Vision classes

Vision classes

- Books Name

- Vision classes Accountancy Book

- Publication

- Vision classes

- Course

- CBSE Class 11

- Subject

- Accountancy

Sales Return Book

This journal is used to record return of goods by customers to them on credit. On receipt of goods from the customer, a credit note is prepared, like the debit note referred to earlier. The difference between the credit not and the debit note is that the former is prepared by the seller and the latter is prepared by the buyer. Like the debit note, the credit note is also prepared in duplicate and contains detail relating to the name of the customer, details of the merchandise received back and the amount. Each credit note is serially numbered and dated. The source document for recording entries in the sales return book is generally the credit note.

Sales Return (Journal) Book

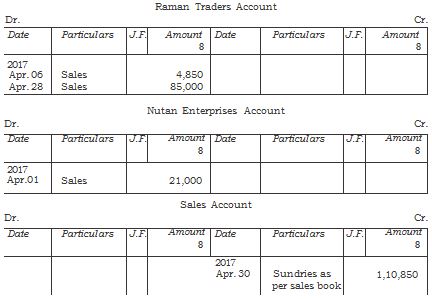

Refer to the sales (journal) book of Koina Supplier of you will find that two water purifiers were sold to Raman Traders for z 2,100 each, out of which one purifier was returned back due to the manufacturing defect (credit note no.10/2017). In this case, the sales return (Journal) book will be prepared as follows :

Sales Return (Journal) Book

Posting to the sales return journal requires that the customer's account be credited with the amount of returns and the sales return account be debited with the periodical total in the same way as is done in case of posting from the purchases journal.