April 1, 2016 was sold for Rs. 20,000.

(v) Depreciation is to be charged @ 10% p.a. on furniture, 15% p.a. on Library books, and 5% p.a. on building.

Solution

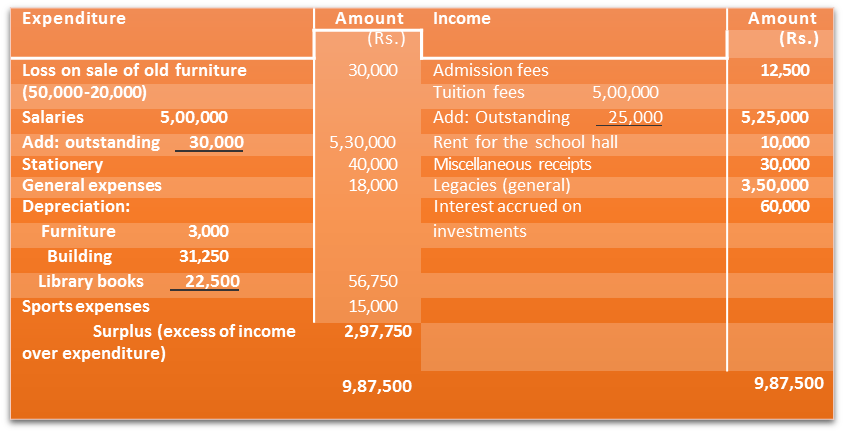

Income and Expenditure Account for the year ending on March 31, 2017

Working Notes:

1. As admission fee is a regular income of a school, so it has been taken as a revenue income of the school.

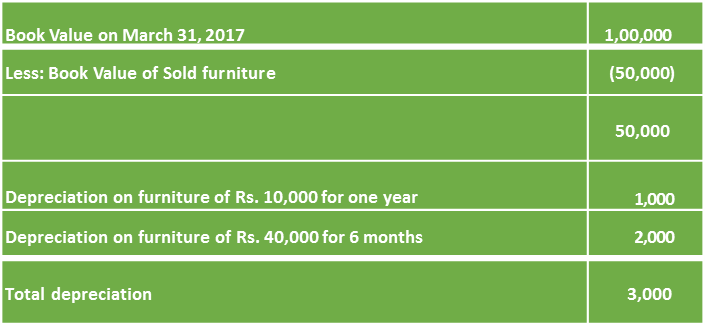

2. Depreciation on furniture has been computed as following on the assumption that furniture was sold on April 1, 2016.

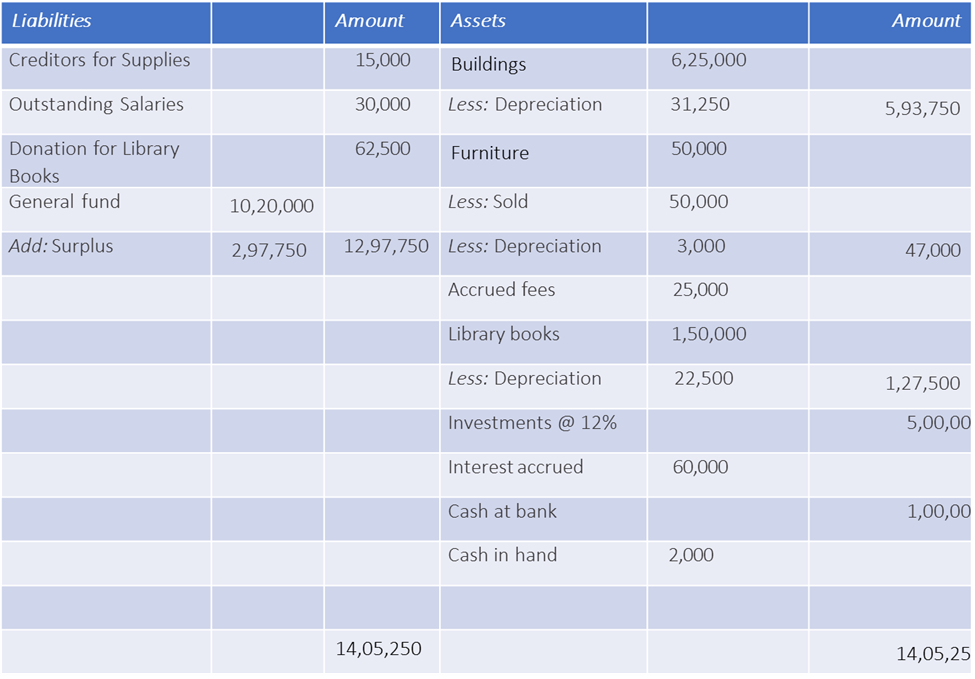

Balance Sheet as on March 31, 2017

Revision 15

Prepare Income and Expenditure Account of Entertainment Club for the year ending March 31, 2017 and Balance Sheet as on that date from the following information:

Receipt and Payment Account For the year ending on March 31, 2017

Additional Information:

Solution

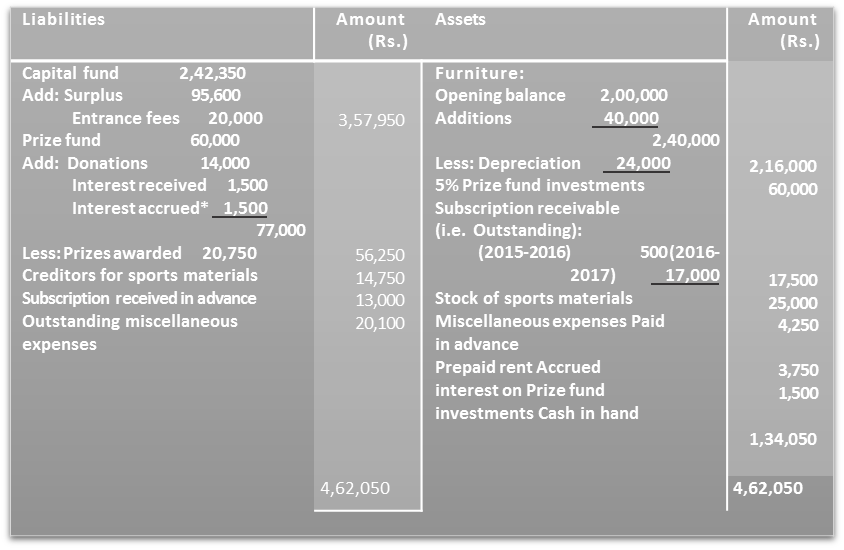

Books of Entertainment Club Income and Expenditure Account for the year ending March 31, 2017

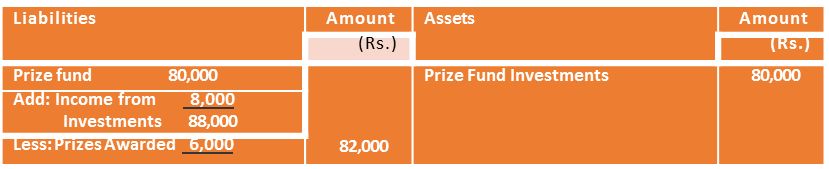

Balance Sheet of Entertainment Club as on March 31, 2016

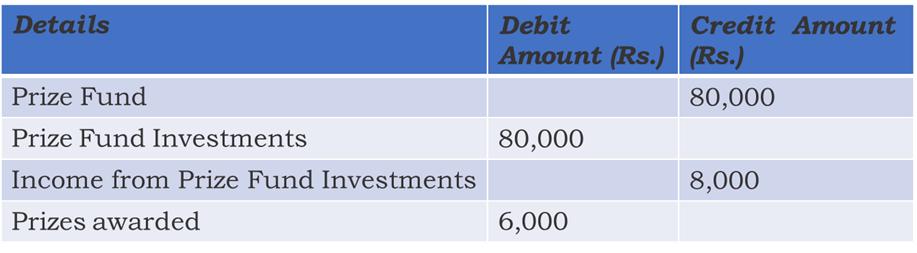

Note: Interest on Prize Fund Investments @ 5% amounts to Rs. 3,000 whereas only Rs. 1,500 have been received; so the balance is treated as Accrued interest.

It is preferable to prepare separate accounts of various items involving many transactions. In this case Account for Subscription, Miscellaneous Expenses, and Sports Materials may be made as a Classroom activity.

