PathSet Publications

PathSet Publications

- Books Name

- Understanding Economic Development Class-10

- Publication

- PathSet Publications

- Course

- CBSE Class 10

- Subject

- Economics

BANK ACTIVITIES

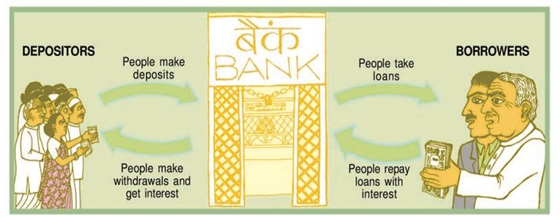

- Have you ever wondered what the bank does with your deposits?

- Banks keep only a small proportion of their deposits as cash with themselves. For example, banks in India these days hold about 15 percent of their deposits as cash. This is kept as a provision to pay the depositors who might come to withdraw money from the bank on any given day.

- Since, on any particular day, only some of its many depositors come to withdraw cash, the bank can manage with this cash. Banks use the major portion of the deposits to extend loans because there is a huge demand for loans for various economic activities.

- In this way, banks mediate between those who have surplus funds (the depositors) and those who need these funds (the borrowers).

- Banks charge a higher interest rate on loans than what they offer on deposits. The difference between what is charged from borrowers and what is paid to depositors is their main source of income.

- A large number of transactions in our day-to-day activities involve credit in some form or the other.

- Credit (loan) refers to an agreement in which the lender supplies the borrower with money, goods, or services in return for the promise of future payment. Let us look at different credit situations.

TWO DIFFERENT CREDIT SITUATIONS

- In our first situation, we have an order and to complete that within time, we obtain a credit to meet the working capital needs of production. The credit helps us to meet the ongoing expenses of production, complete production on time, and thereby increase earnings. Credit, therefore, plays a vital and positive role in this situation.

- In our other situation, let’s say crop production, the main demand for credit is to meet considerable costs on seeds, fertilizers, pesticides, water, electricity, repair of equipment, etc. There is a minimum stretch of three to four months between the time when the farmers buy these inputs and when they sell the crop. Farmers usually take crop loans at the beginning of the season and repay the loan after harvest. Repayment of the loan is crucially dependent on the income from farming. If there is a failure in the crop, loan repayment is impossible. The borrower has to repay the loan by either selling land or taking more loans. This leaves them worse off.

- Thus, we can see that credit can leave us in two situations. In one situation, credit helps to increase earnings and therefore the person is better off than before. In another situation, credit pushes the person into a debt trap.

- Every loan agreement specifies an interest rate, which the borrower must pay to the lender along with the repayment of the principal. In addition, lenders may demand collateral (security) against loans.

- Collateral is an asset that the borrower owns (such as land, building, vehicle, livestock, deposits with banks) and uses this as a guarantee to a lender until the loan is repaid. If the borrower fails to repay the loan, the lender has the right to sell the asset or collateral to obtain payment.

- Property such as land titles, deposits with banks, livestock is some common examples of collateral used for borrowing.

- Interest rate, collateral and documentation requirement, and the mode of repayment together comprise what is called the terms of credit.

LOANS FROM COOPERATIVES :

- Besides banks, the other major source of cheap credit in rural areas are cooperative societies.

- Members of a cooperative pool their resources for cooperation in certain areas.

- It accepts deposits from its members. With these deposits as collateral, the Cooperative has obtained a large loan from the bank.

- These funds are used to provide loans to members. Once these loans are repaid, another round of lending can take place

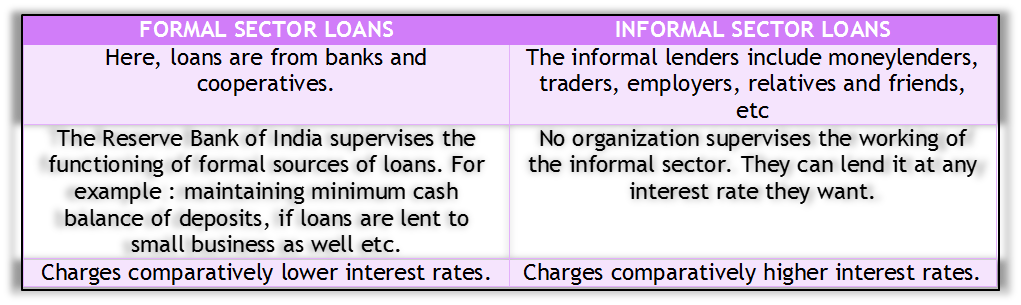

The loans can be categorized into two categories: Formal sector loans and informal sector loans. Let us look at the difference between the two.

- Is there a problem if lenders charge a high rate of interest? Indeed, yes.

- A higher cost of borrowing means a larger part of the earnings of the borrowers is used to repay the loan. Hence, borrowers have less income left for themselves. In certain cases, the high-interest rate for borrowing can mean that the amount to be repaid is greater than the income of the borrower. This could lead to increasing debt and a debt trap. In addition, people who might wish to start an enterprise by borrowing may not do so because of the high cost of borrowing.

- Cheap and affordable credit is crucial for the country’s development. That is why it is preferred that the formal sector extends cheap loans.

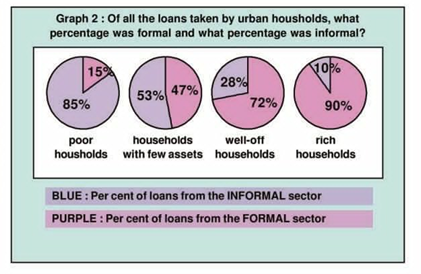

- 85 percent of the loans taken by poor households in the urban areas are from informal sources whereas only 10 percent of the urban rich households lend loans from the informal sectors.

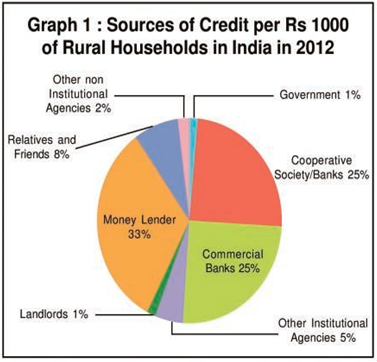

- This implies that the formal sector meets only about half of the total credit needs of the rural people. Thus, banks and cooperatives must increase their lending particularly in the rural areas so that the dependence on informal sources of credit reduces

- Secondly, while formal sector loans need to expand, it is also necessary that everyone receives these loans

SELF HELP GROUPS FOR POOR

- The absence of collateral is one of the major reasons which prevents the poor from getting bank loans while no such thing is seen in the informal sector. However, the moneylenders charge very high rates of interest keep no records of the transactions and harass the poor borrowers.

- A new idea of Self-help groups (SHG) has been started in rural areas, particularly by women, to pool their savings.

- Saving per member varies from Rs 25 to Rs 100 or more, depending on the ability of the people to save. Members can take small loans from the group itself to meet their needs.

- The group charges interest on these loans but this is still less than what the moneylender charges. After a year or two, if the group is regular in savings, it becomes eligible for availing loan from the bank.

- The loan is sanctioned in the name of the group and is meant to create self-employment opportunities for the members.

- Most of the important decisions regarding the savings and loan activities are taken by the group members.

- The group decides as regards the loans to be granted — the purpose, amount, interest to be charged, etc. and failure of repayment of the loan by any one member is followed up seriously by other members in the group.

- SHGs are the building blocks of the organization of the rural poor. Not only does it help women to become financially self-reliant, but the regular meetings of the group also provide a platform to discuss and act on a variety of social issues such as health, nutrition, domestic violence, etc.