Vision classes

Vision classes

- Books Name

- Vision classes Accountancy Book

- Publication

- Vision classes

- Course

- CBSE Class 11

- Subject

- Accountancy

Chapter 4

Recording of Transactions

Cash Book

Cash book is a book in which all transactions relating to cash receipts and cash payments are recorded. It starts with the cash or bank balances at the beginning of the period. Generally, it is made on monthly basis.

This is a very popular book and is maintained by all organisations, big or small, profit or not-for- profit. It serves the purpose of both journal as well as the ledger (cash) account. It is also called the book of original entry. When a cashbook is maintained, transactions of cash are not recorded in the journal, and no separate account for cash or bank is required in the ledger.

Single Column Cash Book

The single column cash book records all cash transactions of the business in a chronological order, i.e., it is a complete record of cash receipts and cash payments. When all receipts and payments are made in cash by a business organisation only, the cash book contains only one amount column on each (debit and credit) side.

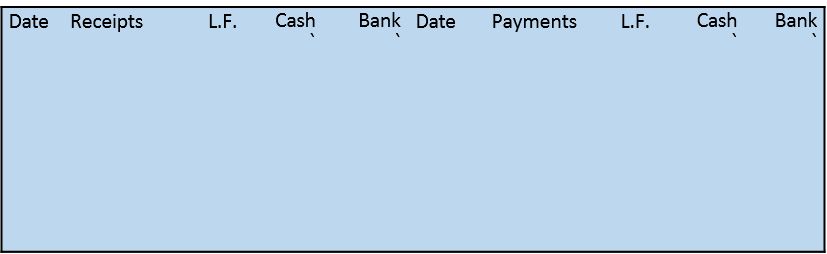

Cash book

(Format of single column cash book)

