Vision classes

Vision classes

- Books Name

- Vision classes Accountancy Book

- Publication

- Vision classes

- Course

- CBSE Class 11

- Subject

- Accountancy

Procedure of preparing Bank Reconciliation Statement (BRS)

A Bank Reconciliation Statement is prepared when we get the duly completed Pass Book from the Bank.

- First of all tally the Debit side entries of the cash book with the Credit side entries of the Pass Book and vice versa.

- Tick the items appearing in both the books.

- Unticked items will be the points of differences.

- A BRS is then prepared by taking either the balance as per Cash Book or Pass Book as a starting point.

Important points

- If the Starting point is Cash Book Balance then the ending point will be Pass Book Balance.

- If the starting point is Pass Book Balance then the ending point will be the Balance as per Cash Book.

- Debit Balance as per Cash Book or Credit Balance as per Pass Book, means that the firm has that much amount of deposit at the bank ->also called favourable balance -> write the amount under + items.

- Credit Balance as per Cash Book or Debit Balance as per Pass Book, means that this much amount has seen withdrawn in excess of deposit -> also called overdraft or unfavourable balance -> write the amount under items.

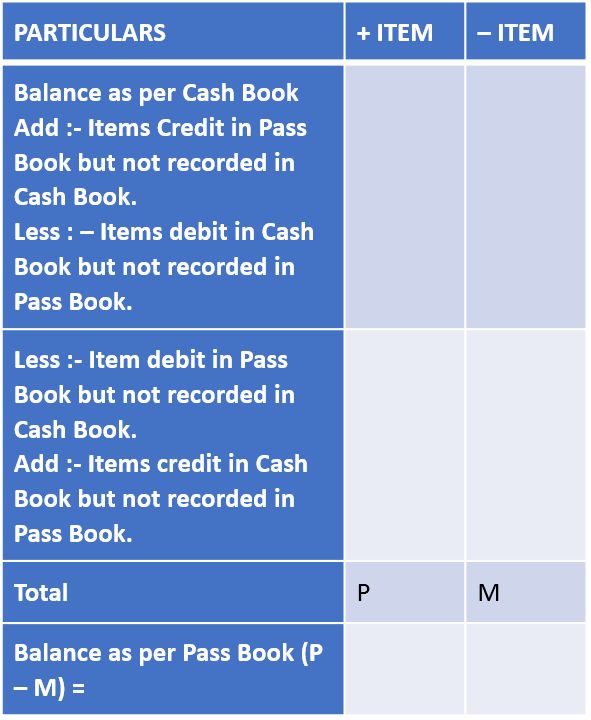

Method of preparing BRS starting with the Balance/overdraft as per Bank Column of Cash Book.

Bank Reconciliation Statement as on ………………………..

Note:

- If total of Plus (+) Items is more than the total of (-) items Difference is Credit Balance or favourable balance as per Pass Book.

- Where as if the – items total is more than the (+) items total then Difference is Debit Balance or overdraft as per Pass Book.

- If BRS is started with Balance as per Cash Book then ending point is Balance as per Pass Book and Vice-Versa.

- Debit balance of Cash Book means favourable balance or (+) Balance

- Debit balance of Pass Book means unfavourable balance or (-) balance.

- Credit balance of Pass Book means favourable balance or (+) balance

- Credit balance of Cash Book means unfavourable balance or (-) Balance.

Ready Reference Items which increase the pass Book Balance or decreases the Cash Book Balance

- Cheques issued but not yet presented.

- Credits made by the bank for Interest.

- Amount directly deposited by the customers in our bank A/c.

- Interest and dividend collected by the bank.

- Cheques paid into the bank but omitted to be recorded in the Cash – Book.

Items which decreases the pass Book Balance or increase the Cash Book Balance

- Cheques sent to the bank for collection but not yet credited by the – bank.

- Cheques paid into the bank but dishonoured.

- Direct payments made by the bank.

- Bank charges, commission etc. debited by the bank.

- Cheques issued but omitted to be recorded in the Cash Book.

READY REFERENCE

Items which increases the Cash Book Balance or decreases the Pass Book Balance

- Cheques deposited into the bank but dishonoured.

- Cheque sent for collection but not yet collected.

- Direct Payments made by the bank.

- Bank charges, commission etc.debited by the bank.

- Cheques issued but omitted to be recorded in the Cash Book.

Items which decreases the Cash Book Balance or increase the Pass Book Balance

- Cheques issued but not yet presented.

- Credits made by the bank for interest.

- Amount directly deposited by the customers into the Bank.

- Interest and dividend collected by the Bank.

- Cheques paid into the bank but omitted to be recorded in the Cash Book.

Amended Cash Book Method

Introduction: So far we have studied the preparation of Bank Reconciliation Statement simply by reconciling the causes of differences between the Cash Book and Pass Book. In actual practice adjustments are done in the Cash Book by comparing the Bank column of Cash Book with the Bank Statement and after that, B.R. Statement is prepared. It is called Amended Cash Book Method.

Procedure

- Adjusted Cash book prepared starting with the Balance of the Cash Book given in the question.

- All errors that have been committed in the Cash Book will have to be rectified by passing adjusting entries in the Cash Book.

Usual of General Errors are

- Overcasting or Undercasting of Debit/Credit Column of Cash – Book.

- Cheques deposited or Issued but omitted to be entered in the Cash Book.

- Incorrect amount (if any) entered in the Cash Book.

- Entries on the correct side or in the wrong column of Cash Book.

- Any amount recorded twice in the Cash Book.

Certain amounts for which Bank has debited our A/c will be recorded on the Credit side of Cash Book. Such items are

- Interest charged by the bank on overdraft, etc.

- Debits made by the bank for the bank charges, commission etc.

- Direct payments made by the Bank on behalf of the A/c holder.

- Cheques sent for collection but dishonoured.

Cash Book is then balanced: and the new Balance of the Cash book is taken as the starting point for preparing the B.R. Statement.

Important: It should be noted that the following items must not be recorded in the Amended Cash Book.

- Cheques deposited into the Bank but not yet credited by the Bank.

- Cheques Issued but yet not presented for payment.

- Any wrong Entry in Pass Book.

Points to Remember

- Amended or adjusted Cash Book is started with the given balance of bank as per Cash Book.

- Closing Balance of the adjusted Cash Book is the opening balance of bank Reconciliations statement.