Vision classes

Vision classes

- Books Name

- Vision classes Accountancy Book

- Publication

- Vision classes

- Course

- CBSE Class 11

- Subject

- Accountancy

Purchase Return Book

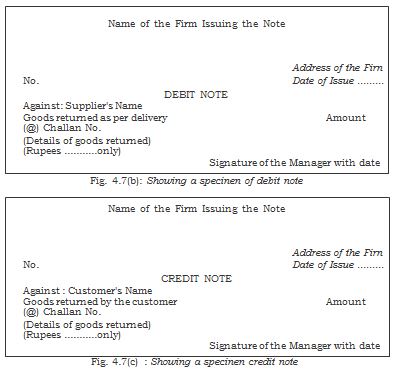

Sometimes goods purchased are returned to the supplier for various reasons such as the goods are not of the required quality, or are defective, etc. For every return, a debit note (in duplicate) is prepared and the original one is sent to the supplier for making necessary entries in his book. The supplier may also prepare a note, which is called the credit note. The source document for recording entries in the purchases return journal is generally a debit note. A debit note will contain the name of the party (to whom the goods have been returned) details of the goods returned and the reason for returning the goods. Each debit note is serially numbered and dated.

Purchases Return (Journal) Book

Debit and Credit Notes

A Debit note is a document evidencing a debit to be raised against a party for reasons other than sale on credit. On finding that goods supplied are not as per the terms of the order placed, the defective goods are returned to the supplier of the goods and a note is prepared to debit the supplier; or when an additional sum is recoverable from a customer such a note is prepared to debit the customer with the additional dues. In these two situations the note is called a debit.

On the other hand, a Credit note is prepared, when a party is to be given a credit for reasons other than credit purchase. It is a common practice to make it in red ink. When goods are received back from a customer, a credit note should be sent to him.