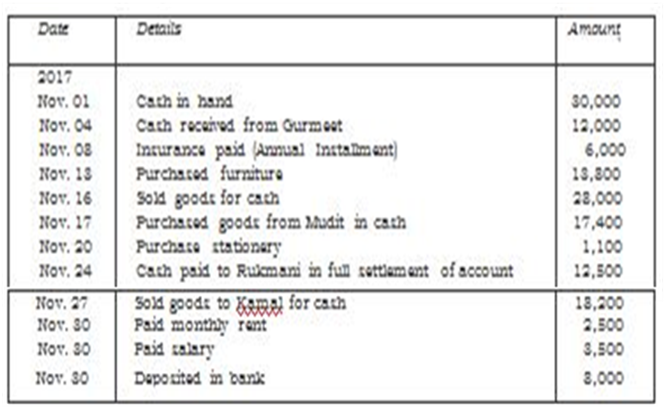

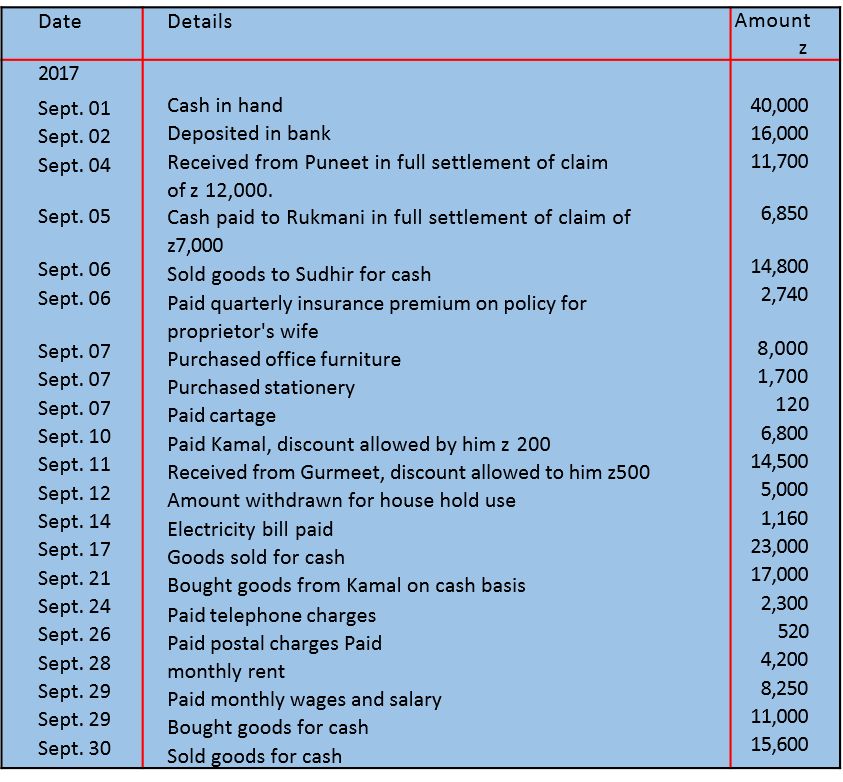

Recording of entries in the single column cash book and its balancing is illustrated by an example. Consider the following transactions of M/s Roopa Traders observe how they are recorded in a single column cash book.