Revision 16

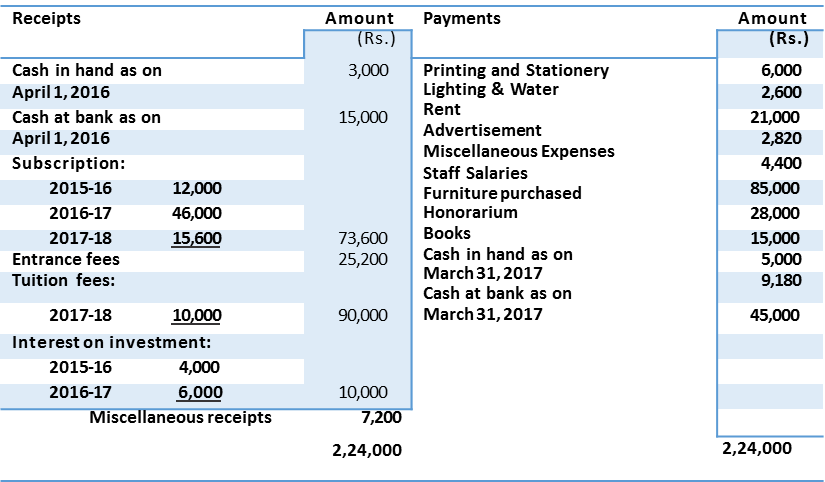

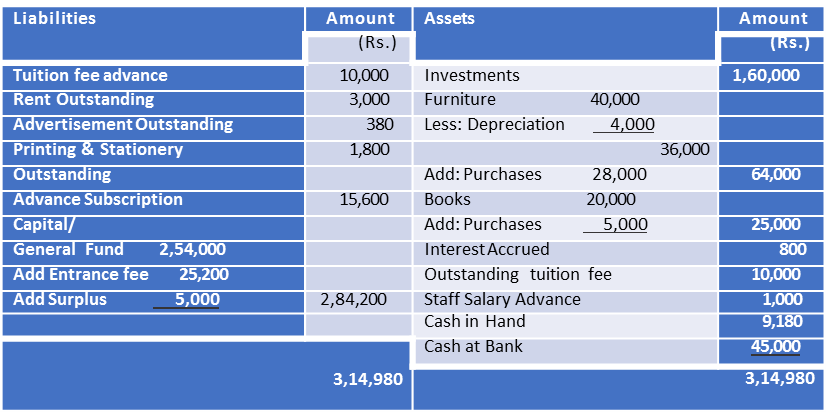

Shiv-e-Narain Education Trust provides the information in regard to Receipt and Payment Account and Income and Expenditure Account for the year ended March 31st 2017:

On March 31, 2016 the following balances appeared:

Investments Rs.1, 60,000; Furniture Rs.40, 000; and Books Rs.20, 000.

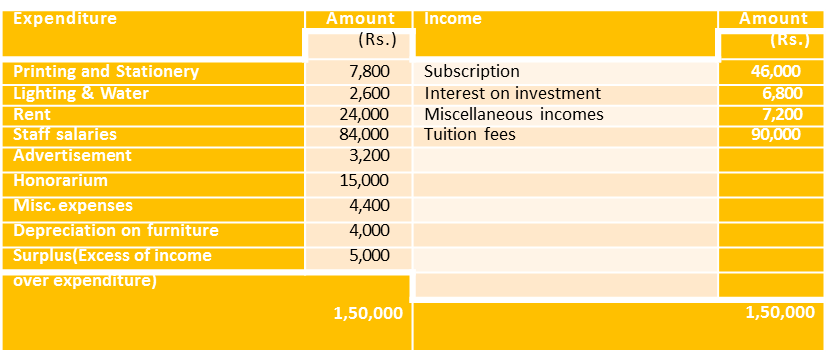

Income and Expenditure Account for the year ending on March 31, 2017

Prepare opening and closing balance sheet

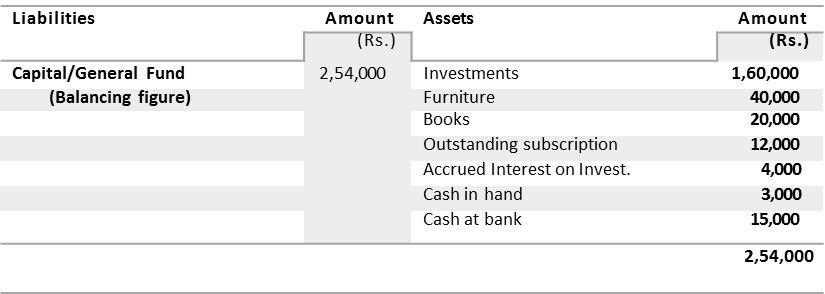

Solution

Shiv-e-Narain Education Trust Balance Sheet as on March 31, 2016

Note:

1. Income and Expenditure Account for the current year shows interest on investment income Rs.6,800 while Receipts and Payments Account shows the receipts of Rs.6,000 the difference of Rs.800 means interest on investment has become due but not yet receivable during the year.

