Vision classes

Vision classes

- Books Name

- Vision classes Accountancy Book

- Publication

- Vision classes

- Course

- CBSE Class 11

- Subject

- Accountancy

Purchase Book

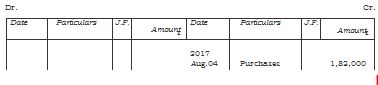

All credit purchases of goods are recorded in the purchases journal whereas cash purchases are recorded in the cash book. Other purchases such as purchases of office equipment, furniture, building, are recoded in the journal proper if purchased on credit or in the cash book if purchased for cash. The source documents for recording entries in the book are invoices or bills received by the firm from the supplies of the goods. Entries are made with the net amount of the invoice. Trade discount and other details of the invoice need not be recorded in this book. The format of the purchases journal is shown in figure 4.6.

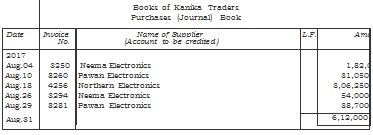

Purchases (Journal) Book

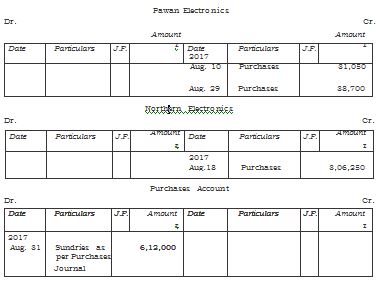

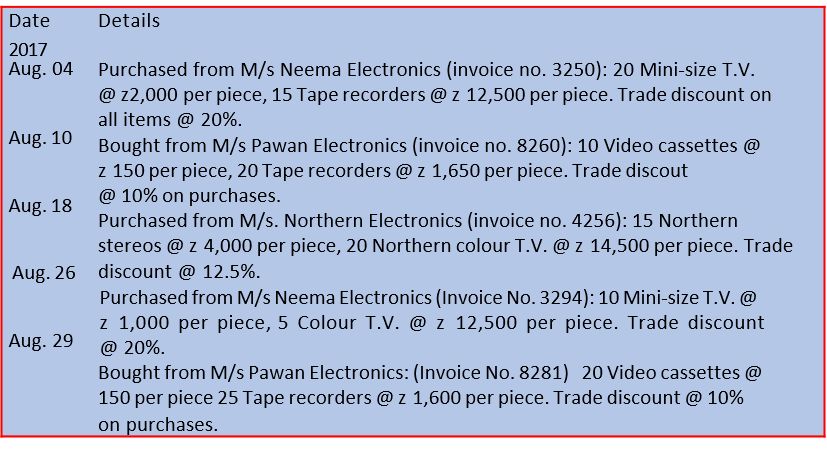

The monthly total of the purchases book is posted to the debit of purchases account in the ledger. Individual suppliers accounts may be posted daily. Consider the following details obtained from M/s Kanika Traders and observe how the entries are recorded in the purchase journal.

Posting from the purchases journal is done daily to their respective accounts with the relevant amounts on the credit side. The total of the purchases journal is periodically posted to the debit of the purchases account normally on the monthly basis. However, if the number of transactions is very large, this total may be done and posted at some other convenient time interval such as daily, weekly or fortnightly. The posting from the purchases journal to the ledger from is illustrated as follows:

Books of Kanika Electronics Neema Electronics