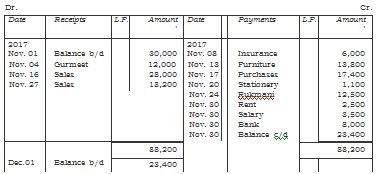

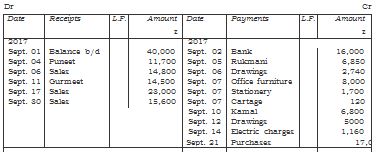

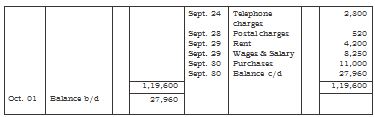

Roopa Traders Cash Book

Posting of the Single Column Cash Book

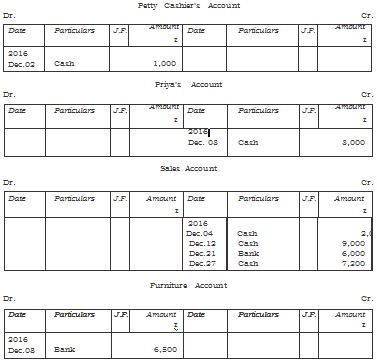

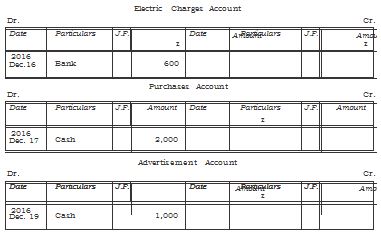

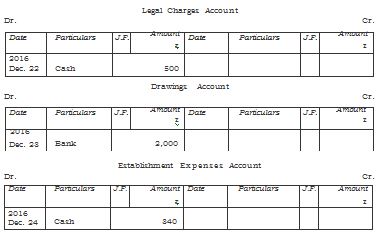

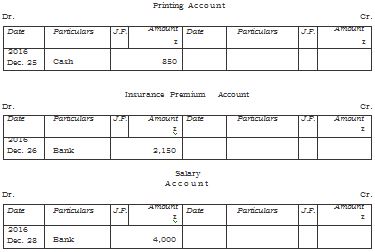

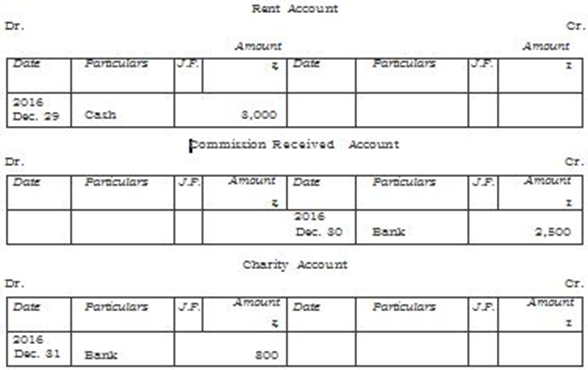

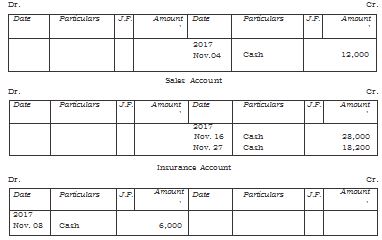

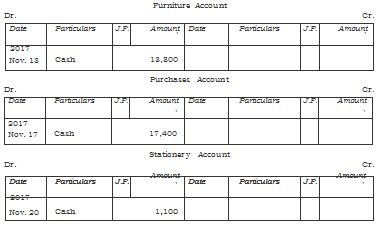

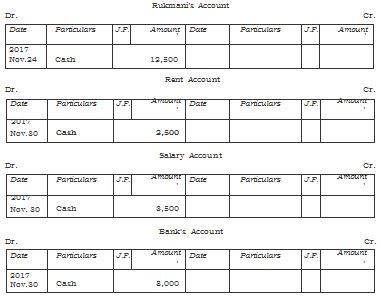

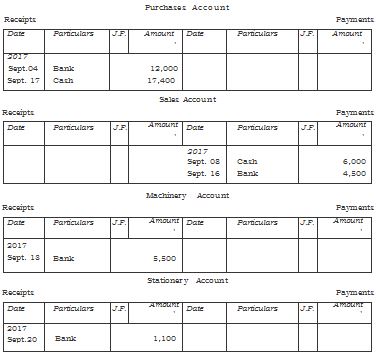

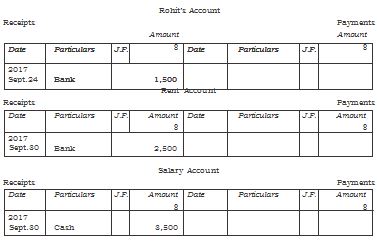

The left side of the cash book shows the receipts of the cash whereas the right side of the cash book shows all the payments made in cash. The accounts appearing on then debit side for the cash book are credited in the respective ledger accounts because cash has been received in respect of them. Thus, in our example, an entry 'cash received from Gurmeet' appears on the debit side of the cash book conveys that the cash has been received from Gurmeet. Therefore, in the ledger, Gurmeet's account will be credited by writing 'Cash' in the particulars column on the credit side. Similarly, all the account names appearing on the credit side of the cash book are debited as cash/cheque has been paid in respect of them. Now, notice, how the transactions in our example are posted to the related ledger accounts:

Books of Roopa Traders Gurmeet’s Account

Double Column Cash Book

In this type of cash book, there are two columns of amount on each side of the cash book. In fact, now-a-days bank transactions are very large in number. In many organisations, as far as possible, all receipts and payments are affected through bank.

A businessman generally opens a current account with a bank. Bank, do not allow any interest on the balance in current account but charge a small amount, called incidental charges, for the services rendered.