2. Income and Expenditure Account shows Rs.90,000 as income from Tuition fees. However, the Receipts and Payments Account shows Rs.10,000 as tuition fees received for the year 2017-18 and Rs.80,000 for 2015-16. It implies that Rs.10,000 on account of tuition fees for the year 2016-17 are still receivable (i.e. Tuition fees are outstanding).

3. Receipt and Payment Account shows a payment of Rs.85,000 on account of staff salaries, but the Income and Expenditure Account shows expenditure of Rs.84,000 on account of staff salaries. It means the excess of Rs.1,000 shown in the Receipt and Payment Account may either belong to the pervious year or the next year. Their is no evidence that staff salaries of Rs.1,000 was outstanding at the end of the previous year 2013-14. This is why this payment of Rs.1,000 has been considered as an advance salaries to the staff.

Summary

- Difference between Profit Seeking Entities and Not-for-Profit Entities: Profit- seeking entities undertake activities such as manufacturing trading, banking and insurance to bring financial gain to the owners. Not-for-Profit entities exist to provide services to the member or to the society at large. Such entities might sometimes carry on trading activities but the profits arising therefrom are used for further the service objectives.

- Appreciation of the need for separate Accounting Treatment for Not-for-Profit Organisations: Since not-for-profit entities are guided primarily by a service motive, the decisions made by their managers are different from those made by their counterparts in profit-seeking entities. Differences in the nature of decisions implies that the financial information on which they are based, must also be different in content and presentation.

- Explanation of the nature of the Principal Financial Statements prepare by Not-for- Profit enterprises: Not-for-Profit Organisations that maintain accounts based on the double-entry system of accounting, generally prepare three principal statements to fulfil their information needs. These include Receipts and Payments Account, Income and Expenditure Account, and a Balance Sheet. The Receipts and Payments Account is summarised under relevant heads, cash book which records all cash Receipts and cash Payments without distinguishing between capital and revenue items, and between items relating to the current year and those relating to previous or future years. The Income and Expenditure Account is an income statement which is prepared to ascertain the excess of revenue income over revenue expenditure or vice versa, for a particular accounting year, as a result of the entity's overall activities. Although it is considered to be a substitute for the Trading and Profit and Loss Account of a profit-seeking entity, there are certain conceptual differences between the two statements. The Balance Sheet is prepared at the end of the entity's accounting year to depict the financial position on that date. It includes the Capital Fund or Accumulated Fund, special purpose funds, and current liabilities on the left hand or liabilities side, and fixed assets and current assets on the right hand or assets side.

- Difference between the Receipt and Payment Account and the Income and Expenditure Account: Many differences exist between the Receipt and Payment Account and the Income and Expenditure Account which is evident from the nature and purpose of two statements. While the former records both capital and revenue receipts and payments relating to any accounting year, the latter records only revenue items relating to the current accounting year. Non-cash expenses such as depreciation on fixed assets and outstanding incomes and expenses are shown in the latter but omitted in the former. The Receipt and Payment Account has an opening balance while the Income and Expenditure Account does not. The closing balance of the former account represents cash and bank balances on the closing date while in the latter account it indicates surplus or deficit from the activities of the enterprise.

- Conversion of a Receipt and Payment Account into an Income and Expenditure Account: This essentially involves five steps namely, (i) adjusting the revenue receipts on the debit side to include accrued incomes and incomes relating to the current year received earlier and to exclude amounts received in arrears or in advance; (ii) adjusting revenue payments on the credit side; (iii) identifying and showing non-cash expenses and losses on the debit side of the Income and Expenditure Account; (iv) computing and showing profits/losses from trading and/or social activities on the credit/debit side of the Income and Expenditure Account; and (v) ascertaining the surplus or deficit as the closing balance of the Income and Expenditure Account.