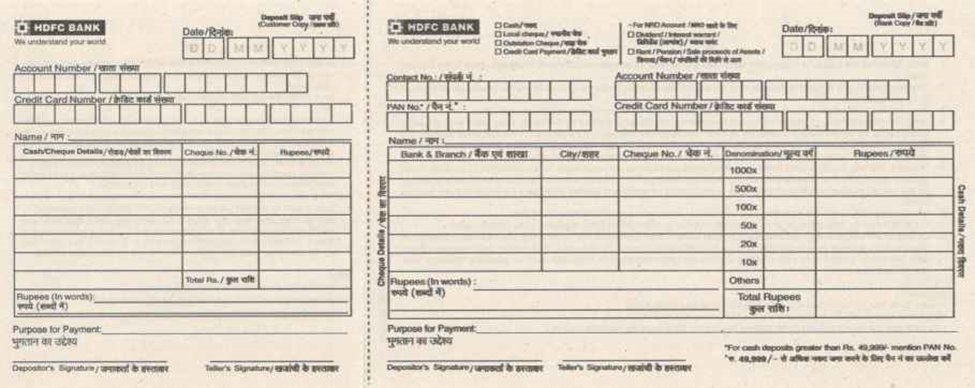

For depositing cash/cheques in the bank account, a form has to be filled, which is called a pay-in-slip. It contains a counterfoil also which is returned to the customer (depositor) with the signature of the cashier, as receipt.

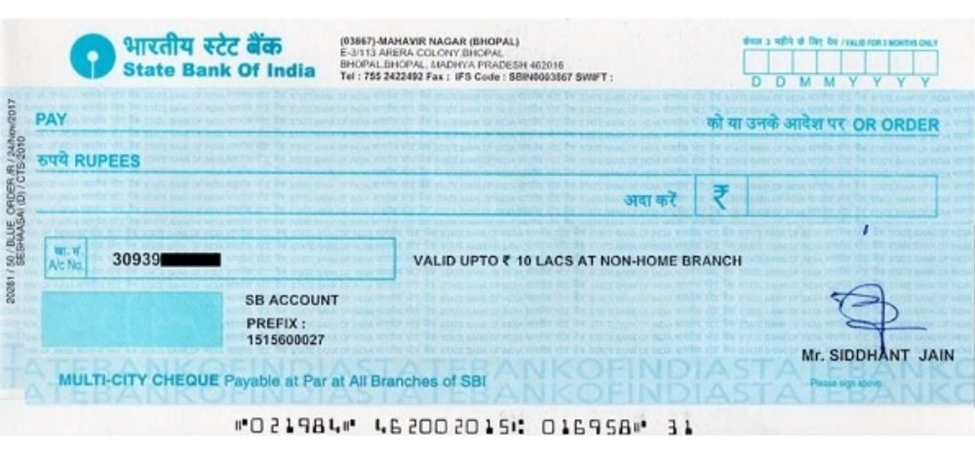

The bank issues blank cheque forms, to the account holder for withdrawing money. The depositor writes the name of the party to whom payment is to be made after the words Pay printed on the cheque. Cheque

forms have the printed word bearer, which means payment is to be made to the person whose name has been written after the words "pay" or the bearer of the cheques. When the world 'bearer' is struck off by drawing a line, the cheque becomes an order cheque. It means payment is to be made to the person whose name is written on the cheque or to his order after proper identification.

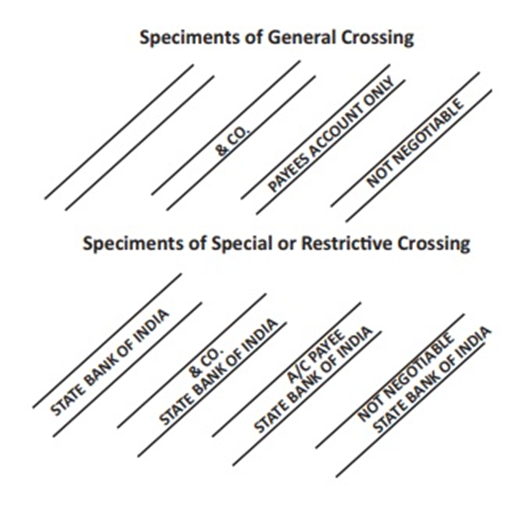

Cheques are generally crossed in practice. The payment of a crossed cheque cannot be made direct to the party on the counter. It is to be paid only through a bank. When two parallel lines are drawn across the cheque, it is said to be crossed. The various types of crossing providing different degrees of safety to the payment. In case of an A/c payee only crossing, the amount of the cheque can be deposited only in the account of the person whose name appears on the cheque. When the name of the bank is written between two parallel lines, it becomes a special crossing and the payment can be made only to the bank whose name has been written between the two lines.

Though this is rarely done, a cheque can be transferred by the payee (the person in whose favour the cheque has been drawn) to another person, if it is not crossed A/c payee only. A bearer cheque can be passed on by mere delivery. An order cheque can be transferred by endorsement and delivery. Endorsement means the writing of instructions to pay the cheque to a particular person and then singing it on the back of the cheque.

When the number of bank transactions is large; it is convenient to have a separate amount column for bank transactions in the cash book itself instead of recording them in the journal. This helps in getting information about the position of the bank account from time to time. Just like cash transactions, all payments into the bank are recorded on the left side and all withdrawals/payments through the bank are recorded on the right side. When cash is deposited in the bank or cash is withdrawn from the bank, both the entries are recorded in the cash book. This is so because both aspects of the transaction appear in the cash book itself. When cash is paid into the bank, the amount deposited is written on the left side in the bank column and at the same time the same amount is entered on the right side in the cash column. The reverse entries are recorded when cash is withdrawn from the bank for use in the office. Against such entries the word C, which stands for contra is written in the L.F. column indicating that these entries are not to be posted to the ledger account.

The bank column is balanced in the same way as the cash column. However, in the bank column, there can be credit balance also because of overdraft taken from the bank. Overdraft is a situation when cash withdrawn from the bank exceeds the amount of deposit. Entries in respect of cheques received should be made in the bank column of the cash book. When a cheque is received, it may be deposited into the bank on the same day or it may be deposited on another day. In case, it is deposited on the same day the amount is recorded in the bank column of the cash book on the receipts side. If the cheque is deposited on another day, in that case, on the date of receipt it is treated as cash received and hence recorded in the cash column on the receipts side. On the day of deposit to the bank, it is shown in the Bank Column on receipt (Dr.) side and in the Cash Column on the payment (Cr.) side. This is a contra entry.

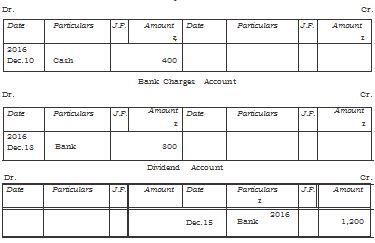

If a cheque received from a customer is dishonoured, the bank will return the dishonoured cheque and debit the firm's account. On receipt of such cheque or intimation from the bank, the firm will make an entry on the credit side of the cash book by entering the amount of the dishonoured cheque in the bank column and the name of the customer in the particulars column. This entry will restore the position prevailing before the receipt of the cheque form the customer and its deposit in the bank. Dishonour of a cheque means return of the cheque unpaid, generally due to insufficient funds in the customer's account with the bank.

If the bank debits the firm on account of interest, commission or other charges for bank services, the entry will be made on the credit side in bank column. If the bank credits the firm's account, the entry will be made on the debit side of the cash book in the appropriate column.

Cash book

We will now learn how the transactions are recorded in the double column cash book.

Consider the following example:

The following transactions related to M/s Tools India :

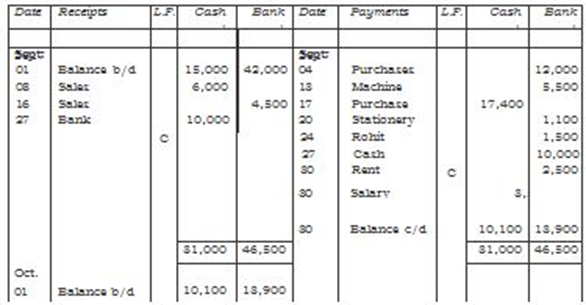

The double column cash book based upon above business transactions will prepared as follows:

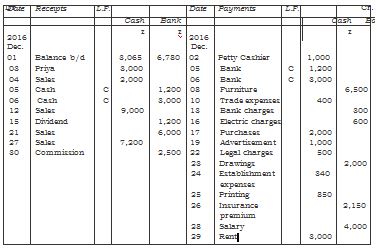

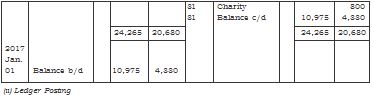

Cash book

When the bank column is maintained in the cash book, the bank account also is not opened in the ledger. The bank column serves the purpose of the bank account. Entries marked C (being contra entries as explained earlier) are ignored while posting from the cash book to the ledger. These entries represent debit or credit of cash account against the bank account or vice-versa. We will now see how the transactions recorded in double column cash book are posted to the individual accounts.

Petty Cash Book

In every organisation, a large number of small payments such as conveyance, cartage, postage, telegrams and other expenses (collectively recorded under miscellaneous expenses) are made. These are generally repetitive in nature. If all these payments are handled by the cashier and are recorded in the main cash book, the procedure is found to be very cumbersome. The cashier may be overburdened and the cash book may become very bulky. To avoid this, large organisations normally appoint one more cashier (petty cashier) and maintain a separate cash book to record these transactions. Such a cash book maintained by petty cashier is called petty cash book.

The petty cashier works on the Imprest system. Under this system, a definite sum, say 8 2,000 is given to the petty cashier at the beginning of a certain period. This amount is called imprest amount. The petty cashier goes on making all small payments out of this imprest amount and when he has spent the substantial portion of the imprest amount say 81,780, he gets reimbursement of the amount spent from the head cashier. Thus, he again has the full imprest amount in the beginning of the next period. The reimbursement may be made on a weekly, fortnightly or monthly basis, depending on the frequency of small payments. (In certain cases, the petty cash system is operated through the main cash book itself. In such instances, the petty cash book is not maintained independently.)

The petty cash book generally has a number of columns for the amount on the payment side (credit) besides the first other amount column. Each of the amount columns is allotted for items of specific payments, which are most common. The last amount column is designated as 'Miscellaneous' followed by a 'Remarks' column. In the miscellaneous column those payments are recorded for which a separate column does not exist. In the 'Remarks' the nature of payment is recorded. At the end of the period, all amount columns are totaled. The total amount column l shows the total amount spent and to be reimbursed. On the receipt (debit) side, there is only one amount column. Columns for the date, voucher number and particulars are common for both receipts and payments.

Balancing of Cash Book

On the left side, all cash transactions relating to cash receipts (debits) and on the right side all transactions relating to cash payments (credits) are entered date-wise. When a cash book is maintained, a separate cash book in the ledger is not opened. The cash book is balanced in the same way as an account in the ledger. But it may be noted that in the case of the cash book, there will always be debit balance because cash payments can never exceed cash receipts and cash in hand at the beginning of the period.

The source document for cash receipts is generally the duplicate copy of the receipt issued by the cashier. For payment, any document, invoice, bill, receipt, etc., on the basis of which payment has been made, will serve as a source document for recording transactions in the cash book. When payment has been made, all these documents, popularly known as vouchers, are given a serial number and filed in a separate file for future reference and verification.

Example 1

From the following transactions made by M/s Kuntia Traders, prepare the single column cashbook.

Solution

Books of Kuntia Traders

Cash Book

Example 2

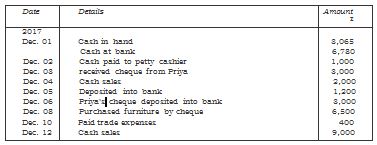

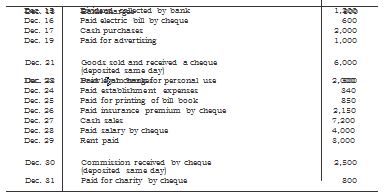

Prepare double column cash book of M/s Advance Technology Pvt. Ltd. for the month of December 2014 from the following transactions:

Solution

Books of Advance Technology

Cash Book