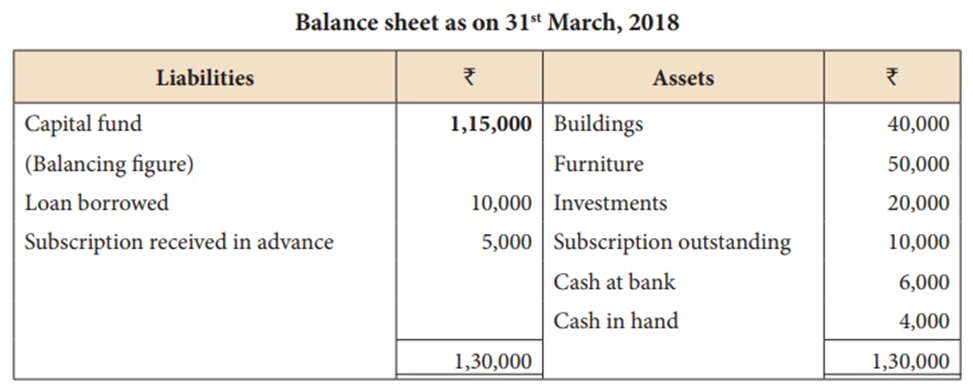

How to Prepare Opening & Closing Balance Sheet?

Step 1 – Take into account the closing balances of assets & liabilities of the previous year & the opening balances of the Receipts & Payments A/c will be the cash in hand & cash at the bank as of that date. The Balancing Figure will be Capital Fund

Step 2 – After the preparation of the opening Balance Sheet, we shall proceed towards the preparation of the Closing Balance Sheet& for this purpose, the assets will be then adjusted for any sale or purchase during the year. Any gain or loss on the sale of assets will be taken to Income & Expenditure A/c. Any depreciation will also be taken to Income & Expenditure A/c. Only the net assets will appear on the Balance Sheet& the payments made for the purchase of new assets in the Receipts & Payments A/c shall appear as the new asset or added to the old assets.

Step 3 – From the Receipts side, any capital receipts like contributions to Building Fund & specific funds like specific donations will be recorded on the liabilities side.

Step 4 – Adjustments for prepaid & outstanding expenses will be made to the relevant expenses. Outstanding expenses & advance subscriptions will appear on the liabilities side whereas prepaid expenses & outstanding subscriptions will appear on the asset side.

Step 5 – The liabilities appearing in the previous year’s Balance Sheet should be checked with the payments made during the year. If some liabilities have been paid, then these liabilities will not appear in the new Balance Sheet to the extent they are paid. Only the net unpaid amount if any will appear on the Balance Sheet.

Step 6 – Finally, the Capital Fund balance from Opening Balance Sheet shall be adjusted with surplus or deficit from the Income & Expenditure A/c & also any specific fund which is not required anymore will be added to the Capital fund.

AN EXAMPLE OF CLOSING A BALANCE SHEET

Meaning and Treatment of Special Items

The meaning and treatment of the special items in the financial statements of non-profit making organizations are as follows:

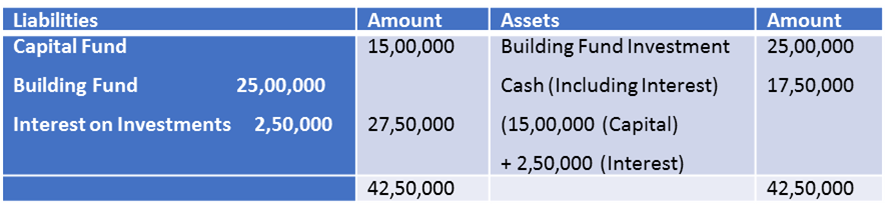

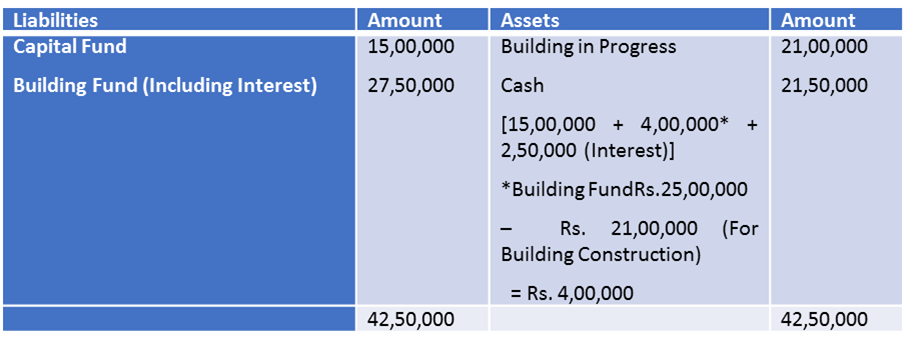

1. Capital Fund

Non-profit organizations follow FUND BASED ACCOUNTING method. In this method, the fund is of two types i.e. General Fund or Capital Fund & Specific Fund. The capital introduced is known as the General Fund or Capital Fund. It is an unrestricted fund that can be used to achieve the objectives of society. All the recurring expenses like salary and rent are charged to General Fund through Income & Expenditure A/c similarly all the revenues are added to the General Fund through Income & Expenditure A/c. If the fund money is invested somewhere then the interest earned will be directly added to the General Fund/Capital Fund.

On the other hand, Specific Fund is a restricted fund set up for a specific purpose. The money can be used only for the achievement & realization of that particular purpose. The restriction on the use of this fund is either put by the donor or by the management. If the fund money is invested somewhere then the interest earned will be directly added to the specific Fund. It is again classified into two types;

- Specific Asset Building – Funds used for building some fixed assets like Building or Pavilion.

![]()

![]()

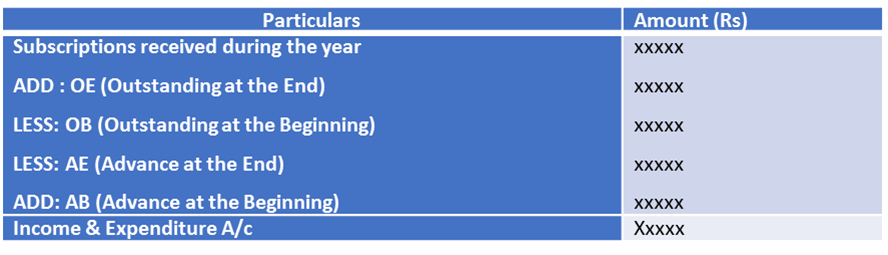

2. Subscriptions

Subscriptions are collected by non-profit making organizations from their members regularly. It is revenue in nature. It is the main source of income for any non-profit making organization. Subscriptions related to the current year shall be recorded in Income & Expenditure A/c whether received or not. Subscriptions due for the current year shall also be shown in the asset side of the Balance Sheet. Subscriptions received in advance for next year shall not appear in the Income & Expenditure A/c as it is not a current year item but the amount received in advance shall be recorded as a liability in the Balance sheet as it is a prepaid income.

Explanation:-

Income& Expenditure A/c is nothing but P/L A/c with a different name. Since the purpose of preparing P/L A/c is to find out the current year's profit or loss, therefore, only current items of revenue nature is recorded in P/L A/c. In the same way, Income & Expenditure A/c also records only the current year items & items of the previous year & next year are excluded.

- Outstanding at the end shall be added as it is a current year item.

- Outstanding at the beginning shall be deducted as it is a previous year's item (last year’s closing outstanding is this year’s opening outstanding)

- Advance at the End is not a current year item. It is the membership fees received for next year in advance so it’ll be deducted from the total subscriptions received.

- Advance at the beginning is this year’s income because it represents last year’s closing advance i.e. membership fees for the current year received in advance during the previous year.

3. Donations

A non-profit making organization may receive donations from time to time. Donations received for a particular purpose like the development of a pavilion, construction of a building, awarding prizes etc. are called specific donations. A donation received not for a specific purpose is called a general donation.

Accounting Treatment: All specific donations are to be capitalized i.e. put in the liabilities side of the Balance Sheet.

If the general donation is a big amount it is to be capitalized i.e. added to the Capital Fund in the liabilities side of the Balance sheet.

In case the general donation is a small amount it is treated as income and put in the credit side of the Income and Expenditure Account.

Note: Whether the amount of general donation is big or small, it is judged by considering the nature of the activities of the non-profit making organizations.

4. Entrance Fees

This is the fee collected from the new entrants on admission to the clubs or societies etc. It is also known as admission fees.

Accounting Treatment: The entrance fees may be treated as revenue or capital depending upon the rule and by-laws of the organizations.

5. Legacies

It is a kind of gift received by a non-profit making organisation as per the will of a deceased person.

Accounting Treatment: If legacy is a small amount, it is treated as an income and is to be taken in the credit side of Income and Expenditure Account.

In case of a big amount, it should be capitalised i.e. added to Capital Fund in the liabilities side of Balance Sheet.

Note:Whether the amount of legacy is big or small, it is judged by considering the nature of activities of non-profit making organisation.

6. Life Membership Fees

Membership fees for the whole life collected from members is known as life membership fees. In this case the member is to pay a lump-sum amount instead of periodic payments and enjoys the benefits of the organisation till the end of his life.

Accounting Treatment: Life membership fees is treated as capital item and hence added to the Capital fund.

Note: However, there is another way of treatment.

It is credited to a separate fund (Life Membership Fees Account) and an amount equal to the annual membership fee (subscription) is transferred to the Income and Expenditure Account. The balance in the separate fund is shown in the liabilities side of the Balance Sheet. If a life member dies, then the balance lying in the special fund is transferred to the Capital Fund of the organization.

7. Special Fund

Sometimes a non-profit making organisation may create funds for some special purposes. For example, a sports club may create Tournament Fund for meeting tournaments expenses or a building fund for the construction of building etc.

Accounting Treatment: The fund may be invested in banks or in Govt. securities.

- Any income relating to such special fund is added to this fund.

- Any expenditure on account of this fund is subtracted from such fund.

- Such special fund appears in the liabilities side of Balance Sheet.

- If there is deficit (the expenditure on account of fund is more than the amount of fund) it is recorded in the expenditure side of Income and Expenditure Account.

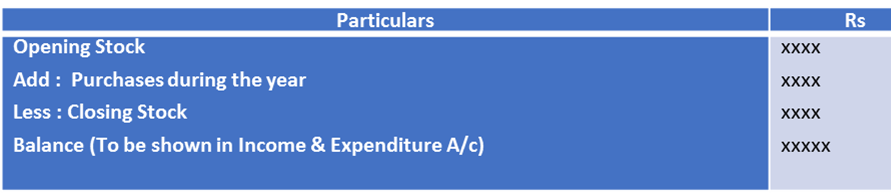

8. Calculation of Cost of Consumable Goods – Consumable goods are the items that are used or consumed during the year such as sports material, stationery, books, medicines, and food items. In the Income & Expenditure A/c, only the amount of such items consumed will during the year be shown. Therefore, it is necessary to find out the cost of consumption of such goods.

STEPS TO PREPARE INCOME & EXPENDITURE A/C FROM RECEIPTS & PAYMENTS A/C

- Prepare the Opening Balance Sheet to find out the opening balance of Capital Fund (if it is not given).

- Identify the revenue receipts from the receipts side of Receipts & Payment A/c & show them in the Income side of the Income & Expenditure A/c. Capital receipts will be shown in the Balance sheet.

- Identify the Capital expenditure from the payment side of Receipts & Payment A/c & show it in the Balance sheet. Capital items won’t appear in Income & Expenditure A/c.

- Certain items do not appear in Receipts & Payment A/c but shall be recorded in Income & Expenditure A/c such as depreciation of fixed assets, loss on sale of fixed assets, and profit on the sale of fixed assets. Depreciation & loss shall be shown in the Expenditure side whereas profit on the sale of fixed assets shall be shown in the Income side.

- Finally, find out the surplus or deficit i.e. if the income side is higher it is surplus & if the expenditure side is higher then it is a deficit.

- Prepare Closing Balance Sheet by taking into consideration the opening balance of assets & liabilities, surplus/deficit, purchase & sale of assets during the year & depreciation on fixed assets. The surplus shall be added to the Capital whereas the Deficit shall be deducted from the Capital.

INCIDENTAL TRADING ACTIVITY

This Incidental Trading activity is also known as incidentals, these are the gratuities and the fees or costs which are incurred in addition to the main item, service or event paid for during the trading pursuits.

Trading pursuits like a hospital or a chemist shop or even a beauty parlor or canteen, all these places can also in use to furnish certain provisions to the members or public. In this scenario, the trading A/c has to be drawn to determine the outcome of this incidental pursuit. The profit from these trading pursuits is solicited to accomplish the primary objectives which satisfy the cause for which the establishment was set up, then it is transferred to the Income and Expenditure A/c.

In Relation to the Above, the following are the Details:

- The trading A/c has to be outlined to ascertain either profit or loss due to incidental commercial pursuit. All these costs and revenues in a straight way and principally are associated with such pursuits, are documented in the trading A/c. After this, the Balance of the trading A/c is being transferred to the Income and Expenditure A/c

- Income and Expenditure A/c documents, also the trading profit (or loss), and all other incomes and expenses are not documented in the Trading A/c. Surfeit or deficit is disclosed by the Income and Expenditure A/c as is being transferred to the capital or general fund.